When you buy health insurance, one question matters more than the premium: will the insurer actually pay when you need it most? That is where the health insurance claim settlement ratio comes in. It is one of the most searched numbers in India because it looks like a quick way to judge an insurer’s reliability.

But here is the reality check: a high claim settlement ratio is useful, not conclusive. It tells you something about past claims, not a promise about your future claim. To make a smarter choice, you need to understand what the ratio means, where it can mislead you, and what other metrics and policy details matter just as much.

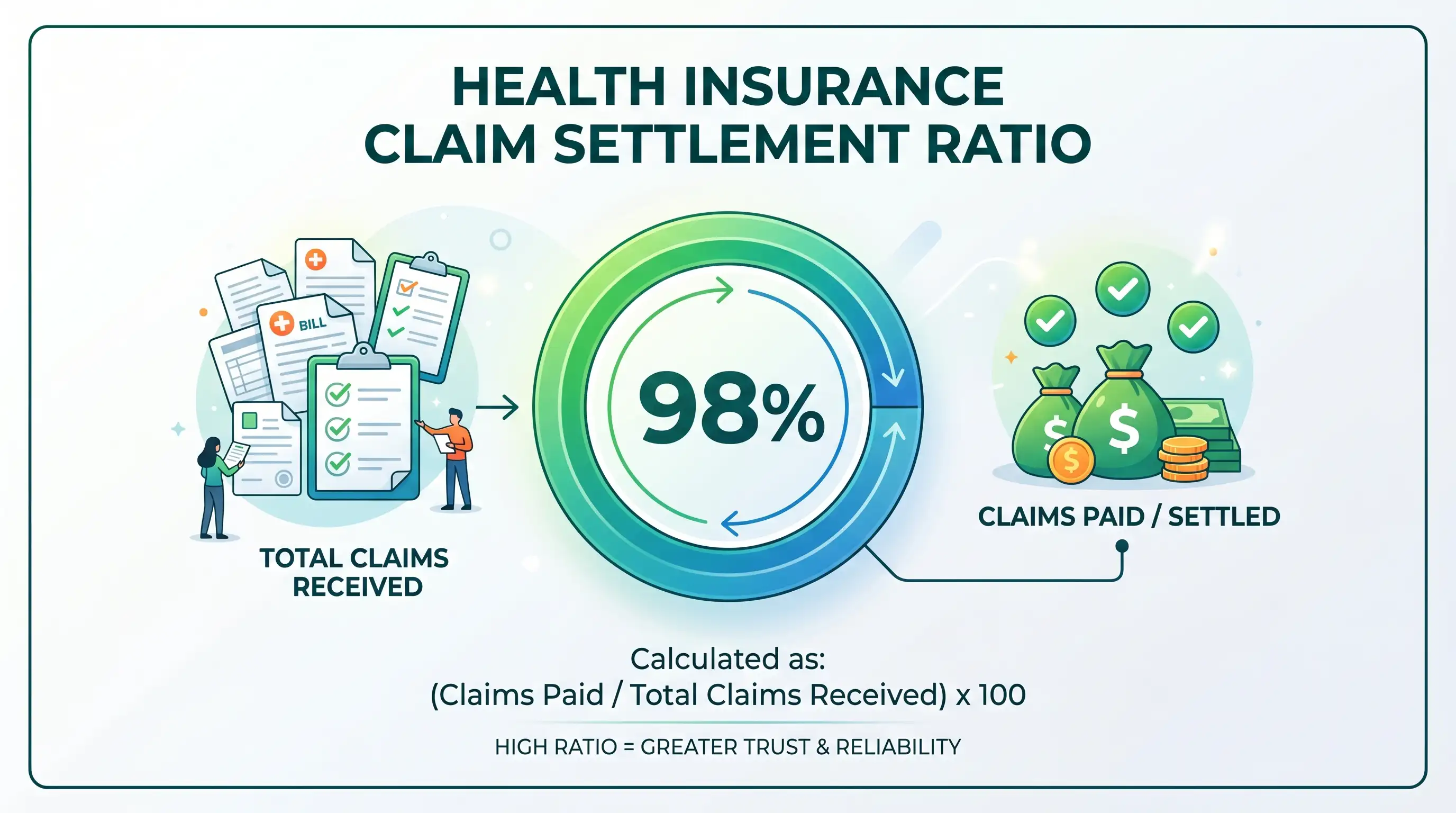

What is the Health Insurance Claim Settlement Ratio?

The health insurance claim settlement ratio, often called CSR, shows the percentage of claims an insurer settled out of the total claims it received during a specific period. The basic formula is:

The health insurance claim settlement ratio, often called CSR, shows the percentage of claims an insurer settled out of the total claims it received during a specific period. The basic formula is:

CSR = (Claims Settled ÷ Total Claims Received) × 100

For example, if an insurer received 100 health insurance claims in a year and settled 95 of them, the CSR would be 95%. In simple terms, that means 95 claims were paid or accepted according to the policy terms, while 5 were not settled.

