Many people buy life insurance thinking it is also a way to invest. That confusion is common, but it can lead to the wrong choice. The primary purpose of life insurance is financial protection for your family if something happens to you. The different types of life insurance in India serve different goals, and knowing the difference can help you choose more wisely.

This guide explains the major types of life insurance policy available in India, including term insurance, endowment plans, ULIPs, money back policies, and whole life policies. It also shows how to compare them based on protection, savings, risk, and suitability so you can decide what matters most for your family.

What is Life Insurance and Why Do You Need It?

Life insurance is a contract in which you pay a premium to an insurer, and in return the insurer promises to pay a sum of money to your nominee if you pass away during the policy term. In some plans, you may also receive a maturity benefit if you survive the policy term.

Life insurance is a contract in which you pay a premium to an insurer, and in return the insurer promises to pay a sum of money to your nominee if you pass away during the policy term. In some plans, you may also receive a maturity benefit if you survive the policy term.

The core idea is simple: replace the income your family may lose. If you are earning, have dependents, a home loan, children’s education goals, or other liabilities, life insurance can act as a financial safety net.

The most important number in a life insurance policy is the sum assured. This is the amount the insurer promises under the policy terms. For pure protection plans, a higher sum assured usually means better family protection. For savings-linked plans, you should also understand what part of your premium goes toward insurance cover and what part is used for savings or investment.

In India, life insurance products are regulated by IRDAI (Insurance Regulatory and Development Authority of India). That means policy wording, charges, claim rules, and benefits follow regulatory guidelines, but each product still has its own terms and exclusions. Always read the policy document carefully.

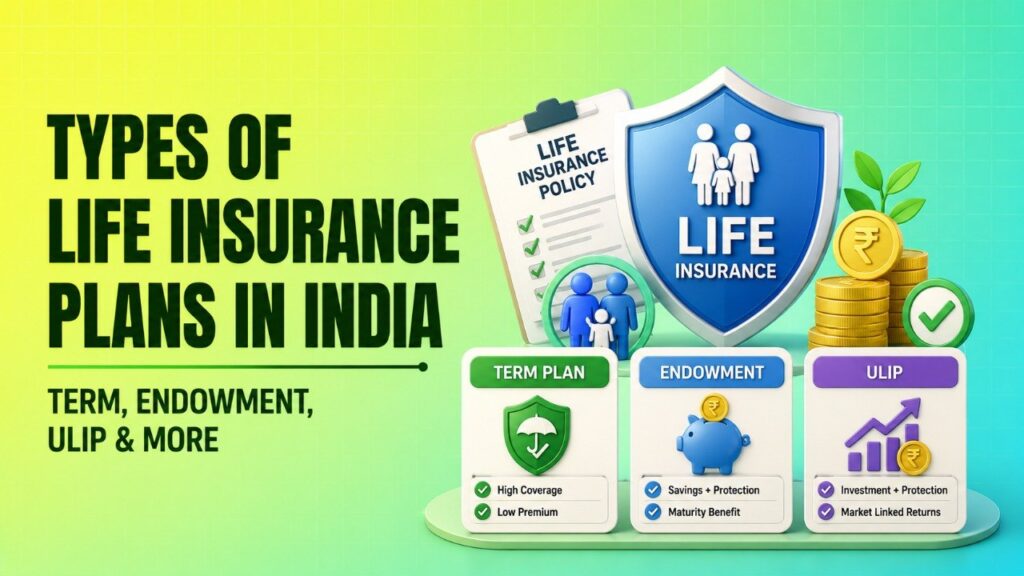

Term Insurance: Pure Protection

Term insurance is the simplest and most transparent form of life cover. You pay a relatively low premium for a large death benefit. If the policyholder dies during the policy term, the nominee receives the sum assured. If the policyholder survives the term, there is usually no maturity value.

Term insurance is the simplest and most transparent form of life cover. You pay a relatively low premium for a large death benefit. If the policyholder dies during the policy term, the nominee receives the sum assured. If the policyholder survives the term, there is usually no maturity value.

This is why term insurance is often called pure protection. You are paying for risk cover, not for returns. That is also why term insurance usually offers much higher cover for a lower premium than savings-linked plans.

For example, a healthy young salaried person can usually get a much larger cover through term insurance than through a plan that mixes insurance and investment. Premiums also depend on age, health condition, smoking status, policy term, and sum assured. As a rule, the older you are when you buy, the higher the premium tends to be.

