A salaried person usually needs a loan for simple reasons: medical expense, rent gap, credit card payment, home repair, travel, or an urgent family need.

The best loan app is the one that shows the lender name, loan amount, APR, processing fee, EMI, tenure, late fee, and complaint details before you accept the loan. RBI’s digital lending rules apply to digital loans given through apps and online platforms, including mobile banking apps when they meet the definition of digital lending apps.

For salaried users, a good loan app should do 3 things well: approve the loan quickly, keep the total cost clear, and disburse money through a bank or NBFC-backed process.

Best loan apps for salaried persons in India

Here are some popular loan apps salaried users can compare before applying.

| Loan app | Best for | Loan amount | Interest / APR range | Tenure | Key point |

|---|---|---|---|---|---|

| Moneyview | Fast personal loan | ₹5,000 to ₹10 lakh | Starting 14% p.a. | Up to 5 years | Requires salaried or self-employed income, ₹25,000+ household income, and 650+ CIBIL as per its site. |

| Fibe | Digital personal loan | Up to ₹10 lakh | APR starting 18% | 6 to 36 months | Processing fee starts from 2% plus GST, foreclosure charges are nil as per Fibe’s fee page. |

| KreditBee | Small to mid-size instant loans | ₹6,000 to ₹10 lakh | Depends on lender and profile | 6 to 60 months | KreditBee says loan approval is done by RBI-registered NBFCs or banks, with direct bank transfer. |

| Navi | Larger personal loan | Up to ₹20 lakh | 9.9% to 45% p.a. | Up to 72 months | Navi lists nil foreclosure fee on its personal loan page. |

| CASHe | Salaried short-term loan | ₹15,000 to ₹3 lakh | 1.667% to 3% per month, based on tenure | 90 to 540 days | CASHe lists 2.5% processing fee for its loan products. |

| PaySense | EMI-based personal loan | Up to ₹5 lakh | 1.4% to 2.3% per month | 3 to 60 months | PaySense states monthly interest rate of 1.4% to 2.3% on personal loans. |

| Finnable | Salaried professionals | Up to ₹10 lakh | Check app before applying | Depends on offer | Finnable positions its loan product for salaried professionals and mentions loan in 60 minutes. |

Rates and fees can change. Always check the app’s latest Key Fact Statement before accepting the loan.

What is the best loan app for salaried person?

The best loan app for a salaried person is one that matches your salary, credit score, EMI capacity, and repayment timeline.

For example, if you have a salary account with a bank, check your bank app first. Salary account users may get pre-approved personal loans with lower paperwork.

If you need a small emergency loan, apps like KreditBee, Moneyview, Fibe, CASHe, PaySense, and Finnable may be useful. If you need a larger amount, compare Navi, bank apps, and NBFC apps before applying.

The useful rule is simple: compare APR, not only interest rate. RBI says APR may be disclosed at origination in the KFS format, and revised APR should be shared if the floating rate changes.

Why salaried people use loan apps

Loan apps became popular because they reduce paperwork.

A salaried person can usually apply with PAN, Aadhaar, salary proof, bank statement, selfie, and basic employment details. Many apps check eligibility in minutes.

Loan apps are also useful when the user does not want to visit a branch. Some apps disburse money directly to the bank account after approval.

KreditBee mentions 100% online process, 10-minute disbursal, and direct bank transfer. Moneyview says users can check eligibility in 2 minutes and get money directly into the bank account after approval.

How to choose the best loan app

Check the lender name

A safe loan app should clearly show who is giving the loan.

The app may be a fintech platform, but the actual loan should come from a bank or RBI-registered NBFC. KreditBee, for example, says it facilitates loan transactions between borrowers and personal loan providers such as RBI-registered NBFCs or banks.

Avoid any app that hides the lender name.

Compare APR

APR is the annual cost of the loan. It gives a better view than a monthly interest number.

Example: CASHe’s rates are monthly. PaySense also shows monthly rates. A monthly rate can look small, but the annual cost can be high.

Before accepting, check:

- APR

- EMI

- processing fee

- GST

- late fee

- bounce charge

- foreclosure rule

- cooling-off period

Check processing fee

A loan with a low interest rate can still become expensive if the processing fee is high.

