General insurance is a non-life financial protection tool that helps you manage losses linked to health, vehicles, home, travel, and other assets. It does not pay a death benefit like life insurance. Instead, it helps cover the cost of a specific loss, damage, or medical expense, depending on the policy terms.

For Indian households, general insurance can be an important part of financial planning because one unexpected event can create a large expense. A hospital bill, a car accident, or a house fire can disrupt savings quickly. That is why understanding how general insurance works, what it covers, and how claims are processed is so useful before you buy a policy.

Understanding General Insurance: The Basics

General insurance is usually a contract for a fixed policy term, often one year, although some products may have different durations. You pay a premium to an insurer, and in return the insurer promises to compensate you for covered losses as per the policy wording, subject to exclusions, limits, and conditions.

General insurance is usually a contract for a fixed policy term, often one year, although some products may have different durations. You pay a premium to an insurer, and in return the insurer promises to compensate you for covered losses as per the policy wording, subject to exclusions, limits, and conditions.

Two basic terms matter most:

- Premium: The amount you pay to keep the policy active.

- Sum insured: The maximum amount the insurer will pay for a covered claim, unless the policy has a different structure such as a fixed benefit.

The idea behind general insurance is simple: you transfer a financial risk to the insurer. Instead of bearing the full cost of an uncertain event on your own, you pay a known premium and get protection against specified risks.

Another important concept is the principle of indemnity. In many general insurance policies, the goal is to restore you to the financial position you were in before the loss, not to create a profit. For example, if a covered car repair costs ₹40,000 and the policy conditions are met, the insurer may pay the eligible amount after deductibles, depreciation, and policy limits are applied. The claim is meant to compensate the loss, not give extra money.

Why General Insurance Is Essential for Your Financial Plan

General insurance matters because it protects your savings from sudden, high-cost events. Most families can handle routine expenses, but a major hospitalisation or accidental damage can strain a budget. A good policy works like a safety net.

It also supports risk transfer. Instead of keeping the full financial burden of a health emergency, vehicle accident, or home damage, you shift that burden partly or fully to the insurer, depending on the coverage and conditions. This can help you keep long-term goals like emergency savings, education planning, and retirement planning on track.

In India, general insurance is also regulated by the Insurance Regulatory and Development Authority of India (IRDAI). IRDAI sets rules for insurers, policy disclosures, grievance handling, and policyholder protection. That regulatory oversight is one reason policy wording, exclusions, and claim procedures are standardized to a meaningful extent across the industry, even though product features still vary by insurer.

Common Types of General Insurance in India

When people search for general insurance, they often mean the main non-life products sold in India. The most common categories are health, motor, home/property, travel, and personal accident insurance.

When people search for general insurance, they often mean the main non-life products sold in India. The most common categories are health, motor, home/property, travel, and personal accident insurance.

Health Insurance

Health insurance helps pay for hospitalisation and other eligible medical expenses, depending on the plan. Many policies may cover room rent, surgery, doctor consultation, medicines during hospital stay, day-care procedures, and emergency treatment, but the exact list varies widely.

Health insurance policies often include waiting periods for pre-existing diseases, maternity benefits, or certain specified treatments. So the cheapest premium is not always the best choice if the policy has strong exclusions or restrictive limits.

Motor Insurance

Motor insurance is designed for vehicles such as cars, two-wheelers, and commercial vehicles. In India, third-party motor insurance is mandatory for vehicles using public roads, as required under the Motor Vehicles Act and related rules. This covers liability for injury, death, or property damage caused to a third party.

A comprehensive policy usually includes third-party cover plus own-damage protection for your vehicle, subject to policy terms. Add-ons may be available for benefits like zero depreciation, engine cover, or roadside assistance.

Property and Home Insurance

Home insurance can protect the structure of the house, household contents, or both. It may cover risks such as fire, theft, burglary, natural disasters, or accidental damage, depending on the policy. This can be especially useful for homeowners with expensive furniture, appliances, or electronics.

Property cover is often overlooked, but a single incident like fire or flooding can cause major losses. The policy wording usually defines what counts as “contents” and what kinds of events are covered.

Travel and Personal Accident Insurance

Travel insurance is designed to protect against trip-related risks such as medical emergencies abroad, baggage loss, trip cancellation, or delayed flights, depending on the plan. Personal accident insurance provides financial protection for accidental death, disability, or injury caused by an accident.

These policies are useful for short-term risks and can be helpful when you travel frequently or have work that involves higher accident exposure.

What Is Covered vs. What Is Not

Many beginners assume general insurance covers “everything related to the insured item.” That is not how it works. Every policy has inclusions, exclusions, conditions, and waiting periods.

Common inclusions are events or expenses that the policy is designed to cover. For example, a health policy may cover hospitalisation, while a motor policy may cover accident damage and third-party liability.

