A life insurance policy is a simple risk-transfer tool that helps your family manage money if something happens to you. It is mainly meant for protection, not as a shortcut to build wealth.

If you have ever wondered what is life insurance or searched for a clear life insurance definition, the short answer is this: you pay a premium to an insurer, and the insurer promises to pay a benefit to your nominee or legal heir, subject to the policy terms.

Used properly, life insurance can protect loans, replace income, and give your family financial breathing room during a difficult time.

What is Life Insurance and How Does It Really Work?

Life insurance is a contract between you and the insurer. You pay premiums regularly, and in return the insurer provides financial cover for a chosen period or, in some policies, for life.

The key terms are easy to understand:

- Sum assured: The amount the insurer promises to pay if the insured event happens.

- Premium: The price you pay to keep the policy active.

- Nominee: The person who receives the claim amount as per the policy terms.

Insurance works on the principle of Utmost Good Faith. That means you must disclose all relevant facts honestly, especially about age, health, smoking, occupation, medical history, and existing policies. If important facts are hidden, a claim can be delayed or rejected later.

For Indian buyers, it is wise to read the policy wording and the Customer Information Sheet carefully before paying the first premium. These documents explain benefits, exclusions, waiting periods, charges, and claim rules in plain language.

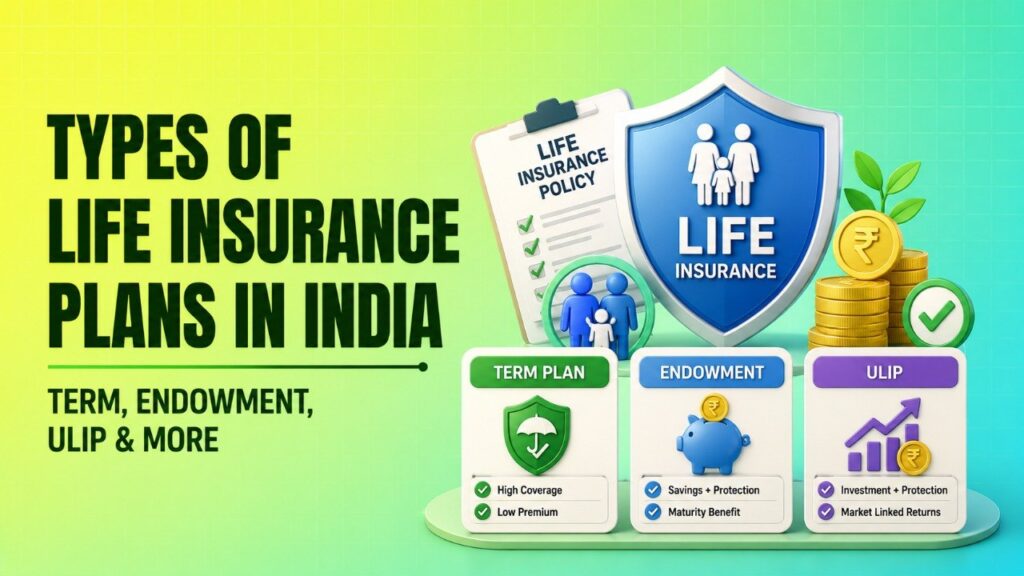

Types of Life Insurance Policies in India

There are a few common types of life insurance policies in India. Each serves a different purpose.

Term Insurance (Pure Protection)

Term insurance gives the highest cover for a relatively low premium. If the policyholder dies during the term, the nominee gets the sum assured. If the policyholder survives the term, there is usually no maturity payout in a plain term plan.

This is often the best starting point for most families because it focuses on protection rather than returns.

Endowment Plans (Protection + Savings)

Endowment plans combine life cover with a savings element. If the policyholder survives the policy term, a maturity amount may be paid. These plans are more expensive than term insurance because part of the premium goes toward savings.

ULIPs (Protection + Market-Linked Investment)

ULIP stands for Unit Linked Insurance Plan. A part of the premium provides life cover, and the rest is invested in market-linked funds. ULIPs can move up or down with the market, so returns are not guaranteed. They also come with charges and lock-in rules, so they need careful evaluation.

