A ₹10 lakh health insurance policy may look sufficient until one major hospitalisation uses most or all of the available cover. If another family member needs treatment during the same policy year, you could be left without enough insurance.

This is where the restoration benefit in health insurance may help. It can refill the available sum insured after a claim, giving you additional cover for eligible hospitalisations during the same policy year.

However, restoration does not work identically in every policy. It may activate after partial or complete use of the cover, apply only to future claims or come with restrictions for the same illness and insured member.

What Is Restoration Benefit in Health Insurance?

Restoration benefit in health insurance is a feature that reinstates the sum insured after it has been partially or fully used during a policy year. The restored amount can then be used for eligible subsequent claims, subject to the policy’s conditions.

This benefit may also be called:

- Restore benefit

- Refill benefit

- Recharge benefit

- Reset benefit

- Reinstatement of sum insured

Restoration may be included in the base policy or offered as an optional add-on for an additional premium.

How Does Restoration Benefit Work?

Consider a family-floater policy with the following details:

- Base sum insured: ₹10 lakh

- First hospitalisation claim: ₹10 lakh

- Remaining base cover: ₹0

- Restoration available: ₹10 lakh

After the first claim exhausts the base cover, the insurer restores ₹10 lakh. The restored amount may then be available for another eligible hospitalisation during the same policy year.

For example, if another insured family member later needs treatment costing ₹4 lakh, the claim may be paid from the restored cover, subject to the policy terms and the applicable cashless health insurance claim process.

However, restoration does not always increase the limit available for the first hospital bill.

Suppose the first admissible hospital bill is ₹15 lakh, but the policy has a base sum insured of ₹10 lakh. A restoration feature may not automatically pay the remaining ₹5 lakh under the same claim. Some policies allow restoration only for a later hospitalisation.

This is why restoration should not be treated as a replacement for an adequate base sum insured.

Types of Restoration Benefits

Restoration After Full Exhaustion

Under this structure, restoration activates only after the base sum insured and, where applicable, the accumulated bonus have been completely used.

For example, if you have ₹10 lakh of base cover and only ₹7 lakh has been used, the restoration may not activate because ₹3 lakh is still available.

This type provides less flexibility when the remaining cover is too small for another major treatment.

Restoration After Partial Exhaustion

Some policies activate restoration as soon as any part of the base cover is used.

For example:

- Base sum insured: ₹10 lakh

- First claim: ₹4 lakh

- Remaining base cover: ₹6 lakh

- Restored cover: Up to ₹10 lakh, subject to policy terms

The restored amount may form a separate pool for eligible future claims. This is generally more flexible than restoration that begins only after complete exhaustion.

One-Time Restoration

The policy restores the sum insured only once during a policy year. Once that restored amount is used, no further restoration is available until the next policy year.

Multiple or Unlimited Restoration

Some policies allow restoration more than once or advertise unlimited restoration for eligible claims.

However, “unlimited restoration” does not mean every hospital bill will be paid without limits. Waiting periods, exclusions, room-rent restrictions, co-payment, sub-limits and claim eligibility still apply.

When Can You Use the Restored Sum Insured?

The rules differ between policies. Depending on the wording, restored cover may be available:

- For a different illness

- For the same illness

- For another insured family member

- For the same insured member

- Only for a later hospitalisation

- After complete exhaustion of the base cover

- After partial use of the base cover

- Once or multiple times in a policy year

Some policies do not allow restoration for a second claim connected with the same disease or its complications. Others may permit it, including for the same insured person.

Do not depend only on phrases such as “100% restoration” or “unlimited refill.” Read the exact conditions that determine when and how the restored amount becomes usable.

When May Restoration Benefit Not Help?

Restoration may not provide the expected support in the following situations.

One Large Claim Exceeds the Base Cover

If one hospitalisation costs more than the base sum insured, restoration may not cover the excess amount under that same claim.

A ₹10 lakh policy with restoration should not automatically be treated as ₹20 lakh of cover for one hospitalisation.

Restoration Applies Only to Future Claims

Many policies make restored cover available only after the earlier claim has been settled or the base cover has been exhausted.

It may therefore be usable for a later hospitalisation, not the ongoing one.