Fibe lists processing fees starting from 2% of the loan amount plus GST. Moneyview lists processing fee or facilitation charges starting from 2% of the approved loan. CASHe lists 2.5% processing fee for its loan products.

Check late payment charges

Late payment has 2 costs.

You pay a penalty, and your credit score may suffer.

Fibe lists late payment charges as ₹500 plus GST or 3% of the total loan amount, whichever is higher as per the overdue amount. CASHe states delayed interest of 3% per month after the grace period if EMI remains unpaid.

Check foreclosure rules

Foreclosure means closing the loan before the full tenure.

This matters when you get a bonus, salary hike, or extra cash and want to close the loan early.

Fibe lists nil foreclosure charges. Navi also lists nil foreclosure fee. Moneyview says foreclosure is allowed only after a minimum number of EMIs, depending on tenure.

App-wise details for salaried users

Moneyview personal loan app

Moneyview can suit salaried users who want a fully digital personal loan.

Moneyview lists loan amounts from ₹5,000 to ₹10 lakh, interest starting from 1.16% per month or 14% annually, and repayment options up to 5 years. Its eligibility page mentions age 21 to 57 years, salaried or self-employed status, ₹25,000+ monthly household income, bank account salary credit, and 650+ CIBIL score.

Good for: salaried users with regular bank credits and decent CIBIL.

Check before applying: processing fee, foreclosure condition, and final APR.

Fibe personal loan app

Fibe is suitable for salaried people who want a digital personal loan with short to medium tenure.

Fibe lists personal loan interest rates starting from 18% p.a. on reducing balance, APR starting from 18%, tenure of 6 to 36 months, and processing fee starting from 2% plus GST. It also lists nil foreclosure charges.

Good for: salaried users who want a quick online loan and prefer shorter tenure.

Check before applying: late payment charges and final APR.

KreditBee loan app

KreditBee is popular for small and mid-size personal loans.

The website lists loan amounts from ₹6,000 to ₹10 lakh, 100% online process, 10-minute disbursal, and direct bank transfer. It also says all loan applications are approved and sanctioned by RBI-registered NBFCs or banks.

Good for: users who need a smaller loan quickly.

Check before applying: lender name, final interest rate, processing fee, and repayment date.

Navi personal loan app

Navi can suit users who need a larger personal loan and have a strong credit profile.

Navi lists personal loan amount up to ₹20 lakh, interest rate from 9.9% to 45% p.a., nil foreclosure fee, and tenure up to 72 months.

Good for: salaried users who want a higher loan amount and longer tenure.

Check before applying: final rate, processing charge, and EMI comfort.

CASHe loan app

CASHe is mainly known for salaried personal loans and short-tenure credit.

CASHe lists loan amount from ₹15,000 to ₹3 lakh on its website. Its terms page shows different monthly rates based on tenure, such as 1.667% flat per month for 90 days and up to 3% flat per month for 540 days. It also lists 2.5% processing fee across product slabs.

Good for: salaried users who need a short-term loan.

Check before applying: monthly rate, APR, processing fee, and delayed payment cost.

PaySense personal loan app

PaySense can suit users looking for EMI-based personal loans.

PaySense states personal loans up to ₹5 lakh. Its FAQ states interest of 1.4% to 2.3% per month.

Good for: users who need a smaller EMI loan.

Check before applying: final lender, APR, processing fee, and repayment schedule.

Finnable loan app

Finnable focuses on salaried professionals.

Its website says it gives personal loans for salaried professionals, mentions loan in 60 minutes, and says EMIs can be as low as ₹3,000 for loans up to ₹10 lakh.

Good for: salaried users who want a digital loan and salary-based eligibility.

Check before applying: current interest rate, lender details, APR, processing fee, and city availability.

Eligibility for salaried loan apps

Most loan apps check these details:

- age

- monthly salary

- job type

- salary account history

- CIBIL score

- employer profile

- existing EMI burden

- city

- PAN and Aadhaar

- bank statement

A higher salary does not guarantee approval. Existing EMIs, credit card dues, late payments, and low CIBIL can reduce approval chances.

