A systematic transfer plan is a mutual fund facility that allows you to transfer money automatically from one mutual fund scheme to another at fixed intervals. In simple words, instead of investing a large lump sum into equity funds in one go, you can first park the money in a liquid or debt fund and then transfer a fixed amount regularly into an equity fund.

This helps Indian investors reduce timing risk, manage volatility, and invest large amounts more gradually. But STP does not guarantee profit and it has tax, exit load, and market risks.

What is Systematic Transfer Plan?

A systematic transfer plan, also called STP, is a facility where money is moved from one mutual fund scheme to another scheme in a planned way.

Usually, investors use STP to transfer money from a lower-risk fund to a higher-risk fund.

For example:

- From liquid fund to equity fund

- From debt fund to hybrid fund

- From one equity fund to another fund

- From equity fund to debt fund for reducing risk

A common use case is this: you receive ₹3 lakh from bonus, FD maturity, property sale, or savings. You do not want to invest the full amount in equity mutual funds on the same day. So, you park it in a liquid fund and set up an STP of ₹25,000 per month into an equity fund for 12 months.

This gives you a disciplined way to enter the market gradually.

How Does a Systematic Transfer Plan Work?

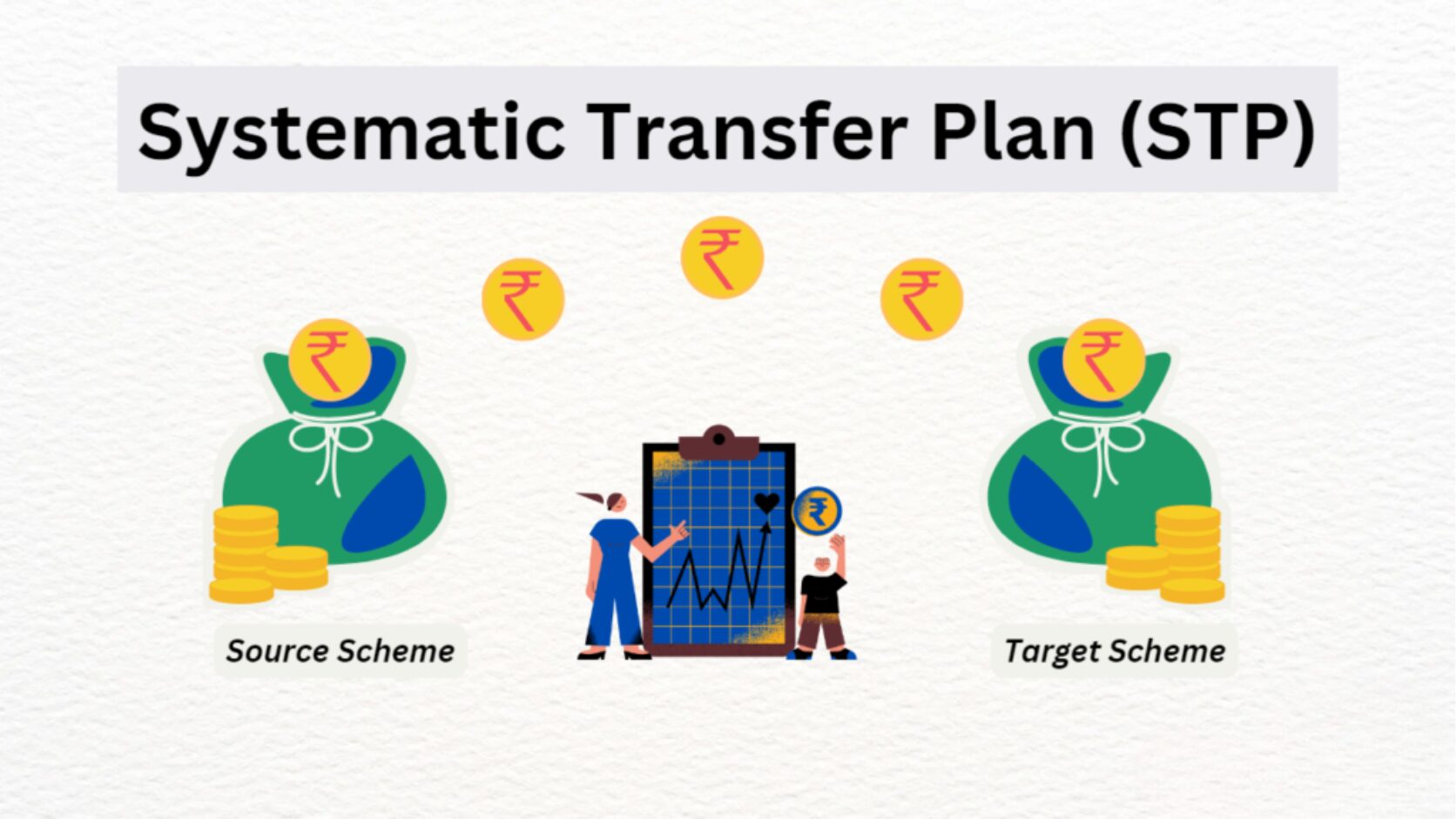

A systematic transfer plan has two main funds:

| Term | Meaning |

|---|---|

| Source fund | The fund from where money is transferred |

| Target fund | The fund where money is invested |

In most cases, the source fund is a liquid fund or debt fund, and the target fund is an equity fund.

Here is how it works:

- You invest a lump sum amount in the source fund.

- You choose the target fund.

- You select transfer amount, frequency, and duration.

- On each selected date, money is redeemed from the source fund.

- The redeemed amount is invested in the target fund.

- This continues until the STP duration ends or the source fund balance is exhausted.

The competitor article also explains STP as a method where money is transferred gradually from one investment to another over time, often from debt to equity, to manage volatility.

