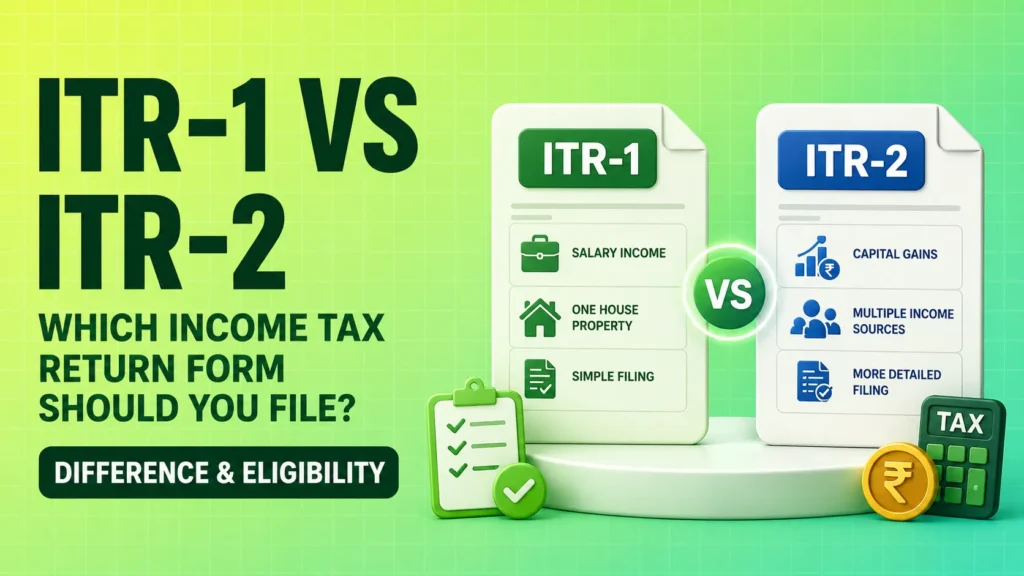

Choosing the correct income tax return form is one of the first important steps in income tax return filing. Many salaried taxpayers, pensioners, investors and first-time filers get confused between ITR-1 and ITR-2 because both forms are used by individuals, but they are not meant for the same income situation.

The main difference in ITR 1 vs ITR 2 is simple: ITR-1 is for a simpler income profile, while ITR-2 is for taxpayers with more detailed income reporting needs, such as capital gains, foreign assets, foreign income, or more complex house property details. If you select the wrong form, your return may be treated as defective, or you may have to file a revised return later.

This guide explains who should file income tax return using ITR-1, who should move to ITR-2, what documents are needed, how the income tax return filing procedure works online, and what to do if you make a mistake. This is educational information, not personalized tax advice. Tax rules, due dates and ITR utilities can change every assessment year, so always verify the latest details from the official Income Tax Department portal or consult a qualified tax professional.

What is ITR-1?

ITR-1, also called Sahaj, is a simplified income tax return form for individual taxpayers with a relatively straightforward income profile. It is commonly used for income tax return file for salaried employee cases where income mainly comes from salary or pension, one simple house property, and other sources such as savings account interest or fixed deposit interest.

In general, ITR-1 is meant for a resident individual whose total income is within the prescribed limit, commonly up to ₹50 lakh, and whose income does not require detailed schedules such as capital gains, foreign assets, business income, or professional income.

For most beginner taxpayers, ITR-1 may fit if the income sources are simple and easy to match with Form 16, AIS, TIS and bank interest details. It is often the first form salaried employees see on the e-filing portal because the portal may auto-suggest a form based on available data. Still, auto-suggestion should not be followed blindly.

You should check ITR-1 eligibility carefully before choosing it. A taxpayer may generally consider ITR-1 when:

- The taxpayer is a resident individual.

- Income is mainly from salary or pension.

- Total income is within the limit allowed for ITR-1.

- Income from house property is simple and allowed under the current assessment year instructions.