For many salaried users, a credit score above 700 gives better chances. A score above 750 can improve the chance of a lower rate, depending on lender policy.

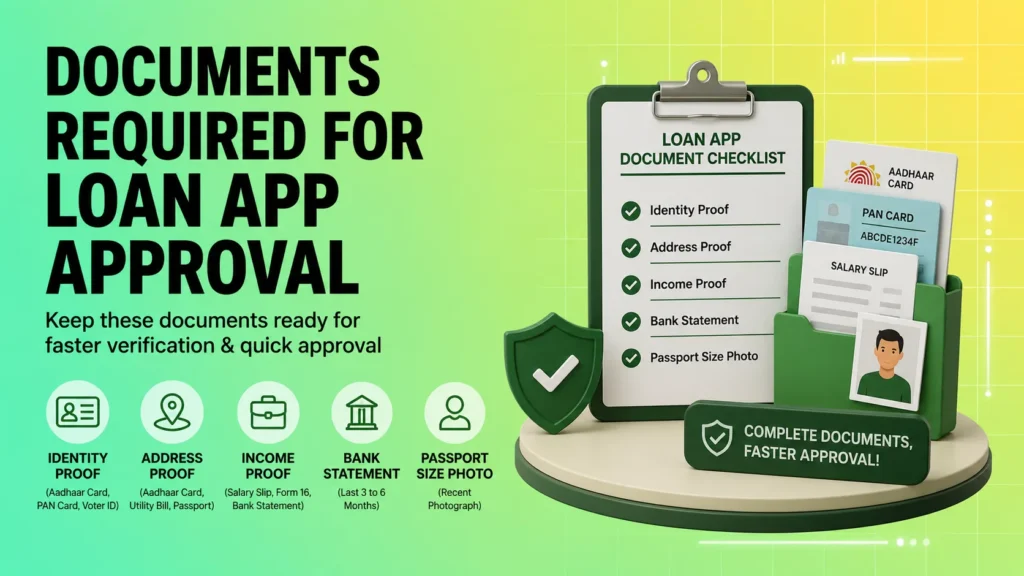

Documents required for loan app approval

Most loan apps ask for:

- PAN card

- Aadhaar card

- selfie or video KYC

- salary slip

- bank statement

- employment details

- current address proof

- salary account details

Some apps approve loans without a salary slip if the salary is visible in the bank statement. Moneyview, for example, says income must be credited directly to the bank account.

How to apply for a loan through an app

Step 1: Download the app from a safe source

Use Google Play Store, Apple App Store, or the lender’s official website.

Step 2: Enter basic details

Add name, mobile number, PAN, salary, city, and loan amount.

Step 3: Complete KYC

Most apps use PAN, Aadhaar, selfie, and bank verification.

Step 4: Upload income proof

Upload salary slip or bank statement if required.

Step 5: Check the offer

Before accepting, check:

- lender name

- loan amount

- APR

- EMI

- tenure

- processing fee

- GST

- late fee

- foreclosure rule

Step 6: Accept only after reading the KFS

The Key Fact Statement should show the cost clearly.

Step 7: Receive money in bank account

The money should come to your bank account after approval.

Best loan app for low interest

For low interest, bank apps and salary account offers are usually worth checking first.

Check your salary bank app, such as SBI YONO, HDFC Bank app, ICICI Bank app, Axis Bank app, Kotak app, or IDFC FIRST Bank app. Existing bank customers may get pre-approved personal loans because the bank already has salary and transaction data.

Among fintech loan apps, compare Moneyview, Fibe, Navi, KreditBee, PaySense, CASHe, and Finnable. The final rate depends on salary, CIBIL score, employer type, existing loans, city, and repayment history.

Best loan app for fast approval

For fast approval, apps like KreditBee, Moneyview, Fibe, and Finnable are worth comparing.

KreditBee mentions 10-minute disbursal and Moneyview mentions eligibility check in 2 minutes, subject to approval. Finnable mentions loan in 60 minutes.

Fast approval does not mean cheap loan. Always check APR and fees before accepting.

