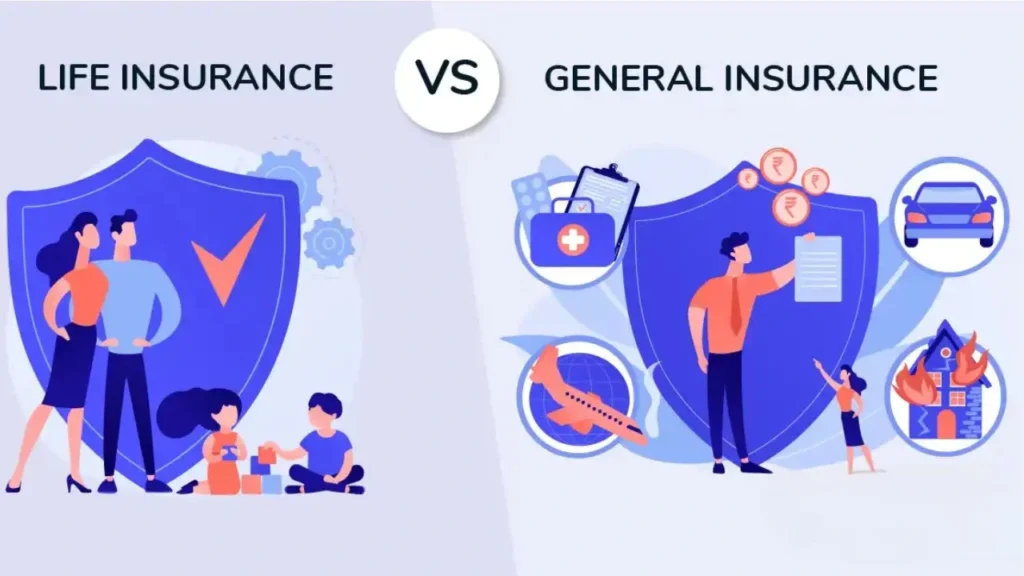

Life insurance and general insurance both protect you against financial loss, but they cover different risks. Life insurance mainly protects your family against the financial impact of your death, while general insurance covers non-life risks such as hospital expenses, vehicle damage, travel emergencies and property loss.

Understanding the difference between life insurance and general insurance can help you avoid major coverage gaps. For a broader understanding, you can first read how insurance works and how it protects people against specified financial risks.

The main difference is simple: life insurance covers risks connected with human life, while general insurance covers health, property, vehicles, travel and other non-life risks.

What Is Life Insurance?

Life insurance is a contract between an insurer and a policyholder. The insurer agrees to pay a specified benefit when a covered event connected with the insured person’s life occurs.

Depending on the policy, the benefit may be paid:

- On the death of the insured person

- When the policy reaches maturity

- At selected survival stages

- Through regular income or instalments

The person who purchases the policy is the policyholder. The person whose life is covered is the life assured. In many policies, both are the same person.

Common Types of Life Insurance

The main types include:

- Term insurance: Provides life cover for a fixed period. A standard term plan generally does not pay a maturity benefit if the insured survives the policy term.

- Whole-life insurance: Provides life cover for a long duration, subject to policy terms.

- Endowment plan: Combines life cover with a maturity or savings benefit.

- Money-back policy: Pays specified survival benefits during the policy term.

- Unit-linked insurance plan: Combines life insurance with market-linked investment.

You can compare the types of life insurance plans in India to understand how term plans, endowment policies, ULIPs and other options serve different financial needs.

Life insurance is especially important when family members depend on the policyholder’s income.

Read Also: Life Insurance vs Investment Plans: Which Option Is Better?

What Is General Insurance?

General insurance protects against financial risks that are not directly connected with the duration of a person’s life.

It can cover medical expenses, accidents, vehicle damage, property loss, travel emergencies and legal liabilities. Most general insurance policies are renewed periodically, commonly every year, although longer policy terms may be available.

Common types of general insurance include:

- Health insurance

- Motor insurance

- Home insurance

- Travel insurance

- Personal accident insurance

- Commercial insurance

- Marine insurance

- Cyber insurance

In India, health insurance may be issued by general insurers as well as standalone health insurers. It is not a form of life insurance.