Some term plans offer a Return of Premium option, often called TROP. Under this structure, the insurer may return the base premiums paid if the policyholder survives the term, subject to policy terms. TROP is not a separate class of insurance; it is an add-on feature within term insurance. The trade-off is that the premium is usually higher than a standard term plan.

Who is it for? Term insurance suits people who want the most protection for the least cost. It is usually the first plan to consider if your main goal is income replacement for dependents.

Endowment Plans: The Hybrid Approach

Endowment plans combine life insurance and savings. They offer a payout either on maturity or on death during the policy term, depending on the policy terms. Because they include a savings element, premiums are higher than a pure term plan.

These plans may feel attractive because they appear to offer both protection and a lump sum later. But the returns are usually lower than what you might expect from a separate long-term investment product, especially after considering inflation and charges. That is why endowment plans should be viewed carefully rather than assumed to be the “best” of both worlds.

Endowment plans may suit people who want disciplined saving with some life cover, especially if they value certainty over higher return potential. Even then, you should compare the maturity value, premium outgo, and coverage clearly before buying.

Who is it for? Endowment plans may appeal to conservative savers who want a fixed-style outcome and do not want market-linked risk.

ULIPs (Unit Linked Insurance Plans)

ULIPs are market-linked life insurance products. A portion of your premium goes toward life cover, while the remaining portion is invested in equity, debt, or balanced funds, depending on the fund choice under the policy.

This means your policy value may rise or fall based on market performance and the fund’s performance. ULIPs also usually have a lock-in period, and charges may apply in different forms such as premium allocation charges, policy administration charges, fund management charges, and mortality charges. The exact structure depends on the policy document.

ULIPs are not plain insurance plans and not plain mutual funds either. They sit somewhere in between. The insurance component gives life cover, while the investment component gives market exposure. Because of this structure, you should compare the cost of insurance, charges, fund options, and lock-in before committing.

A useful way to think about ULIP is to separate sum assured from market value. The sum assured is the insurance promise under the policy. The market value is the value of the fund units you hold, and it depends on market movement. These are not the same thing.

Who is it for? ULIPs may suit people who want life cover plus long-term market-linked investment and who understand market risk and charges.

Money Back and Whole Life Policies

Money back policies are a type of life insurance where a part of the sum assured is paid out at regular intervals during the policy term, instead of only at maturity. The balance, if any, is paid at maturity or on death as per policy terms.

These plans can feel comforting because they provide periodic payouts. However, the total benefit structure, premium level, and long-term value should be checked carefully. Money back plans are usually chosen for specific cash flow needs rather than for maximum return or maximum cover.

Whole life policies provide coverage for a very long period, often until age 99 or 100, depending on the product. They are less common for everyday retail buyers but may be considered by people who want lifelong coverage or estate-planning style protection.

Who are these for? Money back plans are for people who want periodic payouts. Whole life policies are for those who want very long-term protection and are comfortable with the premium structure.

Quick Comparison: Which Plan Suits Your Goal?

| Plan Type | Primary Goal | Risk Level | Liquidity | Tax Benefit | Best For |

|---|---|---|---|---|---|

| Term Insurance | Pure protection for family | Low | Low during term; no maturity value in standard plans | May qualify under Section 80C and 10(10D), subject to current tax rules and policy terms | Earners with dependents, loans, and a need for high cover |

| Endowment Plan | Protection plus savings | Low to moderate | Lower than pure savings products; surrender may reduce value | May qualify under Section 80C and 10(10D), subject to conditions | Conservative savers who want fixed-style outcomes |

| ULIP | Insurance plus market-linked investment | Moderate to high | Limited by lock-in period; subject to fund performance | May qualify under Section 80C and 10(10D), subject to applicable tax rules | Long-term investors comfortable with market risk |

| Money Back | Periodic payouts with life cover | Low to moderate | Moderate, depending on policy structure | May qualify under Section 80C and 10(10D), subject to policy terms | People who want scheduled payouts |

| Whole Life | Coverage for a very long duration | Low | Usually low to moderate, depending on plan design | May qualify under Section 80C and 10(10D), subject to conditions | Those seeking lifelong protection |

Life Insurance Purpose Matcher

Use this simple guide to narrow down what you may want to research next. This is for educational purposes only and does not constitute financial advice. Please consult a licensed professional before buying any policy.

Step 1: Choose your age band.

- Young earner: below 35

- Mid-career: 35 to 50

- Near-retirement: above 50

Step 2: Pick your main goal.

- Protection

- Protection plus some savings

- Long-term market-linked growth

Step 3: Choose your risk appetite.