Whole Life Insurance

Whole life insurance usually provides cover for a longer period, often up to age 99 or 100, depending on the product. It can be useful for estate planning or leaving a legacy, but it is not always the most practical choice for every family.

| Type | Primary Goal | Risk Profile | Liquidity | Best For |

|---|---|---|---|---|

| Term Insurance | Family protection | Low | Low | Income replacement and loan protection |

| Endowment Plan | Protection plus savings | Low to moderate | Low | People who want a forced savings discipline |

| ULIP | Protection plus market-linked growth | Moderate to high | Moderate after lock-in | Long-term buyers who understand market risk |

| Whole Life Insurance | Long-duration protection | Low | Low | Legacy planning and long-term coverage |

How Much Life Insurance Do You Need?

Many people buy too little cover because they choose a random number. A better approach is to estimate the family’s actual financial need.

A common starting method is the Human Life Value (HLV) approach:

HLV = (Annual Income × Years to Retirement) + Existing Debt – Liquid Assets

Here is what each part means:

- Annual income: Your yearly take-home or stable income.

- Years to retirement: The number of working years left.

- Existing debt: Home loan, personal loan, education loan, or other liabilities.

- Liquid assets: Cash, savings, fixed deposits, mutual funds, or any assets your family can easily use.

Example: If someone earns ₹10 lakh a year, has 20 working years left, owes ₹15 lakh, and has ₹5 lakh in liquid assets, the rough cover need may be:

₹10 lakh × 20 + ₹15 lakh – ₹5 lakh = ₹2 crore.

This is only a rule-of-thumb example. Your actual cover may need to be higher if you have young children, large EMIs, dependent parents, or future education goals.

For many first-time buyers, a term plan with a sufficient sum assured is usually more practical than mixing insurance with investing.

Life Insurance Coverage Calculator

Simple life cover estimator: Use this as a starting point only. Actual needs depend on inflation, family lifestyle, health, existing assets, and long-term goals.

| Input | How to Use It |

|---|---|

| Annual income | Enter your yearly income |

| Current liabilities | Add loans and other debts |

| Future financial goals | Add education, marriage, or major family goals |

Recommended minimum cover formula: Annual income × 10 to 15 + current liabilities + future goals – liquid assets

Example: If annual income is ₹8 lakh, liabilities are ₹20 lakh, future goals are ₹25 lakh, and liquid assets are ₹10 lakh, the estimated cover range is:

₹8 lakh × 10 to 15 = ₹80 lakh to ₹1.2 crore

Plus ₹20 lakh + ₹25 lakh – ₹10 lakh = ₹35 lakh

Estimated cover range = ₹1.15 crore to ₹1.55 crore

This is a simplified estimation tool. Actual insurance needs vary based on lifestyle, inflation, and family goals. Consult a financial advisor for a personalized plan.

Tax Rules for Life Insurance in India

Tax treatment is one reason many people look at life insurance. But it is important to understand the rules correctly, because tax benefits depend on policy type, premium amount, and current law.

Section 80C: Deduction on Premiums Paid

Premiums paid for eligible life insurance policies can qualify for deduction under Section 80C, subject to the overall limit available under the Income Tax Act. The exact benefit depends on the tax regime you choose and the policy conditions.

Do not assume every premium is fully deductible. The policy must meet the applicable tax rules, and the deduction is available only if you are using the relevant tax framework.

Section 10(10D): Tax-Free Maturity or Death Benefit

Under Section 10(10D), the proceeds from a life insurance policy may be exempt from tax, including the death benefit. However, this exemption comes with conditions.

For some policies, especially high-premium plans and certain ULIPs, the premium-to-sum-assured ratio and other rules matter. Budget changes in recent years have tightened tax treatment for some high-value policies, so buyers should verify the latest rules before choosing a plan.

Important: Tax rules can change. Check the latest Income Tax Department guidance or speak with a qualified tax professional before relying on tax savings.

| Benefit | Section | What It Usually Covers | What to Check |

|---|---|---|---|

| Premium deduction | 80C | Eligible premiums paid | Tax regime, policy conditions, overall deduction limit |

| Maturity or death benefit | 10(10D) | Policy proceeds, subject to conditions | Premium limits, policy type, issuance date, latest tax rules |

Life insurance should not be bought only for tax saving. Protection need should come first, and tax benefit should be treated as an added advantage.