Families comparing medical coverage should carefully evaluate the sum insured, waiting periods, co-payment and hospital network before choosing a suitable family health insurance plan.

Many general insurance policies work on the principle of indemnity. This means the insurer compensates an admissible financial loss up to the policy limit.

However, not every general insurance policy is strictly indemnity-based. Critical illness, personal accident and hospital cash policies may pay a predetermined benefit when a covered event occurs.

Read Also: Standalone Health Insurance Companies in India

Difference Between Life Insurance and General Insurance

The following table explains the key differences.

| Basis | Life Insurance | General Insurance |

|---|---|---|

| Primary purpose | Protects against financial risks connected with human life | Protects against health, asset, travel, accident and liability risks |

| What is covered | The life of an insured person | Health, vehicles, homes, property, travel and other non-life risks |

| Common policy duration | Often long-term | Commonly one year, although longer terms may be available |

| Claim trigger | Death, maturity or survival, depending on the policy | Covered illness, damage, accident, loss or liability |

| Claim amount | Usually a predetermined policy benefit | Usually based on admissible loss or a predetermined benefit |

| Claim recipient | Policyholder, nominee, beneficiary or legal heir | Policyholder, insured person, hospital, repairer or affected third party |

| Premium payment | Regular, limited-term or single premium | Commonly paid when purchasing or renewing the policy |

| Maturity benefit | Available only in selected life insurance plans | Generally not available |

| Savings or investment | Available in selected policies | Normally not included |

| Renewal | May continue for a long policy term if premiums are paid | Usually renewed periodically |

| Common examples | Term, whole life, endowment and ULIP | Health, motor, travel and home insurance |

The main general and life insurance difference is the type of risk covered. Life insurance deals with financial risks connected with a person’s life, while general insurance protects against non-life losses and expenses.

Life Insurance vs General Insurance: A Practical Example

Consider a 35-year-old salaried employee who supports a spouse, two children and dependent parents.

The employee may purchase a term insurance policy of ₹1 crore. If the insured person dies while the policy is active, the nominee may receive the applicable death benefit. The money can help the family manage daily expenses, repay loans and fund future goals.

The same person may also purchase:

- Health insurance to cover admissible hospital expenses

- Motor insurance for vehicle-related damage and third-party liability

- Home insurance for covered damage to the house or its contents

- Travel insurance for specified emergencies during a trip

Vehicle owners should compare coverage, deductibles, network garages and claim support before choosing suitable vehicle insurance in India.

A term plan cannot pay for a regular hospital bill or vehicle repair. Similarly, motor or health insurance cannot replace a person’s future income after death.

Life and general insurance therefore complement each other. One cannot normally replace the other.

How Do Claims Differ?

Life insurance and general insurance claims are assessed differently because the policies cover different risks.

Life Insurance Claim Process

For a death claim, the nominee or claimant generally informs the insurer and submits the required documents.

These may include:

- Claim form

- Death certificate

- Policy information

- Nominee’s identity and bank details

- Medical or hospital records, where required

- Additional documents depending on the cause of death

The insurer checks whether the policy was active, verifies the claim and reviews the information provided in the proposal form. Once the claim is accepted, the applicable policy benefit is paid according to the selected payout option.

Maturity and survival claims follow a different process. The benefit, where available, is paid to the eligible policyholder according to the policy conditions.

General Insurance Claim Process

A general insurance claim begins when the policyholder reports a covered event such as hospitalisation, vehicle damage, travel disruption or property loss.

Depending on the policy, the claimant may need to submit:

- Bills and payment receipts

- Medical records

- Repair estimates

- Surveyor reports

- Police reports

- Photographs of the damage

- Travel documents

- Proof of ownership

The insurer assesses whether the event is covered and calculates the admissible claim amount.

The approved amount may be:

- Reimbursed to the policyholder

- Paid directly to a network hospital

- Settled with an authorised repair centre

- Paid as a predetermined benefit

- Paid to an affected third party

The documents and settlement steps differ across policies. Read the complete insurance claim process to understand how to file, track and reduce avoidable claim problems.

