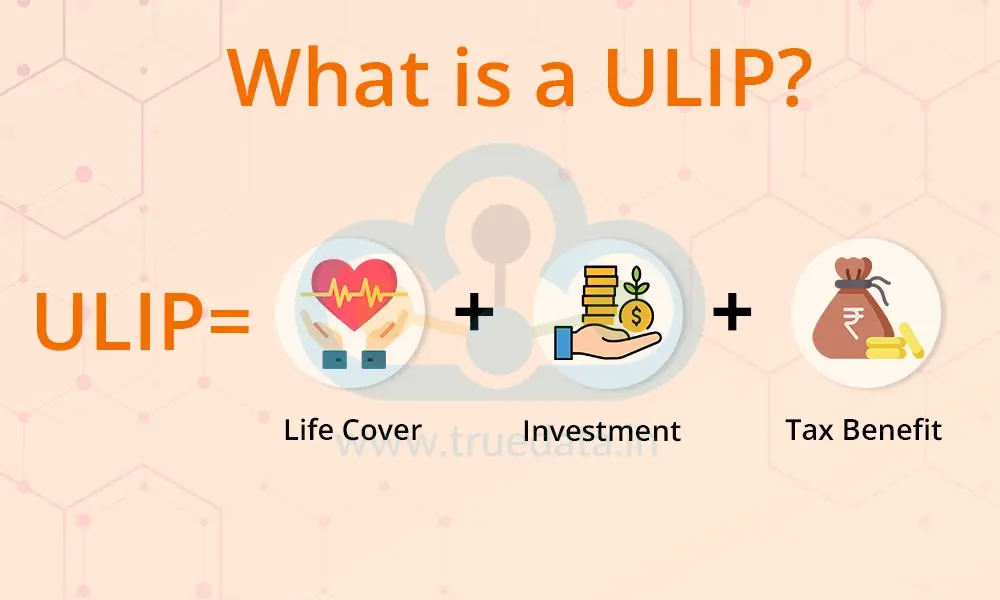

A ULIP offers life insurance and market-linked investment within one policy. This combination may look convenient, but it can also make the product harder to understand.

While ULIPs offer fund choices, tax benefits and long-term investment discipline, they also come with market risk, multiple charges and a five-year lock-in period. Before investing, you should understand the main ULIP advantages and disadvantages and compare them with separate insurance and investment options.

What Is a ULIP and How Does It Work?

ULIP stands for Unit Linked Insurance Plan. It combines life insurance cover with market-linked investment.

When you pay a premium, the insurer deducts applicable charges. One part of the premium provides life insurance, while the remaining amount is invested in funds selected by you.

The process works like this:

Premium paid → Charges deducted → Life cover provided → Remaining amount invested → Units allocated

You can usually choose from:

- Equity funds: Invest mainly in shares and carry higher market risk.

- Debt funds: Invest mainly in bonds and fixed-income securities.

- Balanced funds: Invest in both equity and debt.

The fund value changes according to the performance of the selected investments. Therefore, ULIP returns are not guaranteed.

Advantages of ULIPs

Life Insurance and Investment in One Plan

A ULIP provides life insurance protection and an investment component under one policy. This may be convenient for people who prefer managing both through a single product.

However, you should still check whether the life cover is enough to support your family.

Choice of Investment Funds

You can select equity, debt or balanced funds based on your financial goals and risk tolerance.

Equity funds may suit investors seeking long-term growth, while debt funds may be suitable for those who prefer comparatively lower market risk.

Fund-Switching Facility

Most ULIPs allow policyholders to move money between available funds.

For example, you may shift from an equity fund to a debt fund when you want to reduce investment risk. The number of free switches and charges for additional switches depend on the policy.

Long-Term Investment Discipline

The mandatory ULIP lock-in period is five years. This prevents frequent withdrawals and encourages policyholders to remain invested for long-term goals.

However, five years should not be considered the ideal investment period. Market-linked products may require a longer horizon to manage short-term market fluctuations.

Partial Withdrawals

Partial withdrawals are generally available after completing the lock-in period, subject to policy conditions.

This facility may help with financial needs such as education, medical expenses or another planned goal without closing the entire policy.

Transparency

Policyholders can usually track:

- Number of units

- Net Asset Value

- Fund value

- Premium allocation

- Policy charges

- Fund performance

The insurer must also provide a benefit illustration showing how the policy may perform under assumed return scenarios. These illustrations are examples and not guaranteed returns.

Possible Tax Benefits

ULIP premiums and policy proceeds may receive tax benefits when the policy meets applicable tax-law conditions.

Tax treatment depends on factors such as the policy issue date, annual premium, sum assured and prevailing tax rules. You should not assume that every ULIP maturity amount will automatically be tax-free.

Disadvantages of ULIPs

Multiple Charges

One of the main disadvantages of ULIPs is their charge structure.