- Other income is mainly interest, family pension or similar allowed sources.

- Agricultural income, if any, is within the permitted limit.

ITR-1 is not suitable for everyone. You generally cannot use ITR-1 if you have business or professional income, taxable capital gains that need detailed reporting, foreign assets, foreign income, income from more complex property situations, or if you are a director in a company. Current assessment year forms may add or change specific conditions, so always check the latest ITR-1 instructions before filing.

What is ITR-2?

ITR-2 is a more detailed income tax return filing type for individuals and Hindu Undivided Families who are not eligible for ITR-1 and do not have income from business or profession. It covers a wider range of income situations and requires more information than ITR-1.

In simple words, if your income is not business income but is more complex than normal salary and interest income, ITR-2 may be the correct form.

ITR-2 is commonly used when a taxpayer has capital gains from shares, mutual funds, property or other assets. It is also used where the taxpayer has foreign assets, foreign income, multiple house property details, income above the ITR-1 limit, or other reporting requirements that ITR-1 does not support.

Taxpayers should choose ITR-2 when they need detailed schedules for:

- Capital gains from listed shares, equity mutual funds, debt funds, property or other assets.

- More detailed house property reporting.

- Foreign assets or foreign income reporting.

- Income above the limit allowed for ITR-1.

- A status or income condition that makes them ineligible for ITR-1.

ITR-2 is not for taxpayers with income from business or profession. Such taxpayers may need ITR-3 or another applicable form depending on their income type. This is why understanding types of income tax return filing is important before starting the return.

Difference Between ITR-1 and ITR-2

The easiest way to understand ITR 1 vs ITR 2 is to compare the income profile each form supports. ITR-1 is for simpler cases, while ITR-2 is for broader reporting where the taxpayer still does not have business or professional income.

| Point | ITR-1 | ITR-2 |

|---|---|---|

| Eligibility | Mainly for resident individuals with simple income sources. | For individuals and HUFs not eligible for ITR-1 and without business or professional income. |

| Income limit | Generally used where total income is within the ITR-1 limit, commonly ₹50 lakh, subject to current form rules. | Used when income exceeds the ITR-1 limit or the taxpayer has income details not allowed in ITR-1. |

| Capital gains | Usually not suitable for detailed capital gains reporting. | Suitable for reporting capital gains from shares, mutual funds, property and other assets. |

| Foreign assets | Not suitable for reporting foreign assets or foreign income. | Suitable where foreign assets or foreign income reporting is required. |

| Number of house properties | Used for simple house property cases allowed under current instructions. | Used when house property reporting is more detailed or not allowed in ITR-1. |

| Suitable taxpayers | Salaried employees, pensioners and simple-interest-income taxpayers. | Investors, high-income taxpayers, taxpayers with capital gains, foreign assets, foreign income or more detailed reporting needs. |

A practical rule is this: if your income details fit easily from Form 16, bank interest and basic deduction details, ITR-1 may be enough. If you sold shares, mutual funds, land, house property, have foreign assets, or crossed the allowed limit, check ITR-2 first.

Who Should File ITR-1?

ITR-1 is usually suitable for salaried employees and pensioners with a simple income structure. If you are wondering how to file income tax return for salaried person, the form often starts with Form 16. Form 16 gives salary, tax deducted by employer, exemptions and deductions reported through payroll. While checking Form 16, salaried employees should also review their PF in salary, because EPF deduction can affect monthly take-home salary, CTC breakup, retirement savings, and tax-saving calculation.

You may consider ITR-1 if you are a salaried employee with no capital gains, no foreign assets, no business income and no complex income reporting. For example, a person earning salary from one employer, interest from savings account, and fixed deposit interest may generally have a simple return profile.

ITR-1 may also work for pensioners who receive pension as salary income and have interest income. Many retired taxpayers use ITR-1 when their income sources are limited and they do not have capital gains or foreign asset reporting.

