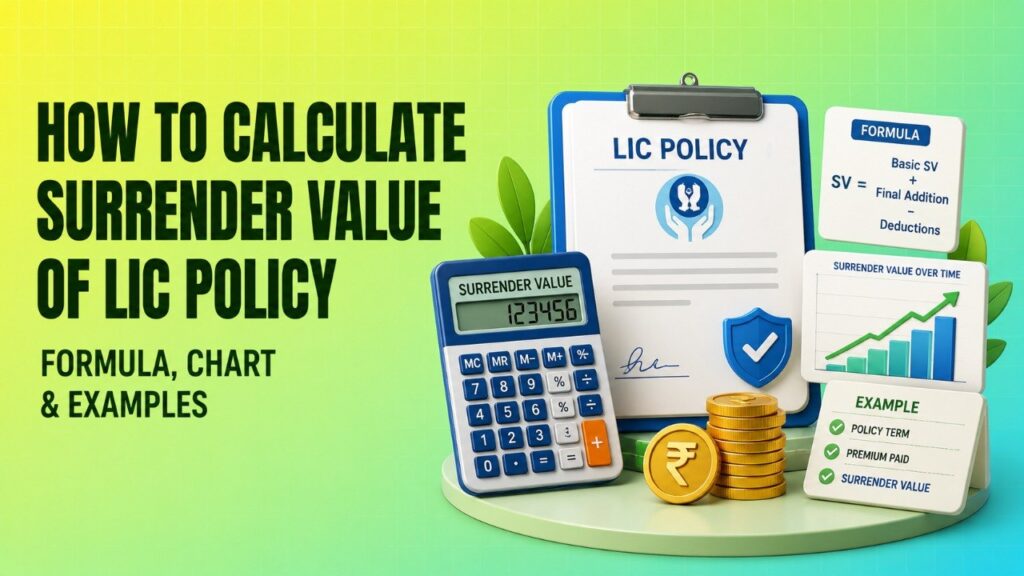

If you need money urgently and are thinking about closing your LIC policy before maturity, the first thing to understand is the surrender value of LIC policy. This is the amount LIC may pay you if you exit the policy early. It is an early exit, not a full refund, and in most cases it leads to a financial loss compared with continuing the policy till maturity.

If you are trying to figure out how to calculate surrender value of LIC, the answer is not just one simple formula. The payout depends on the policy type, premium-paying term, bonuses, and LIC’s surrender factors. That is why many policyholders receive a lower amount than they expect. The good news is that once you understand the logic, the estimate becomes much easier to follow.

What is Surrender Value in an LIC Policy?

Surrender value is the amount LIC pays when you terminate the policy before the maturity date. It is usually available only after you have paid premiums for a minimum period, commonly 2 to 3 years depending on the plan terms. If you surrender too early, you may get nothing or only a very small amount.

Surrender value is the amount LIC pays when you terminate the policy before the maturity date. It is usually available only after you have paid premiums for a minimum period, commonly 2 to 3 years depending on the plan terms. If you surrender too early, you may get nothing or only a very small amount.

The exact amount is not fixed in a single universal way because LIC policy terms differ by plan. The policy bond, surrender clause, and LIC’s current rules are the final authority. In practical terms, surrender value is the exit amount after LIC applies its internal valuation rules to your policy.

For most traditional plans such as endowment or money-back policies, the surrender value is linked to the premiums paid, the vested bonuses earned, and the reduced paid-up benefit. That is why two policyholders with similar policies may still receive different amounts if their premium history or bonus accumulation is different.

Understanding the Two Types of Surrender Value

LIC generally uses two concepts while evaluating an early exit: Guaranteed Surrender Value and Special Surrender Value. These are not the same, and the final payout may depend on whichever method gives the higher amount under the applicable rules.

Guaranteed Surrender Value (GSV)

Guaranteed Surrender Value is the minimum surrender amount defined in the policy terms. It is usually calculated as a percentage of the premiums you have paid, excluding the first-year premium and often excluding certain charges and riders. In simple words, this is the baseline amount.