- Low risk

- Moderate risk

- Comfortable with market risk

Simple result guide:

- If you are a young earner with a protection goal and low risk appetite, start with term insurance.

- If you want protection plus savings and prefer predictable outcomes, compare endowment plans carefully.

- If you are comfortable with market risk and want long-term growth with insurance, research ULIPs after checking charges and lock-in.

- If you want very long cover or periodic payouts, check whole life or money back plans.

Before using any policy illustration, read the policy document, exclusions, benefit schedule, charges, and claim conditions.

Critical Factors to Consider Before Buying

Choosing from the different types of life insurance should begin with your life stage, not with a sales pitch. A policy that works for one person may be unsuitable for another.

1) Age

Age affects premium directly. Younger buyers usually pay lower premiums for the same cover. If you wait too long, the cost of insurance rises, and some products may become less efficient.

2) Annual income

Your insurance cover should ideally be connected to your income. The goal is to replace part of your family income for several years if you are not around. Buying too little cover can leave your family exposed.

3) Liabilities

Consider all loans such as home loans, education loans, and personal loans. If you have debt, your life insurance cover should take those obligations into account so your family is not forced to repay them from savings.

4) Dependents

If your spouse, children, ageing parents, or anyone else relies on your income, you need a stronger cover than someone with no dependents.

5) Claim Settlement Ratio

The claim settlement ratio tells you how many claims an insurer settles compared to the total claims it receives in a period. It does not guarantee your claim will be approved, but it is a useful indicator of claim experience. Always check the latest figures from the insurer’s official disclosures and IRDAI-related information before buying.

6) Policy wording and exclusions

Do not rely only on brochures. Read the policy document, exclusions, waiting periods, surrender terms, and nomination details. Claim outcomes depend on the exact policy terms and honest disclosure at the time of purchase.

Common Mistakes to Avoid

- Mixing insurance with investment without understanding the trade-off: A policy with savings or market exposure is not automatically better than a pure protection plan. First ask whether you need cover or wealth creation.

- Buying too little sum assured: Many people focus on the premium and ignore whether the cover is actually enough for the family’s needs, loans, and future expenses.

- Ignoring age-related cost: Waiting too long usually makes premiums higher. Buying earlier can make protection more affordable.

- Hiding health or lifestyle information: Non-disclosure of smoking, medical history, or other material facts can cause claim problems later. Be accurate in the proposal form.

- Not checking surrender charges: If you stop a policy early, you may lose part of the value. This matters especially in endowment plans and ULIPs.

- Assuming tax benefit is the main reason to buy: Tax benefit under Section 80C and possible tax treatment under Section 10(10D) depend on current law and policy conditions. Never buy a weak policy only for tax saving.

Life insurance works best when it is chosen for the right purpose. If your main need is family protection, a term plan often gives the most cover for the lowest cost. If you want some savings or market-linked investment along with insurance, endowment plans and ULIPs may fit better, but they come with different costs, limitations, and risk levels.

The safest way to compare life insurance is to first decide your goal: protection, savings, or long-term market-linked growth. Then check the sum assured, charges, exclusions, lock-in, claim conditions, and tax treatment. Because policy rules and tax rules can change, verify the latest details from IRDAI, the insurer’s official policy wording, and the Income Tax Department before buying.

FAQs

Is it better to buy Term Insurance or Endowment?

If your main goal is financial protection for your family, term insurance is usually the better choice because it gives much higher cover at a lower premium. If you want savings along with insurance, you can consider an endowment plan, but the cover is usually lower and the return side should be compared carefully.

Can I have more than one life insurance policy?

Yes, you can have more than one life insurance policy. Many people do this to separate needs, such as one term plan for family protection and another policy for a specific goal. The total cover should still be based on your income, liabilities, and dependents.

What is the Claim Settlement Ratio and why does it matter?

The claim settlement ratio shows the percentage of claims an insurer settles out of the claims it receives. A higher ratio generally suggests better claim experience, but it does not guarantee approval. Policy terms, documents, and truthful disclosure still matter most.

Do I get tax benefits on all types of life insurance?

Many life insurance premiums may qualify for tax deduction under Section 80C, subject to current tax rules and limits. The payout may also receive tax treatment under Section 10(10D), but only if the policy and conditions meet the law. Always verify the latest rules before relying on tax benefits.

Can I surrender my life insurance policy?

Yes, many policies can be surrendered, but surrender charges or loss of benefits may apply, especially if you exit early. In some plans, the surrender value may be much lower than the total premiums paid. Read the policy document before making this decision.