Do You Need Both Life and General Insurance?

Many people need both because life insurance and general insurance protect against different financial risks.

Life Insurance May Be Important When:

- Your family depends on your income

- You have outstanding loans

- You have dependent parents

- You want to protect your children’s future goals

- Your savings cannot fully support your family after your death

Understanding the benefits of life insurance can help you decide whether your dependants, debts and long-term family goals require separate life cover.

A person without financial dependants may have a lower immediate need for a large term insurance policy. However, future responsibilities and outstanding liabilities should still be considered.

General Insurance May Be Important When:

- You need protection against hospital bills

- You own a vehicle

- You own a home or valuable property

- You travel frequently

- You operate a business

- You face professional or legal liability risks

The required policies depend on your individual exposure. For example, a person who does not own a vehicle may not need motor insurance, but health insurance can still be important.

Which Insurance Should You Buy First?

There is no single order that suits every person. The right priority depends on your dependants, health, assets, liabilities and legal obligations.

Prioritise Term Life Insurance When You Have Dependants

When your family relies on your earnings, adequate term insurance should be a priority. The sum assured should be sufficient to replace income, repay important debts and protect long-term family goals.

Do not choose a very low sum assured only because its premium is cheaper.

Prioritise Health Insurance for Medical Expenses

Hospital treatment can create a large and sudden expense. Health insurance can help pay admissible treatment costs according to the policy terms.

Even when you have employer-provided health insurance, personal coverage may be useful because employment benefits can change when you switch jobs, retire or become self-employed.

Maintain Required Motor Insurance

Vehicle owners must maintain the legally required third-party motor cover. Comprehensive or own-damage protection can also be considered based on the vehicle’s value and the owner’s risk exposure.

Buy Asset-Specific Insurance When Needed

Home, travel, cyber and commercial insurance should be selected according to the risks you actually face.

For example:

- A homeowner may require protection against fire and specified natural events.

- An international traveller may require medical and trip-related cover.

- A business owner may require property, liability or employee-related insurance.

The aim is not to buy every available policy. It is to identify risks that could cause a serious financial loss and insure the most important ones.

Key Points to Check Before Buying Insurance

Whether you are purchasing life insurance or general insurance, do not select a plan only because it has a low premium.

Check the following:

- Coverage provided

- Sum assured or sum insured

- Policy duration

- Exclusions

- Waiting periods

- Deductibles and co-payment

- Claim process

- Renewal conditions

- Nominee details

- Optional benefits

- Insurer’s service network

- Policy wording and Customer Information Sheet

Life insurance buyers should also check the death benefit, maturity benefit, payout option and premium-payment period.

General insurance buyers should examine policy-specific conditions such as cashless hospitals, vehicle depreciation, room-rent limits, deductibles and geographical coverage.

Life Insurance and General Insurance: Which Is More Important?

Neither category is universally more important. They solve different financial problems.

Life insurance becomes essential when your death could leave dependants without adequate financial support. General insurance becomes essential when medical costs, vehicle damage, property loss or another covered event could significantly affect your finances.

For many households, an appropriate combination may include:

- Adequate term life insurance for earning members

- Health insurance for the family

- Legally required motor insurance for owned vehicles

- Home, travel or business insurance according to actual needs

Insurance should be selected according to the size and seriousness of the risk, not simply because a product is popular.

Conclusion

The difference between life insurance and general insurance lies in their purpose, coverage and claim structure.

Life insurance protects against financial risks related to human life. It can provide a predetermined benefit on death, maturity or survival, depending on the policy. General insurance covers non-life risks such as illness, vehicle damage, accidents, travel emergencies and property loss.

Life insurance is generally long-term, while general insurance commonly requires periodic renewal. Many general insurance policies compensate an admissible loss, while life insurance usually pays a defined policy benefit.

For complete protection, most families should not view this as life insurance versus general insurance. They should identify their life, health and asset-related risks and build a suitable combination of policies.