Common exclusions are situations the insurer will not pay for. These may include:

- Pre-existing issues during the waiting period in health insurance

- Wear and tear or normal depreciation

- Intentional damage or fraud

- Driving without a valid licence in motor insurance

- Losses specifically excluded in the policy wording

Waiting periods are also important. A policy may start immediately, but certain benefits may become available only after a set period. This is common in health insurance for specific diseases or pre-existing conditions.

Always read the policy wording, benefits table, and exclusions list. General insurance is a contract of utmost good faith, which means you must disclose material facts correctly. If you hide an existing illness, previous claim history, vehicle modifications, or other relevant details, a claim can be reduced or rejected later.

General Insurance Coverage & Exclusions Table

Policy wordings vary by insurer. Always read the Product Disclosure document before buying.

| Insurance Type | Common Inclusions | Common Exclusions |

|---|---|---|

| Health Insurance | Hospitalisation, surgeries, day-care procedures, ambulance cover, pre/post-hospitalisation expenses as per policy | Waiting period items, cosmetic treatment, self-inflicted injury, non-covered treatments, policy-specific exclusions |

| Motor Insurance | Accident damage, theft, fire, third-party liability, eligible add-ons | Normal wear and tear, driving without valid licence, drunk driving, illegal use, excluded parts or benefits |

| Home Insurance | Fire, burglary, natural calamities, accidental damage, contents cover if selected | Gradual damage, poor maintenance, specific uninsured valuables, policy-defined exclusions |

The Claim Process: How It Actually Works

The claim process in general insurance depends on the type of policy, but the broad steps are similar. First, you inform the insurer as soon as possible after the event. Then you submit the required documents, follow the insurer’s claim process, and wait for assessment and approval.

In some claims, the insurer may appoint a surveyor or claims assessor. This is common in motor and property claims where damage has to be evaluated. In health insurance claims, the hospital network, insurer, and TPA may coordinate the claim based on the type of settlement.

A simple claim flow often looks like this:

- Inform the insurer or insurer’s claims team.

- Register the claim with policy details and event information.

- Submit documents such as bills, reports, FIR copy if needed, photos, prescriptions, or repair estimates.

- Allow inspection or assessment if the insurer requests it.

- Wait for approval, settlement, or query resolution.

- Receive payment or direct settlement as per the claim type.

Time limits, document requirements, and claim procedures can vary. That is why it helps to save the policy document, claim helpline details, and digital copy of your insurance papers in advance.

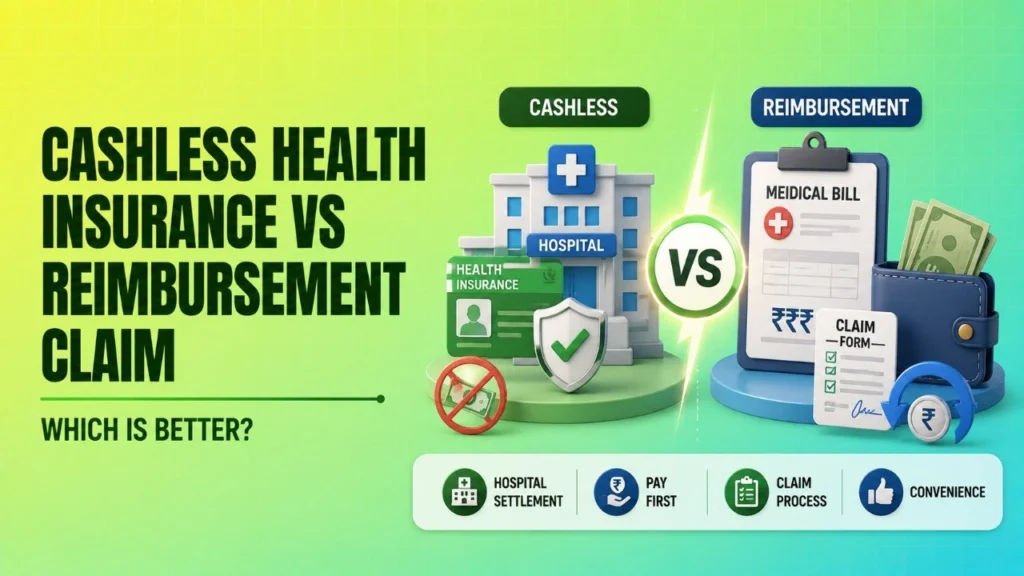

Cashless vs. Reimbursement Claims

This is one of the most confusing parts for beginners, especially in health insurance.

Cashless claim means the insurer pays the eligible hospital bill directly to the network hospital, subject to policy terms and approval. You may still need to pay non-covered items, deductibles, or expenses outside the policy scope.

Reimbursement claim means you pay the bill first and then claim the eligible amount from the insurer later by submitting documents. This method is common when you use a non-network hospital or when cashless approval is not available.

For example, if you are admitted in a network hospital, cashless treatment may reduce upfront stress. If you go to a non-network hospital or have an emergency where cashless approval is delayed, reimbursement may be the route.