Best loan app for small emergency loan

For small emergency needs, compare KreditBee, Moneyview, PaySense, CASHe, and Fibe.

Small loans can become costly when processing fee, GST, and late charges are added. For example, a ₹10,000 loan with a flat fee can cost more than expected if the tenure is short.

Use small loans only when repayment is clear from your next salary cycle.

Best loan app for higher loan amount

For higher amounts, compare bank apps, Navi, Moneyview, Fibe, KreditBee, and Finnable.

Navi lists loan amount up to ₹20 lakh. Moneyview, Fibe, KreditBee, and Finnable list loan amounts up to ₹10 lakh.

For larger loans, check EMI carefully. A long tenure reduces monthly EMI, but total interest can increase.

RBI safety checklist before using any loan app

Use this checklist before applying.

1. Check bank or NBFC name

The app should show the regulated lender.

2. Check KFS

The KFS should show APR, repayment schedule, fees, recovery details, and grievance officer details.

3. Check data permissions

Avoid apps asking for contacts, gallery, call logs, or file access without a clear reason.

4. Check repayment account

Repayment should go through official payment channels linked to the lender.

5. Check complaint details

A genuine app should show customer care, grievance officer, and escalation process.

India has taken stricter action on illegal lending. Reuters reported that the Indian government proposed prison terms and fines for unauthorised lending, including digital platform loans, after complaints about unfair lending and predatory recovery practices.

Red flags of unsafe loan apps

Avoid a loan app if you see these signs:

- lender name is missing

- app asks for contact list access

- app asks for gallery access

- no KFS

- no loan agreement

- no complaint email or phone number

- very short 7-day or 15-day repayment pressure

- advance fee before loan approval

- WhatsApp-only support

- threats before or after repayment

- fake legal notice messages

- pressure to apply immediately

A real loan should give you time to read the cost.

Loan app vs bank personal loan

| Factor | Loan app | Bank personal loan |

|---|---|---|

| Approval speed | Usually faster | Can be fast for pre-approved users |

| Documentation | Mostly digital | Digital or branch-based |

| Interest rate | Can be higher | Often lower for strong salaried profiles |

| Loan amount | Small to medium | Medium to high |

| Best for | Emergency and quick credit | Bigger planned expenses |

| Safety check | Must verify lender | Usually clearer if taken from bank app |

For a salaried person, the safest first step is checking the salary bank app. Then compare NBFC-backed loan apps.

How salaried users can get lower interest

Keep CIBIL score healthy

Pay credit card bills and EMIs on time.

Avoid too many applications

Multiple applications can create hard enquiries.

Borrow only what you need

A smaller loan can improve approval chances and reduce EMI pressure.

Choose EMI based on salary

Keep EMI within a comfortable range. Rent, bills, school fees, insurance, and existing EMIs should be counted first.

Use salary account offers

Pre-approved bank offers can be cheaper for some users.

Compare APR

APR gives a clearer loan cost than a monthly interest number.

Common mistakes salaried users make

Applying without checking total cost

Interest rate is one part. Processing fee, GST, late fee, and bounce charge also matter.

Taking a short loan repeatedly

Repeated short loans can hurt monthly cash flow.

Ignoring salary date

Choose EMI date after salary credit.

Using risky apps for quick money

Unsafe apps can misuse phone data and pressure users through contacts.

Missing EMI

Late EMI can damage credit score and increase the next loan cost.

What to do if a loan app harasses you

First, contact the lender’s customer support and grievance officer.

Keep proof:

- screenshots

- call records

- WhatsApp messages

- payment receipts

- loan agreement

- KFS

- email communication

If recovery agents threaten you, misuse contacts, or send abusive messages, report the issue to the National Cyber Crime portal or call 1930. For lender-related complaints, use RBI complaint channels if the lender is regulated.

Final recommendation

For salaried users, start with your salary bank app. Then compare Moneyview, Fibe, KreditBee, Navi, CASHe, PaySense, and Finnable.

Pick the app only after checking lender name, APR, EMI, processing fee, late fee, foreclosure rules, and KFS.

Fast approval is useful. Low interest is better. Safe borrowing matters most.