Systematic Transfer Plan Example

Suppose Priya has ₹1,20,000. She wants to invest in an equity mutual fund for a 7-year goal, but she is worried that the market may fall soon after investing.

Instead of investing ₹1,20,000 in equity on one day, she can use STP.

| Detail | Example |

|---|---|

| Lump sum amount | ₹1,20,000 |

| Source fund | Liquid fund |

| Target fund | Equity index fund |

| STP amount | ₹10,000 per month |

| STP duration | 12 months |

| Goal | Long-term wealth creation |

Every month, ₹10,000 will move from the liquid fund to the equity fund. If the market falls, she may get more equity fund units at lower NAV. If the market rises, she still participates gradually.

This does not guarantee higher returns, but it reduces the risk of investing the full amount at the wrong time.

Types of STP in Mutual Funds

Fixed STP

In fixed STP, a fixed amount is transferred at regular intervals.

Example: ₹10,000 every month from liquid fund to equity fund.

This is the most common and beginner-friendly STP type.

Capital Appreciation STP

In this type, only the profit or appreciation from the source fund is transferred to another fund.

Example: If your debt fund grows by ₹2,000, only that ₹2,000 is transferred to an equity fund.

This can be useful for conservative investors, but the transferred amount may be small.

Flexible STP

In flexible STP, the transfer amount may vary based on predefined conditions or investor instructions.

This is more suitable for experienced investors who understand market cycles and asset allocation.

STP vs SIP vs SWP

Many beginners confuse SIP, STP and SWP. They are different facilities.

| Feature | SIP | STP | SWP |

|---|---|---|---|

| Full form | Systematic Investment Plan | Systematic Transfer Plan | Systematic Withdrawal Plan |

| Main purpose | Invest regularly from bank account | Transfer from one fund to another | Withdraw regularly from a fund |

| Best for | Monthly salary investors | Lump sum investors | Retirement or monthly income needs |

| Money comes from | Bank account | Mutual fund scheme | Mutual fund scheme |

| Common use | Monthly SIP in equity fund | Liquid fund to equity fund | Monthly withdrawal from debt/hybrid fund |

Use SIP when you want to invest monthly from your salary.