The Role of Third-Party Administrators (TPAs)

In health insurance, a TPA or Third-Party Administrator may help manage the claim servicing process for the insurer. TPAs handle tasks such as claim documentation, authorisation support, network coordination, and claim processing support, depending on the insurer’s model.

TPAs are not the insurer. The insurance company remains responsible for the policy and the final claim decision. For policyholders, the practical point is to check the TPA network and the list of network hospitals before buying a policy or during renewal. This can save time later, especially for cashless hospitalisation.

For motor insurance, a similar practical check is the insurer’s garage network if you want smoother repair processing and cashless facility where available.

Key Factors to Consider Before Buying a Policy

Choosing a general insurance policy is not just about paying the lowest premium. A lower premium can sometimes mean lower coverage, higher deductibles, more exclusions, or stricter sub-limits.

Here is a simple checklist to review before buying:

- Claim settlement ratio: Check how the insurer handles claims over time, but do not use this as the only factor.

- Network hospitals or garages: Especially important if you want cashless service.

- Coverage limits: Look at sum insured, sub-limits, room rent limits, and specific disease or repair caps.

- Deductibles or voluntary excess: Know how much you must pay out of pocket before the insurer pays.

- Exclusions and waiting periods: Read these carefully to avoid surprise rejections.

- Policy wording: The product brochure is not enough; read the actual wording or product disclosure document.

- Renewal terms: Check whether the policy can be renewed smoothly and whether benefits continue with renewal.

A practical comparison table can help you judge policies quickly:

| Insurance Type | Primary Goal | Coverage Focus | Key Exclusions or Check |

|---|---|---|---|

| Health Insurance | Manage medical expenses | Hospitalisation and related eligible treatment costs | Waiting periods, room rent limits, network hospitals, pre-existing disease terms |

| Motor Insurance | Protect vehicle and liability | Third-party cover and own-damage cover | Driving conditions, add-on limits, IDV, garage network, depreciation terms |

| Home Insurance | Protect house and contents | Fire, theft, natural calamities, accidental damage | Content limits, valuation method, maintenance-related losses, item-specific exclusions |

These checks are especially useful in India because policy designs vary a lot across general insurance companies in India. Two plans with the same premium may have very different features.

A Simple Way to Compare General Insurance Policies

If you are comparing a general insurance company’s product with another, focus on the policy document rather than only the marketing page. Ask four simple questions:

- What exactly is covered?

- What is excluded or limited?

- How does the claim process work?

- What will I have to pay out of pocket even after buying the policy?

This approach works better than just searching for the lowest premium. A policy with slightly higher premium can be more useful if it has wider coverage, fewer restrictions, and better claim support.

If you are wondering how many insurance company in India there are, the number can change as new insurers enter the market or existing ones merge or restructure. For the latest count, it is best to check the official IRDAI website rather than relying on old lists. That is also the safest way to identify licensed insurers.

Also remember that a policy’s usefulness depends on your needs. A family with children may prioritise health insurance. A car owner may focus on motor insurance. A homeowner may need property protection. A frequent traveller may need travel cover more often than others.

General insurance does not replace emergency savings. It supports them. Even with a good policy, you may still face deductibles, excluded items, waiting periods, or temporary out-of-pocket costs before reimbursement or settlement.

For Indian buyers, the most practical habit is to keep policy documents, claim numbers, renewal reminders, and hospital or garage network details in one safe place. That makes the claim journey much easier if something goes wrong.

FAQs

How is General Insurance different from Life Insurance?

General insurance covers financial losses from health issues, accidents, vehicle damage, travel problems, or property damage. Life insurance provides a death benefit to nominees if the insured person dies during the policy term. The purpose is different: general insurance protects against specific losses, while life insurance protects dependents financially after death.

Is it mandatory to have General Insurance in India?

Not all general insurance is mandatory, but third-party motor insurance is mandatory for vehicles used on public roads in India. Health, home, and travel insurance are usually optional, though they are highly useful for financial protection.

Can I claim insurance from two different companies for the same loss?

In some cases, yes, but you cannot make a profit from the same loss. General insurance follows the principle of indemnity and contribution. If two policies cover the same loss, the insurers may share the claim as per policy terms and applicable rules. The claim amount is usually limited to the actual loss, subject to policy conditions.

What happens if my claim is rejected?

If a claim is rejected, first ask the insurer for the reason in writing and check the policy wording. If you believe the rejection is unfair, you can raise a grievance with the insurer, escalate it through the insurer’s grievance redressal process, and then approach IRDAI’s grievance platform, including Bima Bharosa, if needed. Keep all documents and communication records ready.

Does General Insurance provide tax benefits?

Some health insurance premiums may qualify for tax deduction under Section 80D of the Income Tax Act, subject to the applicable rules. Not all general insurance policies qualify for tax benefits. Tax rules can change, so check the latest Income Tax Department guidance or ask a tax professional before relying on any deduction.