Before you file income tax return using Form 16, match the salary details with AIS and Form 26AS. Employers may deduct TDS, but the taxpayer is still responsible for checking whether all income is included correctly. Bank interest, FD interest, rental income, dividend income and capital gains may not always be fully captured in Form 16.

Do not choose ITR-1 only because it looks easier. The correct filing type in income tax return depends on your actual income sources and reporting requirements, not just your job type.

Who Should File ITR-2?

ITR-2 becomes important when your income is more than a simple salary or pension case. If you are a salaried person but you sold shares, mutual funds, property, gold or other assets during the financial year, you may need to report capital gains. That can move you from ITR-1 to ITR-2.

You should check ITR-2 if you have capital gains from stocks or property. For example, if you sold equity shares and earned short-term capital gains, or sold a plot and earned long-term capital gains, ITR-2 is generally more appropriate because capital gains need detailed schedules.

ITR-2 may also be mandatory if you have foreign assets or foreign income. This can include foreign bank accounts, foreign company shares, overseas ESOPs, foreign retirement accounts or income earned outside India. Foreign asset reporting is a sensitive area, so taxpayers should not guess. If you are unsure, consult a tax professional.

Taxpayers with more than one house property or complex house property details should also check ITR-2 eligibility. A person may have a self-occupied house and another property given on rent, or may have home loan interest, rental income and municipal tax details that require proper reporting.

High-income individuals who cross the ITR-1 income limit should not use ITR-1. Even if the income is only salary, the form eligibility limit matters.

Mandatory filing of income tax return can also apply due to specific conditions, even where tax payable seems low. Such conditions may change, so verify the latest rules from the Income Tax Department before deciding who is not required to file income tax return.

Documents Required for Filing Income Tax Return

Keeping documents ready before filing saves time and reduces mistakes. The documents required for filing income tax return depend on your income sources. A salaried taxpayer using ITR-1 may need fewer documents, while an investor filing ITR-2 may need capital gains statements and asset details.

Important documents include:

- PAN Card

- Aadhaar Card

- Form 16

- Bank statements

- AIS and TIS

- Form 26AS

- Capital gains statements

- Deduction proofs

A common mistake is filing only from Form 16 and ignoring AIS/TIS. Form 16 covers salary information from the employer, but AIS/TIS may show other income such as savings interest, FD interest, dividends and securities transactions.

How to File Income Tax Return Online Step by Step

The online income tax return filing step by step process is available through the official Income Tax e-filing portal. The exact screen names can change, but the broad income tax return filing procedure remains similar for most individual taxpayers.

Steps to file ITR online:

- Login to the Income Tax Portal.

- Select the correct Assessment Year.

- Choose the correct ITR form.

- Enter income details.

- Verify deductions.

- Match AIS, TIS and Form 26AS.

- Validate and submit return.

- E-verify return.

For beginners, the safest habit is to download the filed ITR acknowledgement, save the computation, and keep copies of supporting documents. This helps if you receive a notice, need a loan, apply for a visa or file a revised return later.

Last Date for Filing Income Tax Return

The last day to file income tax return depends on the taxpayer category and assessment year. For many individual taxpayers who are not required to get accounts audited, the standard due date is usually 31 July of the relevant assessment year. However, the government may extend the filing income tax return last date in some years.

Due dates matter because filing after the due date can lead to late fee, interest, delayed refund and restrictions on carrying forward certain losses.

Do not rely only on old searches such as income tax return filing date 2024, because due dates are assessment-year specific. Always check the latest filing date on the official Income Tax Department portal, especially close to the deadline.

Penalty for Late Filing of Income Tax Return

The penalty for late filing of income tax return is mainly discussed under Section 234F. In many cases, the late filing fee can be up to ₹5,000 if the return is filed after the due date. If total income does not exceed ₹5 lakh, the late filing fee is generally lower, commonly ₹1,000.

This late fee for filing income tax return is not the only cost of delay. If there is unpaid tax, interest may also apply. A delayed return can also delay refund processing. In some cases, losses may not be allowed to be carried forward if the return is not filed within the due date.