GSV is useful because it gives you a floor value. However, it is often lower than what you might receive under the special surrender calculation, especially if the policy has earned bonuses and LIC’s surrender factors are favourable.

Special Surrender Value (SSV)

Special Surrender Value is generally the more important figure for policyholders because it often results in a higher payout. It is commonly linked to the paid-up value plus vested bonuses, then adjusted by LIC’s special surrender factor. This factor is not a public fixed number and can change based on LIC’s internal valuation rules and plan-wise conditions.

In many cases, the surrender amount you actually receive is closer to the special surrender value than the guaranteed value. That is why people searching for lic surrender value after 5 years often need to understand the paid-up value first before they can estimate the final amount.

The Formula to Estimate Your Surrender Value

A simple way to understand the payout logic is this:

(Paid-up Value + Vested Bonus) × SSV Factor = Estimated Surrender Value

This is only an estimation flow. LIC may apply plan-specific conditions, cut-offs, and valuation rules. The final payable amount should always be confirmed through LIC’s branch, portal, or your policy bond.

| Term | Definition | Why It Matters |

|---|---|---|

| Paid-up Value | The reduced benefit amount after stopping future premiums, based on premiums already paid. | Determines the base claim for surrender calculation. |

| Vested Bonus | Bonuses already declared and attached to the policy, if applicable. | Added to the base value and can increase the payout. |

| SSV Factor | LIC’s special multiplier used to arrive at surrender value. | It decides the final payout amount and may change by plan and period. |

To understand this better, let us break down the most confusing part: the paid-up value.

The paid-up value is the reduced policy value when you stop paying future premiums after completing the minimum eligible period. If a policy has a sum assured of ₹10 lakh, but you stop paying midway after qualifying years, the policy does not retain the full ₹10 lakh benefit. Instead, LIC reduces it in proportion to the premiums paid.

A simple paid-up value logic is:

Paid-up Value = (Sum Assured × Number of premiums paid) ÷ Total number of premiums payable

However, this is only a simplified formula to understand the concept. LIC may use the plan’s exact terms, bonus additions, and surrender rules to calculate the payable amount. Always treat this as a learning formula, not the final quote.

Example: Suppose a policy has a sum assured of ₹5 lakh, the premium term is 20 years, and you have paid premiums for 10 years. The paid-up value conceptually becomes about 50% of the sum assured, before adding bonuses and applying the surrender factor. If the policy has vested bonuses, those are added, and then LIC’s special surrender factor is applied.

That is why the real payout can be much lower or higher than a rough guess. The bonus amount and SSV factor matter a lot.

Step-by-Step Guide to Calculate and Process Your Surrender

If you want to know the surrender amount and then close the policy, follow this practical sequence.

- Check eligibility first. Most LIC policies allow surrender only after paying premiums for at least 2 to 3 years. Read your policy bond to confirm the minimum period for your plan.

- Request an official surrender quote. Use the LIC portal if available for your policy or visit the home branch. The official quote is the most reliable number because it reflects the exact plan rules, bonuses, and current surrender factors.

- Collect the required documents. Usually this includes the original policy bond, bank account details, a cancelled cheque, and a valid ID proof. Some branches may ask for additional forms or KYC documents.

- Submit the surrender request at the home branch. Most surrender requests are processed through the policy’s servicing branch. Fill the surrender form carefully, attach the required documents, and submit the original policy bond if required.

- Wait for verification and payment. After validation, LIC credits the surrender amount to the bank account linked in your request form.

If the policy is in force and you only need temporary liquidity, also ask LIC whether a policy loan is available before surrendering. In many cases, a loan against policy may be a less painful option than closing the policy early.

