Most people in India keep money in a savings account because it feels safe and easy to access. The problem is simple. Savings accounts give low interest, usually around 2.5% to 4%.

At the same time, fixed deposits (FDs) give higher returns, often 6% to 7.5% depending on the bank and tenure.

Auto Sweep FD sits between these two. It moves extra money from your savings account into fixed deposits automatically so that idle money keeps earning better interest without blocking access to funds.

Banks also call it flexi FD or sweep-in sweep-out facility.

This feature is common in salary accounts and premium savings accounts across banks like ICICI Bank, HDFC Bank, Axis Bank, SBI, and others.

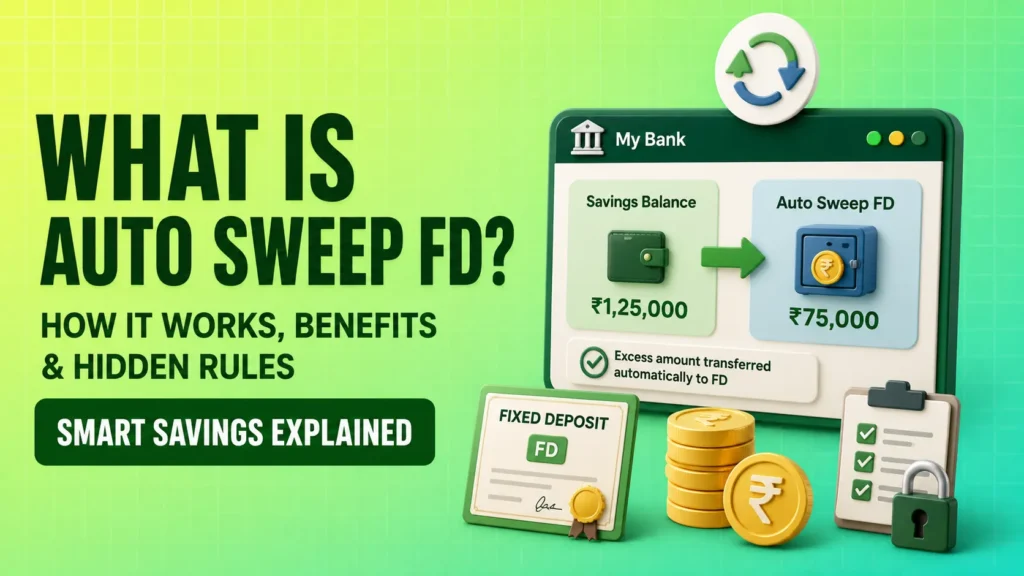

What is Auto Sweep FD?

Auto Sweep FD is a linked account facility where your savings account and fixed deposit account work together.

When your balance goes above a fixed limit (threshold), the extra money automatically gets converted into FD.

When your balance goes below that limit, the bank automatically breaks FD units and transfers money back into your savings account.

You do not need to manually open or close FD every time.

The system runs continuously in the background.

How Auto Sweep FD works (step-by-step)

The working model has three parts:

1. Setting a threshold limit

You decide a minimum balance to keep in your savings account.

Example:

Threshold limit = ₹25,000

- Savings balance = ₹80,000

- ₹55,000 is considered “extra”.

That extra amount moves into FD automatically.

2. Sweep-in process (money moves into FD)

When extra money is found, the bank creates one or more fixed deposits.

Important detail: banks do not create one large FD. They break the amount into smaller FD units.

Example:

- 55,000 may become:

- FD1 = ₹20,000

- FD2 = ₹20,000

- FD3 = ₹15,000

- Each FD can have its own interest calculation.

3. Sweep-out process (money comes back)

When your account balance falls below the threshold, the system breaks FD units and transfers money back.

Example:

- You spend ₹30,000

- Savings balance drops below ₹25,000

- Bank breaks FD units worth ₹30,000 and restores balance

This happens automatically.

No manual request needed.

Interest structure in Auto Sweep FD

Interest is not calculated like a single FD.

Each sweep-created FD has:

- its own start date

- its own interest rate

- its own maturity structure

Interest is usually higher than savings account interest but follows FD rules.