A policy may include:

| ULIP charge | Purpose |

|---|---|

| Premium allocation charge | Deducted before the premium is invested |

| Mortality charge | Cost of providing life cover |

| Fund management charge | Cost of managing the investment fund |

| Policy administration charge | Cost of maintaining the policy |

| Switching charge | May apply after free switches are used |

| Discontinuance charge | May apply when premiums are stopped early |

These deductions reduce the amount invested and can affect the final return. Check the policy-year-wise charge table before buying.

Five-Year Lock-In Period

You cannot freely withdraw your investment during the first five policy years.

If you stop paying premiums during this period, the policy may be moved to a discontinued policy fund. The amount is normally released only after the lock-in period ends, according to policy rules.

This makes ULIPs unsuitable for people who may need access to their money in the short term.

Returns Are Not Guaranteed

ULIP returns depend on the performance of the selected market-linked funds.

Equity funds can fall during weak market conditions, while debt funds may also face interest-rate and credit risks. The final fund value may be lower than the amount shown in promotional illustrations.

ULIPs Can Be Difficult to Understand

A ULIP includes insurance cover, investment funds, units, NAV, charges, switching rules and withdrawal conditions.

This structure can make the product more complicated than a pure term insurance plan or a direct investment product. Buyers who do not understand these features may select unsuitable funds or underestimate the effect of charges.

Life Cover May Be Lower Than Term Insurance

For the same premium, a pure term insurance policy may provide substantially higher life cover because it does not include an investment component.

A ULIP may therefore be unsuitable when your primary goal is to obtain a large sum assured at an affordable premium.

Early Discontinuance Can Affect the Value

Stopping premiums during the early years may lead to discontinuance charges and loss of active life cover.

Even after completing the lock-in period, closing the policy early may prevent the investment from getting enough time to recover charges and benefit from long-term market growth.

Tax Benefits Are Conditional

ULIP tax benefits depend on applicable legal conditions. High-premium policies may not receive the same maturity exemption as eligible lower-premium policies.

Tax rules can also change. Do not buy a ULIP only for tax saving without checking its coverage, charges and investment suitability.

ULIP vs Term Insurance Plus Mutual Fund

A common alternative is to buy term insurance for life protection and invest separately through mutual funds.

| Factor | ULIP | Term Plan and Mutual Fund |

|---|---|---|

| Structure | Insurance and investment combined | Insurance and investment separate |

| Life cover | Depends on policy terms | Usually higher through term insurance |

| Fund choice | Limited to insurer’s funds | Wider mutual-fund selection |

| Lock-in | Five years | Depends on selected mutual fund |

| Charges | Insurance and investment charges | Term premium and fund expense ratio |

| Liquidity | Restricted during lock-in | Depends on the investment |

| Management | One combined product | Both parts managed separately |

Neither option is suitable for everyone.

A ULIP may appeal to someone who wants insurance and investment in one plan. A term plan with mutual funds may suit someone who wants higher life cover and greater control over investments.

Who Should Consider a ULIP?

A ULIP may be suitable if you:

- Want insurance and investment in one policy

- Have a long investment horizon

- Can remain invested beyond five years

- Understand market risk

- Want to switch between funds

- Have reviewed all policy charges

- Already know how much life cover your family needs

The benefits of ULIP investment are more useful when the policy is held for a long period and the selected funds match your risk profile.

Who Should Avoid a ULIP?

A ULIP may not be suitable if you:

- Need high life cover at a low premium

- Want guaranteed returns

- Require short-term access to your money

- May stop paying premiums during the early years

- Do not understand market-linked investments

- Prefer to manage insurance and investments separately

- Have not compared all charges

Do not invest only because an agent highlights projected returns or tax benefits.

What Should You Check Before Buying a ULIP?

Before purchasing a ULIP, compare:

- Sum assured

- Policy term

- Premium-payment term

- Available fund options

- All policy charges

- Fund performance against a suitable benchmark

- Free fund-switching limit

- Partial withdrawal rules

- Discontinuance conditions

- Death and maturity benefits

- Tax conditions

Also review the benefit illustration at assumed returns of 4% and 8%. These figures help explain the effect of charges but do not guarantee that you will earn those returns.

Is a ULIP a Good Investment?

A ULIP may be a suitable long-term option for someone who wants life insurance and market-linked investment within one policy. It also provides fund choices, switching options and disciplined investing.

However, it may not be the best choice if your main requirement is high life cover, simple investment management, guaranteed returns or short-term liquidity.

Before investing, compare the ULIP with a separate term plan and suitable investment products. The right decision depends on your protection needs, financial goals, risk tolerance and ability to remain invested.

Conclusion

The main ULIP pros and cons come from its combined structure. It offers life cover, market-linked growth, fund switching and possible tax benefits, but also has multiple charges, market risk and limited liquidity.

A ULIP can work for a disciplined long-term investor who understands the product. It may not suit someone who needs high insurance coverage at a low cost or wants complete control over investments.

Read the policy document, charge table and benefit illustration carefully before making a decision.