Use STP when you already have a lump sum amount and want to invest gradually.

Use SWP when you want regular withdrawals from your mutual fund investment.

If you want to increase your SIP amount every year, you can also read our guide on step-up SIP strategy.

Benefits of Systematic Transfer Plan

Reduces Timing Risk

STP helps avoid investing the full amount into equity funds on a single day. This is useful when markets are volatile.

It does not remove risk, but it spreads the entry over time.

Helps Manage Market Volatility

When equity markets move up and down, STP can help average out the purchase cost over multiple dates.

This is similar to SIP-style discipline, but it is used for lump sum money.

Keeps Idle Money Invested

Instead of keeping lump sum money idle in a savings account, investors may park it in a liquid or debt fund until the transfer is completed.

However, debt and liquid funds also have risks, so investors should check scheme details carefully.

Useful for Goal-Based Planning

STP is useful when you know your goal and time horizon.

For example:

- Child education goal after 8 years

- Retirement planning

- Long-term wealth creation

- Gradual shift from debt to equity

- Reducing equity exposure before a near-term goal

Encourages Discipline

Once STP is set, transfers happen automatically. This reduces emotional decisions and panic-based investing.

Risks, Charges and Tax Impact of STP

STP is useful, but it is not risk-free.

Market Risk

The target fund may fall after money is transferred. If you are transferring into equity funds, your investment value can go down in the short term.

Mutual fund NAVs can go up or down due to market factors, and past performance does not guarantee future performance.

Source Fund Risk

Many investors assume liquid funds and debt funds are completely risk-free. That is not correct.

Debt funds may carry:

- Interest rate risk

- Credit risk

- Liquidity risk

- Reinvestment risk

Before choosing the source fund, check portfolio quality, maturity, expense ratio, and riskometer.

SEBI has issued circulars on product labelling and risk-o-meter disclosure for mutual fund schemes, so investors should check the scheme risk level before investing.

Exit Load

Some mutual fund schemes charge exit load if units are redeemed before a specific period.

Since every STP transfer involves moving money from one fund to another, exit load may apply depending on the source fund’s rules.

Always check the Scheme Information Document before setting up STP.

Tax Impact

Every STP transfer may be treated like a redemption from the source fund and a fresh investment in the target fund. This means capital gains tax may apply if there is a gain.

Tax depends on:

- Type of source fund

- Holding period

- Date of transfer

- Investor category

- Applicable tax rules

AMFI’s mutual fund tax page explains that tax treatment differs for equity-oriented funds and other funds, and rules changed for transfers on or after 23 July 2024 in some cases. For example, short-term capital gains on equity-oriented fund units transferred on or after 23 July 2024 are listed at 20%, and long-term gains above ₹1.25 lakh are listed at 12.5%, subject to conditions.

Tax rules can change. Always verify with the Income Tax Department, AMFI, fund house documents, or a qualified tax advisor before making large transfers.

If you are investing for tax-saving purposes, first understand how ELSS funds in mutual funds work.

When Should You Use STP?

A systematic transfer plan may be suitable when:

- You have a lump sum amount

- You want to invest in equity gradually

- You are worried about market volatility

- Your goal is long term

- You want disciplined transfer from debt to equity

- You received bonus, inheritance, FD maturity, or property sale money

- You do not want to time the market manually

STP is most useful when the target investment has market risk and you want gradual exposure.

When STP May Not Be Suitable

STP may not be suitable in every case.

Avoid or reconsider STP when:

- Your goal is very short term

- You need the money within a few months

- You do not understand the source and target fund

- Exit load is high

- Tax impact is not checked

- You are transferring to a high-risk fund without understanding volatility

- You are using STP only because someone said it is “safe”

STP reduces timing risk, but it does not make equity investing safe or guaranteed.

How Long Should You Run an STP?