If FD is broken early due to sweep-out, interest is recalculated for the actual holding period.

Banks often apply premature withdrawal rules, which can reduce final returns slightly.

Types of Auto Sweep systems in India

Banks use different models. The structure is similar, but naming changes.

1. Sweep-in FD

Extra money from savings moves into FD automatically.

2. Sweep-out FD

Money comes back from FD when savings balance is low.

3. Flexi FD

A combined system of sweep-in and sweep-out.

4. Multi-deposit structure

Large balances are split into multiple small FDs for easy liquidity.

Benefits of Auto Sweep FD

1. Better interest on idle money

Money sitting unused in savings account starts earning FD-level interest.

This is the main advantage.

2. Liquidity remains intact

Even though money is in FD, you can still access it anytime.

The system breaks FD automatically when required.

No manual breaking needed.

3. Useful for salary accounts

Salary accounts often receive lump-sum deposits.

Auto sweep ensures extra salary money does not sit idle.

4. Emergency support without planning

If you suddenly need money, FD is automatically liquidated.

No delay, no application process.

5. Better cash management

People who maintain high balances benefit more because unused funds get automatically invested.

Hidden rules and limitations

Auto Sweep FD looks simple, but banks apply rules that many users do not notice.

1. Multiple FD fragmentation

Your money is split into many small FDs.

This creates complexity in:

- interest calculation

- withdrawal order

- maturity tracking

2. Premature withdrawal penalty

When FD is broken early due to sweep-out:

- interest rate may drop

- penalty may apply in some cases

You do not always get full FD returns.

3. Taxation on interest

Interest earned from sweep FD is fully taxable.

If multiple FDs generate interest, total income is added to your taxable income.

Banks may also deduct TDS if interest crosses limits.

4. Withdrawal order rules

Banks use internal rules like:

- FIFO (first in first out)

- LIFO (last in first out)

This decides which FD breaks first when cash is needed.

It can affect interest outcome.

5. Threshold setting matters

If you set threshold too low:

- money moves in and out frequently

- FD creation becomes fragmented

If you set it too high:

- liquidity reduces

- savings account may feel tight

6. Not ideal for low balance users

If your account rarely has extra funds, sweep FD gives little benefit.

Real-life example

Let’s take a simple case.

- Salary credited: ₹1,00,000

- Threshold: ₹30,000

- Extra amount: ₹70,000

Bank creates FD for ₹70,000.

After 10 days:

- You withdraw ₹50,000 for rent and expenses

- Bank breaks FD worth ₹50,000

- Remaining FD continues earning interest

This cycle repeats every month.

Who should use Auto Sweep FD?

It works best for:

- salaried employees with monthly credit

- people maintaining emergency funds

- users keeping ₹50,000+ idle balance

- conservative investors who avoid market risk

It is less useful for:

- low balance accounts

- people who frequently empty savings account

- short-term money movement users

Common mistakes users make

1. Treating it like a high-return investment

It is not an investment product. It is a banking feature for idle cash.

2. Ignoring fragmentation

Many users do not realize multiple FD units reduce clarity in interest tracking.

3. Setting wrong threshold

Wrong threshold leads to constant sweep activity and lower efficiency.

Conclusion

Auto Sweep FD is a hybrid banking feature that connects savings accounts with fixed deposits. It improves interest earnings while keeping money accessible.

The system works automatically through sweep-in and sweep-out rules, but banks apply fragmentation, premature withdrawal rules, and taxation that affect real returns.

It is useful for people who maintain consistent idle balances and want better returns without locking money manually.

FAQs

What is Auto Sweep FD in simple words?

It is a system that moves extra savings into fixed deposits automatically and brings it back when needed.

Is Auto Sweep FD safe?

Yes. It is a standard banking feature offered by major Indian banks.

Does Auto Sweep FD give higher returns?

Yes, because money earns FD interest instead of savings interest.

Can I withdraw money anytime?

Yes. The FD breaks automatically when your savings account needs funds.

Is interest taxable?

Yes. Interest from sweep FDs is taxable under income tax rules in India.