In India, this data is usually reported in official insurer disclosures and IRDAI annual reports or handbooks. That is important because you should rely on official sources, not social media claims or marketing material, when comparing insurers.

It is also important to understand what “settled” means here. A claim may be settled in full or in part, depending on the policy terms, room rent limits, co-payment, deductibles, exclusions, and documents submitted. Insurance is a contract, so the final outcome always depends on the policy wording and not only on the ratio.

| Metric | What it tells you | Caution |

|---|---|---|

| Claim Settlement Ratio | How many claims were settled out of total claims received | A past-data indicator, not a guarantee for your future claim |

| Incurred Claim Ratio | How much the insurer paid in claims compared to premium collected | Can be affected by pricing, expenses, and product mix; not a direct measure of your claim experience |

| Claim Rejection Ratio | How many claims were rejected or repudiated | Very useful to understand denial patterns, but reasons matter more than the raw number |

This comparison matters because many buyers treat CSR as the only trust score. It is not. The number is helpful, but it does not tell you whether the claim was simple, whether the policyholder submitted proper documents, or whether the claim fell under an exclusion.

Why You Should Not Rely Solely on High CSR

A high health insurance claim settlement ratio can look reassuring, but it can also be misunderstood. One reason is selection bias: the ratio reflects the claims that came in during a given period and how the insurer handled them. It does not tell you the whole story behind those claims.

For example, an insurer may have a high CSR because many claims were small, simple, and fully documented. Another insurer may have a slightly lower CSR because it handled more complex cases, more high-value hospitalisations, or a larger share of disputed claims. A single percentage cannot capture that full picture.

There is also the issue of rejected claims. An insurer may reject claims for valid reasons such as policy exclusions, non-disclosure of pre-existing diseases, waiting periods, fraud, or missing documents. That does not automatically mean the insurer is unfair. At the same time, a ratio alone does not show whether the insurer communicated claim requirements clearly or helped customers file claims properly.

That is why high CSR should never be read as “your claim will definitely be paid.” It only means that, historically, the insurer settled a certain share of claims received in that period. Your own claim will still depend on the policy terms, hospital bills, diagnosis, waiting period, and documentation.

Another trap is that ratios can be affected by the volume of claims. A company with fewer claims may show a strong ratio in a period, but that does not always make it the smoothest choice for every policyholder. The bigger question is whether the insurer’s process is transparent and whether the policy fits your needs.

Understanding the Claim Rejection Ratio

The flip side of CSR is the claim rejection ratio. This shows how many claims were repudiated or denied. If CSR helps you see the positive side, the rejection ratio helps you understand the risk side.

For a buyer, the real value lies in the reasons behind rejections. Common reasons include:

- Policy exclusions not covered under the plan

- Waiting period not completed for a specific illness

- Incorrect or incomplete documents

- Non-disclosure of medical history or lifestyle risks

- Treatment taken at a non-network hospital for cashless claims

- Claim filed beyond the timeline required in the policy

This is why reading the policy wording is so important. The fine print tells you what is covered, what is not, and what documents the insurer may ask for. In health insurance, the contract terms often matter more than any headline ratio.

Beyond the Ratio: 3 Better Metrics to Evaluate Health Insurance

If you want to judge an insurer more practically, look at the ratio plus these three factors. They often tell you more about your actual claim experience than CSR alone.

1. Claim Processing Time

How fast does the insurer process claims? A company can have a good CSR and still take a long time to approve or settle a claim. For hospitalisation, speed matters because cashless approval and claim settlement can reduce stress during a medical emergency.

Ask these questions before buying:

- How long do cashless approvals usually take?

- How long does reimbursement settlement take?

- Are delays common for document verification?

2. Network Hospital Coverage

Check whether your preferred hospitals are in the insurer’s cashless network. This is especially important in metro cities and for families with a regular doctor or hospital preference. A large network is helpful, but the quality and convenience of network hospitals matter more than just the count.

If your preferred hospital is outside the network, you may need to pay first and file a reimbursement claim later. That is not always a problem, but it changes the process and may require more paperwork.

3. Claim Settlement Process: In-house or Through a TPA

Find out whether the insurer handles claims in-house or through a Third Party Administrator (TPA). An in-house claim settlement team can sometimes make communication more direct because the insurer and claims desk are under one roof. That does not automatically make it better, but it is easier to follow up when one team owns the process.

With a TPA, the claim may still be perfectly smooth if the process is well managed. The key point is not the label alone, but how clear, responsive, and documented the process is. Ask who handles pre-authorisation, which documents are needed, and where grievances should be escalated if the claim gets delayed.

How to Actually Check if an Insurer is Reliable

If you are buying health insurance for the first time, use a simple verification process instead of relying only on marketing claims or a single ratio.