The Second Claim Is for the Same Illness

Some policies allow restoration only for an unrelated illness. A later claim caused by the same disease or its complications may not qualify.

The Same Member Cannot Use It Again

A policy may allow restored cover for another insured family member but restrict its use by the person who made the first claim.

The Claim Falls Under a Policy Restriction

Restoration does not override the waiting period in health insurance. A disease may remain uncovered until the applicable waiting period is completed, even when restored cover is available.

Restoration also does not remove a sub-limit in health insurance. If the policy limits payment for a particular treatment, the restored amount will not automatically increase that treatment-specific limit.

Other restrictions can include:

- Permanent exclusions

- Co-payment

- Deductibles

- Room-rent restrictions

- Non-payable expenses

The claim must remain admissible under the main policy before restored coverage can be used.

The Available Restorations Have Been Used

A one-time or fixed restoration benefit stops after the permitted number of refills has been used.

Restoration in Individual and Family-Floater Policies

| Factor | Individual policy | Family-floater policy |

|---|---|---|

| Base cover | Available to one insured person | Shared by all insured family members |

| Restoration use | May support another eligible claim by the same person | May protect other members after shared cover is used |

| Main value | Helps during multiple hospitalisations in one year | Prevents one member’s claim from leaving the whole family without cover |

| Important condition | Same-illness and same-person eligibility | Same-member, same-illness and shared-cover rules |

Restoration can be particularly useful in a family floater because every insured member shares the same base sum insured.

For example, if one family member uses the entire ₹10 lakh floater, no base cover may remain for the spouse or children. Restoration can provide another pool of cover for eligible claims during that policy year.

While comparing the best health insurance plans for family, check whether restoration is available for the same insured member and the same illness. These two conditions can determine how useful the feature is during multiple hospitalisations.

Benefits of Restoration in Health Insurance

Additional Cover During the Same Policy Year

Restoration gives you another pool of coverage after the original sum insured has been used according to the policy’s trigger.

Protection Against Multiple Hospitalisations

It can be useful when the insured person or family faces more than one hospitalisation in the same year.

Stronger Family-Floater Protection

One large claim can use most of a shared family cover. Restoration may protect the remaining members from being left without insurance.

Automatic Reinstatement

Many policies restore the sum insured automatically after the specified trigger is met. You may not need to submit a separate request.

More Cover Without Immediately Increasing the Base Sum Insured

A restoration feature may provide additional protection at a lower premium than choosing a much larger base cover. However, both options serve different purposes and should be compared carefully.

Restoration mainly supports eligible later claims. A higher base sum insured provides stronger protection against one large hospital bill.

Conditions to Check Before Choosing Restoration Benefit

Do not select a policy merely because it mentions 100% or unlimited restoration. Ask these questions before buying:

- Does restoration activate after partial or complete exhaustion?

- Must the no-claim bonus also be exhausted first?

- Can restored cover be used for the same illness?

- Can the same insured person use it again?

- Can it be used during the same hospitalisation?

- Is there a waiting gap between two claims?

- How many times can restoration occur in one year?

- Is 100% of the base sum insured restored?

- Does restoration apply to all covered benefits?

- Is it built into the plan or available as a paid add-on?

- Do room-rent limits and co-payment still apply?

- Does unused restored cover expire at the end of the policy year?

The answers should be available in the policy wording, prospectus or Customer Information Sheet. Ask the insurer for written clarification if any condition is unclear.

Restoration Benefit vs No-Claim Bonus

Restoration benefit and no-claim bonus are not the same.

| Restoration benefit | No-claim bonus |

|---|---|

| Reinstates cover after eligible claims | Rewards claim-free policy years |

| Generally works within the same policy year | Usually applies at renewal |

| Triggered by utilisation of the sum insured | Triggered by not making a claim |

| Usually does not carry forward if unused | May accumulate according to policy terms |

| Supports eligible subsequent claims | Increases cover or reduces premium, depending on the policy |

A health policy may offer both benefits.

For example, a ₹10 lakh policy may have accumulated a ₹5 lakh no-claim bonus, giving a total available cover of ₹15 lakh. The restoration may activate only after this entire ₹15 lakh has been used, depending on the policy conditions.

