What is PF in Salary?

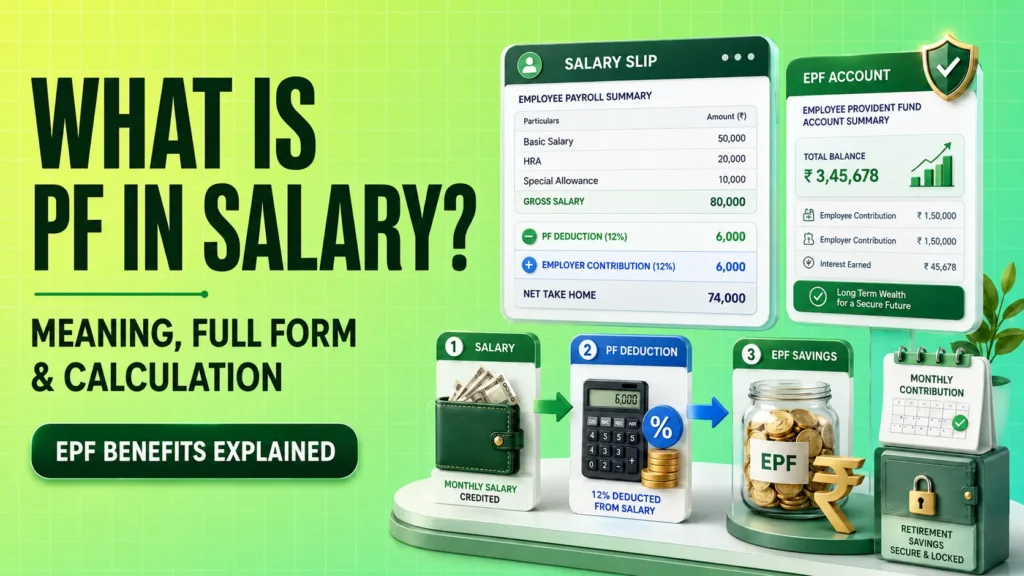

PF in salary means the amount deducted from an employee’s salary and contributed to the Provident Fund account. This fund is mainly created to help employees save money for retirement.

PF is not just a normal salary deduction. It is a long-term saving system where both employee and employer contribute a fixed percentage. The amount gets accumulated in the employee’s PF account and earns interest as per the rate declared by EPFO.

For example, if your salary slip shows “Employee PF” or “EPF Deduction,” it means that amount has been deducted from your salary and added to your PF account.

PF Full Form in Salary

PF full form in salary is Provident Fund.

In India, salaried employees usually come under EPF, which stands for Employee Provident Fund. EPF is managed by the Employees’ Provident Fund Organisation, also known as EPFO.

So, when someone asks what is PF in salary, the simple answer is:

PF is a retirement savings fund where a fixed part of your salary and your employer’s contribution are deposited every month.

Why is PF Deducted from Salary?

PF is deducted from salary to create a long-term savings fund for employees. Many people find it difficult to save money regularly. PF solves this problem by automatically deducting a fixed amount from salary every month.

This deduction helps employees build a retirement corpus without manually investing every month. Since the employer also contributes, PF becomes an important part of employee benefits.

PF can also help during certain financial needs. Under specific rules, employees may be allowed to withdraw PF partially for reasons such as medical emergencies, education, marriage, home purchase, or unemployment.

How Does PF Work in Salary?

PF works through monthly contributions. Every month, a part of the employee’s salary is deducted as employee contribution. The employer also contributes from its side.

Usually, PF is calculated on basic salary plus dearness allowance, not on the full CTC or gross salary. The standard contribution rate is generally 12% from the employee and 12% from the employer for establishments covered under EPF rules.

The employee’s contribution goes fully into the EPF account. The employer’s contribution is split between EPF and EPS, which is the Employee Pension Scheme.

Employee and Employer PF Contribution

Employee PF Contribution

The employee usually contributes 12% of basic salary plus dearness allowance to EPF. This amount is deducted from the employee’s salary every month.

For example, if your basic salary is ₹20,000, then employee PF contribution will be:

₹20,000 × 12% = ₹2,400

This ₹2,400 will be deducted from your salary and added to your EPF account.

Employer PF Contribution

The employer also contributes around 12% of basic salary plus dearness allowance. But the full employer contribution does not always go into the EPF account.

A part of the employer contribution goes to the Employee Pension Scheme, and the remaining part goes to EPF.

EPF and EPS Split

Generally, the employer contribution is split like this:

Here, ₹3,600 is the employee PF deduction.

Benefits of PF in Salary

PF has many benefits for salaried employees.

The biggest benefit is long-term retirement saving. Since PF is deducted every month, it helps employees create a disciplined savings habit.

Another benefit is employer contribution. Your employer also adds money to your retirement fund, which increases your total savings.

PF also earns interest. EPF interest rates are reviewed and declared from time to time, so employees should check the latest EPFO updates before making decisions.

PF can also provide financial support in certain situations. Employees may be able to withdraw partially for approved needs such as medical expenses, house purchase, marriage, education, or unemployment, depending on EPFO rules.

Tax Benefits of PF Contribution

PF can also help in tax planning. Employee contribution to EPF is generally eligible for deduction under Section 80C, subject to the overall limit and applicable tax regime rules.

However, tax rules may differ based on the old tax regime, new tax regime, contribution limits, withdrawal timing, and years of continuous service. So, before claiming tax benefits or withdrawing PF, it is better to check the latest tax rules or consult a tax expert.

EPF vs PPF: What is the Difference?

Many people confuse EPF and PPF. Both are savings schemes, but they are not the same.