There is no fixed perfect duration. It depends on your amount, goal, and risk appetite.

| Situation | Possible STP Duration |

|---|---|

| Small lump sum like ₹50,000 | 3 to 6 months |

| Medium amount like ₹2 lakh to ₹5 lakh | 6 to 12 months |

| Large corpus like ₹10 lakh or more | 12 to 24 months |

| Very volatile market | Longer phased transfer may help |

| Long-term goal above 7 years | Faster transfer may also be acceptable |

Do not stretch STP unnecessarily for many years if your goal is long term and you understand equity risk. Keeping too much money in low-return funds for too long may reduce growth potential.

How to Start a Systematic Transfer Plan

The process may vary by AMC, platform, or mutual fund app, but the general steps are:

- Choose the fund house.

- Invest lump sum in the source fund.

- Select the target fund.

- Choose transfer amount.

- Select frequency such as weekly, monthly, or quarterly.

- Select start date and end date.

- Check exit load, tax impact, and scheme riskometer.

- Confirm the STP request.

Most STPs are easier when source and target funds are from the same AMC.

Before choosing a fund, understand the difference between direct vs regular mutual funds because expense ratio can affect long-term returns.

Documents Required for STP

If your mutual fund account is already active and KYC is complete, you may not need many documents.

Common requirements include:

- PAN

- KYC completion

- Bank account details

- Folio number

- Source fund details

- Target fund details

- STP instruction form or online request

For online platforms, Aadhaar-based verification, OTP, or registered email/mobile confirmation may be required depending on the platform.

Common Mistakes to Avoid

Avoid these mistakes while using a systematic transfer plan:

- Choosing source fund only by return

- Ignoring exit load

- Ignoring tax impact

- Selecting too short a duration for a large amount

- Selecting too long a duration for a long-term goal

- Transferring into a risky fund without checking riskometer

- Assuming liquid funds are risk-free

- Starting STP without knowing your goal

- Not reviewing the portfolio after STP completion

A good STP plan should match your goal, not market gossip.

Myth vs Reality

| Myth | Reality |

|---|---|

| STP guarantees better returns | STP only spreads investment; returns are not guaranteed |

| STP is tax-free | Transfers may create capital gains tax |

| STP removes market risk | It reduces timing risk, not market risk |

| Liquid funds are completely safe | They are lower risk than equity but not risk-free |

| STP is always better than lump sum | It depends on market, goal, amount, and risk appetite |

Advanced STP Strategy for Large Corpus

If you have a large corpus, such as ₹10 lakh, ₹25 lakh, or more, do not start a random monthly STP without planning.

Use this framework:

| Step | Action |

|---|---|

| Step 1 | Decide goal and time horizon |

| Step 2 | Keep near-term money in safer options |

| Step 3 | Divide long-term money into equity allocation |

| Step 4 | Use STP for gradual entry |

| Step 5 | Review tax and exit load |

| Step 6 | Rebalance after STP completion |

Example:

If you have ₹12 lakh for a 10-year goal, you may transfer ₹1 lakh per month for 12 months into equity funds. But if you are very conservative, you may use ₹50,000 per month for 24 months.

If the market has already corrected sharply, a shorter STP may be reasonable. If the market is highly expensive or volatile, a longer STP may feel more comfortable.

This is why STP is not a fixed formula. It is a planning tool.

Final Conclusion

A systematic transfer plan is a useful mutual fund facility for investors who have a lump sum amount but do not want to invest the full money in equity funds at once. It helps reduce timing risk, manage volatility, and build investment discipline.

But STP is not risk-free. Every investor should check market risk, source fund risk, exit load, tax impact, and investment horizon before starting.

For Indian beginners, STP can be a smart method when used with proper goal planning. But it should not be treated as a guaranteed-return strategy.

Disclaimer: This article is for educational purposes only. Mutual fund investments are subject to market risks. Read all scheme-related documents carefully and verify latest tax rules, charges, and scheme details from official sources before investing.