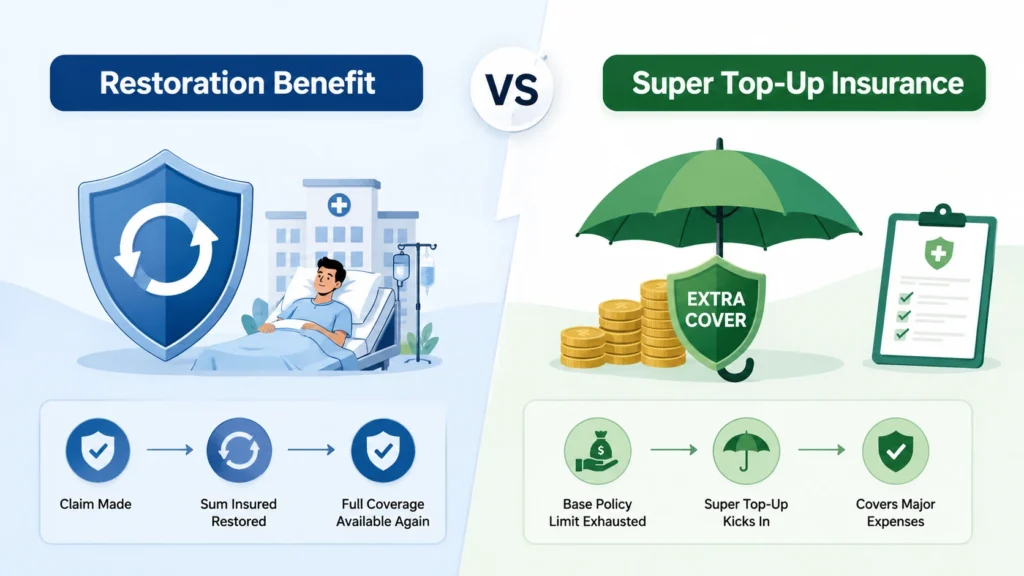

Restoration Benefit vs Super Top-Up Insurance

Restoration and super top-up health insurance both provide additional protection, but they work differently.

Restoration refills the cover according to the conditions of the base policy. A super top-up is a separate policy that becomes payable after cumulative eligible medical expenses cross a chosen deductible during the policy year.

A super top-up may be more helpful when:

- One large claim can exceed your base cover

- You want substantially higher overall protection

- You are willing to manage a deductible

Restoration may be more useful when:

- You are concerned about multiple hospitalisations

- Several family members share one floater

- The policy offers flexible partial-use restoration

- The benefit is included without a major premium increase

Many families may benefit from combining an adequate base policy, practical restoration and a suitable super top-up.

Is Restoration Benefit Worth It?

Restoration benefit can be valuable, especially for:

- Family-floater policyholders

- Families with several insured members

- Buyers concerned about repeated hospitalisations

- People with a moderate base sum insured

- Policies that restore cover after partial use

- Plans that allow the same illness and same member

However, restoration is not enough on its own.

A higher base cover may be more useful when your main concern is one expensive treatment. Restoration may not help if the first claim itself exceeds the original sum insured and the policy allows restored cover only for later claims.

Compare the premium difference between:

- A lower base cover with restoration

- A higher base cover

- A base cover with a super top-up

- A policy offering both restoration and a super top-up

Choose the structure that provides adequate protection without depending on conditions that may be difficult to meet.

Read Also: How to Choose the Best Health Insurance Company in India

Conclusion

Restoration benefit in health insurance refills the sum insured after it has been partially or completely used, depending on the policy terms. It can protect you against eligible subsequent claims during the same policy year.

The feature is particularly useful in family-floater policies, where one member’s hospitalisation can use most of the shared cover.

However, restoration is not automatically available for the same illness, same person or same hospitalisation. It also does not override waiting periods, exclusions, co-payment or sub-limits.

Before buying, check the restoration trigger, amount, frequency and claim eligibility. Most importantly, choose an adequate base sum insured instead of depending entirely on restoration.

Read Also: Insurance Claim Process: How to File, Track and Avoid Rejection