LIC Surrender Value Estimation Logic

The box below is a simple way to understand what goes into the final amount. It is not a replacement for LIC’s official calculation. LIC applies proprietary special surrender value factors that can change periodically. Please get an official surrender quote from the LIC portal or branch before submitting the final application.

| Component | What to Check | Impact on Payout |

|---|---|---|

| Total premiums paid | Count only the premiums you have actually paid, and check whether the first-year premium is excluded in GSV. | Builds the base for paid-up value and surrender eligibility. |

| Years premiums paid | Check whether you have completed the minimum 2 to 3 years needed for surrender. | Decides whether the policy can be surrendered at all. |

| Total sum assured | Read the sum assured from the policy bond. | Used to estimate paid-up value. |

| Vested bonuses | Look at the bonuses accrued so far, if your plan participates in bonuses. | Increases the potential surrender amount. |

| SSV factor | Confirm the applicable factor from LIC through the branch or official servicing channel. | Determines the final payout. |

Quick logic flow: eligibility check → paid-up value calculation → bonus addition → special surrender factor → final quote.

Is Surrendering Your Policy the Best Move?

For many policyholders, surrendering a policy solves a short-term cash problem, but it often comes at a cost. You may lose part of the premium you already paid, lose future bonuses, and give up the life cover. That is why surrendering is usually a financial loss, even if the immediate cash feels useful.

For many policyholders, surrendering a policy solves a short-term cash problem, but it often comes at a cost. You may lose part of the premium you already paid, lose future bonuses, and give up the life cover. That is why surrendering is usually a financial loss, even if the immediate cash feels useful.

Before you surrender, compare the surrender amount with the policy loan option. A loan against policy lets you borrow against the policy’s value while keeping the policy active, depending on the plan’s loan eligibility. This can be helpful if you need funds temporarily and do not want to end the policy entirely.

Here is a simple way to think about it:

- Surrender: You get an exit amount now, but you permanently lose the policy and future benefits.

- Loan against policy: You may keep the policy in force, but you will have to repay the loan and interest as per LIC’s terms.

The better choice depends on your liquidity need, repayment ability, and the specific policy rules. Since charges and terms can change, verify the latest details with LIC before making a decision.

Common Mistakes to Avoid When Surrendering

A lot of people lose money or face delays because they rush the surrender process. These are the most common mistakes to avoid:

- Not checking the surrender quote first: Always ask for the official amount before you submit the surrender form.

- Assuming a full refund: LIC policies do not usually return all premiums on early exit. A surrender is not a full refund.

- Submitting wrong bank details: A mismatch in account number or IFSC can delay payment.

- Ignoring the original policy bond: Many branches require the original bond for processing.

- Overlooking loss of life cover: Once surrendered, the insurance protection stops.

- Forgetting tax checks: Some policy proceeds may have tax implications depending on premium size and the conditions of Section 10(10D). Verify current rules before acting.

Also remember that the policy bond and LIC’s official website are the final authorities. If anything in your policy wording differs from a general explanation online, the policy document wins.

Rules, payout factors, and processing times can change, so always confirm the latest details from LIC or the branch servicing your policy. If your policy has a loan option and you only need short-term money, compare that carefully before you surrender.

FAQ

Can I get a full refund of my LIC premiums?

No. If you surrender an LIC policy early, you usually get less than the total premiums paid. Early surrender often causes a financial loss.

How many years of premium do I need to pay to be eligible for surrender?

Generally, LIC policies require at least 2 to 3 years of premium payment before surrender is allowed. Check your policy bond for the exact rule.

How long does LIC take to pay the surrender amount?

Usually, the payment takes about 7 to 15 working days after successful submission and verification, but the timeline can vary by branch and document accuracy.

Do I need the original policy bond for surrender?

Yes, in most cases the original policy bond is required when you submit the surrender request.

Is the surrender value taxable?

It can be, depending on the policy terms and tax rules. Section 10(10D) may apply in some cases, but tax treatment depends on premium limits and current Income Tax rules. Verify with a tax professional or the latest official guidance.