Understanding Premium Factors

Two people can buy the same sum assured and still pay different premiums. That happens because insurers price risk based on multiple factors.

- Age at entry: Younger buyers usually pay lower premiums because risk is lower.

- Health status and smoking habit: Medical issues and tobacco use can increase the premium.

- Policy tenure: Longer coverage periods may change pricing.

- Sum assured: Higher cover generally means a higher premium.

- Riders: Add-ons such as critical illness, accidental death benefit, or waiver of premium increase the cost.

Insurers may also ask for medical tests depending on age, cover amount, and health declarations. That is normal and helps the insurer assess risk properly.

Important Exclusions: When Will a Claim Be Rejected?

A careful buyer should always check exclusions. These are the situations where the policy may not pay, or may pay only under certain conditions.

- Suicide exclusion: Many policies have a suicide exclusion during the first policy year, sometimes longer depending on policy terms.

- Non-disclosure of medical facts: If a pre-existing disease or major health issue was hidden in the proposal form, the insurer may reject the claim.

- Illegal acts: Death arising from illegal activity or criminal conduct may be excluded.

- High-risk activities: Some extreme adventure sports or hazardous occupations may need extra disclosure or special coverage terms.

This is why the proposal form must be filled honestly. Insurance is a contract, not a casual purchase. If the information is incomplete, the family may face avoidable claim trouble later.

Step-by-Step Guide to Buying the Right Policy

Buying the right life insurance policy is easier when you follow a structured process instead of relying on a single advertisement or one online quote.

- Assess your family’s financial needs. Think about monthly expenses, loans, children’s education, spouse’s income, and future goals.

- Compare quotes from multiple insurers. Do not choose only because one website shows a lower premium.

- Check the insurer’s claim settlement ratio. This number is useful, but it is not the only factor. Also look at the claim process, service quality, and complaint history. If available, also check the insurer’s amount settlement ratio for a wider view of claim payment patterns.

- Disclose everything in the proposal form. Tell the truth about medical history, smoking, occupation, and existing policies.

- Read the policy bond carefully. Verify the cover amount, exclusions, riders, premium due dates, grace period, and waiting period.

- Review the Customer Information Sheet. IRDAI-mandated documents are meant to help customers understand the policy in a simple format.

Also keep the official insurer prospectus and policy wording for your records. If something is not clear, ask the insurer before buying.

What to Check Before You Buy

- Whether the policy is mainly for protection, savings, or market-linked growth.

- The sum assured is enough for your family’s real need.

- The premium fits comfortably into your budget for the full policy term.

- The policy has a clear exclusion list and waiting period details.

- The nominee details are correctly updated.

- The tax benefits are still valid under the current law and your tax regime.

- The insurer’s claim process, service quality, and policy documents are easy to understand.

For official verification, readers should check the insurer’s website, the IRDAI website, and the Income Tax Department’s latest rules where applicable.

FAQ

Is life insurance an investment or an expense?

Life insurance is primarily an expense for protection. Some policies also have a savings or investment element, but the main purpose is to provide financial cover for your family.

What happens if I stop paying my life insurance premium?

If you stop paying premiums, the policy may lapse after the grace period, and the cover may end. Some policies may offer revival options or reduced paid-up benefits, depending on the product terms.

Can I have multiple life insurance policies?

Yes, you can have multiple life insurance policies if the total cover and disclosures are properly declared. You should still disclose all existing policies in every new application.

What is the difference between a nominee and a legal heir?

A nominee is the person named in the policy to receive the claim amount. A legal heir is someone entitled under succession law. In many cases, the nominee receives the payout, but the legal treatment can depend on the situation and applicable law.

Does my company-provided group insurance cover all my needs?

Usually no. Group insurance from an employer may help, but the cover amount is often limited and may end when you leave the job. It is better to treat it as extra protection, not your only cover.

How does the claim process work for my family?

Your family should inform the insurer, submit the claim form, death certificate, policy details, and any other documents requested. The insurer then verifies the claim based on the policy terms, exclusions, and disclosures before releasing the benefit.