Belated filing of income tax return is possible within the permitted time limit, but it is better not to treat it as a normal option. Timely filing gives more time to correct errors, claim eligible refunds and respond to any mismatch properly.

How to File Revised Income Tax Return

If you select the wrong ITR form or make a mistake after submission, you may need revised income tax return filing. A revised return is used to correct mistakes in a return that has already been filed.

Common mistakes include missing bank interest, wrong deduction, wrong ITR form, incorrect capital gains or mismatch with AIS.

To file a revised income tax return:

- Login to the official Income Tax e-filing portal.

- Select the relevant assessment year.

- Choose the revised return option.

- Select the correct ITR form.

- Correct the income, deduction, tax payment or disclosure details.

- Validate the return and submit it.

- E-verify the revised return.

Do not file a revised return casually without understanding the error. If the issue involves capital gains, foreign assets, tax notices or large mismatches, consider professional help.

Benefits of Filing Income Tax Return

Filing an income tax return is not only about tax compliance. Even when tax has already been deducted through TDS, filing the return can create a clear income record. This record can be useful in many financial situations.

One major benefit of filing income tax return is loan documentation. Banks and lenders may ask for ITR copies while checking income stability for home loans, business loans, personal loans or vehicle loans.

Filing ITR does not guarantee loan approval, because approval depends on lender policy, credit profile, income, documents and repayment history. But ITR can work as formal income proof.

ITR copies may also help in visa applications where proof of income and financial stability is requested. Another benefit is refund processing. If excess TDS has been deducted, the refund can generally be processed only after filing and verifying the return.

Benefits of filing income tax return in India can include:

- Income proof for loan applications.

- Supporting document for visa or financial verification.

- Claiming eligible refund of excess TDS.

- Maintaining a formal financial record.

- Carrying forward eligible losses where allowed and filed within time.

- Reducing the risk of non-filing notices where filing is mandatory.

Conclusion

The ITR 1 vs ITR 2 decision depends on your income sources, not just whether you are salaried. ITR-1 is generally suitable for simple resident individual cases such as salary, pension and basic interest income within the permitted limit. ITR-2 is more suitable when you have capital gains, foreign assets, foreign income, more detailed house property reporting, or income conditions that make you ineligible for ITR-1.

Before filing, check Form 16, AIS, TIS, Form 26AS, bank statements and investment statements. If there is any capital gains transaction, foreign asset, high income or mismatch, do not rush to file ITR-1 just because it looks easier.

Tax rules, ITR forms, due dates and portal utilities can change. For the latest income tax return filing guide, verify details from the official Income Tax Department portal or take help from a qualified tax professional.

FAQs

1. What is the main difference between ITR-1 and ITR-2?

The main difference is eligibility. ITR-1 is for simple income profiles such as salary, pension and basic interest income within the allowed limit. ITR-2 is for individuals or HUFs with more complex income such as capital gains, foreign assets, foreign income or other details not allowed in ITR-1.

2. Can a salaried employee file ITR-2?

Yes, a salaried employee can file ITR-2 if they are not eligible for ITR-1. For example, if the employee has capital gains from shares, mutual funds or property, foreign assets, foreign income, or income above the ITR-1 limit, ITR-2 may be required.

3. Can I file ITR-1 if I have capital gains?

Generally, ITR-1 is not used for detailed capital gains reporting. If you sold shares, mutual funds or property, review ITR-2 eligibility carefully.

4. What happens if I choose the wrong ITR form?

If you choose the wrong ITR form, your return may be considered defective, or you may need to file a revised return. If you receive a notice, respond within the time mentioned in the notice and correct the issue properly.

5. Is it mandatory to file income tax return if TDS is already deducted?

TDS deduction does not automatically remove the need to file ITR. If your income crosses the applicable limit or mandatory filing conditions apply, you should file your return. Filing may also be needed to claim a refund of excess TDS.