Step 1: Visit the official IRDAI website for annual reports

Start with official data. IRDAI annual reports and handbooks are the most reliable sources for claim-related information in India. These reports help you compare insurers using standardised data instead of promotional language. When you compare companies, use the latest available official report and check the period covered.

Step 2: Check the insurer’s claim settlement process

Look at whether claims are handled in-house or through a TPA. Then read how cashless and reimbursement claims work. A good insurer should explain the steps clearly, including timelines, documents, and contact points for support.

If the process feels confusing before purchase, it may become even more confusing during a medical emergency.

Step 3: Look at the Free Look Period and policy transparency

The free look period gives you a window to review the policy after purchase and cancel it if you are not satisfied, subject to the insurer’s rules. This is your chance to verify whether the policy wording matches what was promised to you. Use this time carefully.

Also check whether the insurer clearly explains sub-limits, co-payment, room rent limits, waiting periods, and exclusions. A transparent policy document is usually a better sign than a flashy brochure.

Step 4: Check customer grievances and complaint trends

Customer grievance data can reveal whether policyholders face repeated delays, poor communication, or unfair claim handling. If available in official disclosures, compare the complaint trends along with CSR. A company with a strong CSR but many unresolved complaints may not be the best choice for a nervous buyer.

Also check how quickly the insurer responds to complaints and whether the escalation path is clear. A responsive support system can matter a lot during hospitalisation.

Helpful Interactive Tool: Key Metrics Comparison

| Metric | What it tells you | Limit/Caveat |

|---|---|---|

| Health Insurance Claim Settlement Ratio | How many claims were settled out of total claims received in a period | Lagging indicator based on past data; does not guarantee future approval |

| Incurred Claim Ratio | How much premium collected was paid out as claims | Can vary with pricing, product design, and business mix; not enough on its own |

| Claim Rejection Rate | How often claims were rejected or repudiated | Rejection reasons matter more than the raw rate; some rejections are valid |

Safety note: These metrics are indicators, not guarantees of claim approval. Your individual claim experience will depend on the policy wording, exclusions, waiting periods, documents, and insurer rules.

Common Mistakes When Buying Health Insurance

Many claim problems begin at the time of purchase, not at the time of hospitalisation. Avoid these common mistakes if you want fewer surprises later.

Many claim problems begin at the time of purchase, not at the time of hospitalisation. Avoid these common mistakes if you want fewer surprises later.

- Focusing only on the premium. A cheaper plan may have stricter exclusions, lower room rent limits, co-payment clauses, or higher out-of-pocket costs later.

- Ignoring sub-limits and co-payment clauses. These can reduce the amount the insurer pays, even when the claim is otherwise valid.

- Failing to disclose pre-existing diseases. This is one of the biggest reasons for claim rejection and can lead to serious disputes later.

- Not reading the waiting period rules. Some conditions are covered only after a certain time has passed.

- Assuming every hospital bill is reimbursable. The policy may not cover certain consumables, non-medical expenses, or treatments outside approved terms.

- Not keeping documents ready. Discharge summaries, prescriptions, investigation reports, KYC, and bills should be preserved carefully.

The simplest way to reduce claim trouble is to declare your health history honestly, read the policy wording line by line, and ask the insurer or advisor to explain unclear terms before you buy. Insurance is a contract, and the contract language decides the outcome more than the advertisement does.

Author note: This article is for educational purposes only and should not be treated as a recommendation to buy from any specific insurer. Insurance products are subject to policy terms, exclusions, waiting periods, underwriting rules, and regulatory changes. Please verify the latest details from the insurer and official IRDAI sources before making a decision.

Frequently Asked Questions

Is a 95%+ CSR considered good?

Yes, a 95%+ CSR is generally considered strong, but it should be read with context. A high ratio is more useful when the insurer has handled a large number of claims and still maintained a good settlement record. Always check the claim volume, complaint trends, and policy terms too.

Does a high CSR guarantee my claim will be settled?

No. A high CSR does not guarantee approval of your claim. Your claim will still depend on policy exclusions, waiting periods, document submission, medical necessity, and whether the treatment falls within the policy wording.

Where can I find official CSR data for Indian insurers?

The most reliable source is the IRDAI Annual Report or official IRDAI insurance handbook. You should use these official documents for comparison instead of relying on promotional claims or unverified online lists.

Why do some insurers have a low CSR?

A lower CSR can happen for valid reasons such as incomplete documentation, policy exclusions, waiting periods, non-disclosure of medical history, or fraudulent claims. It may also reflect a stricter claims process, so the reasons behind the number matter more than the number itself.

What is an in-house claim settlement team?

An in-house claim settlement team means the insurer handles claims directly through its own team instead of outsourcing the process fully to a TPA. This can make coordination easier in some cases, but the real test is whether the process is clear, responsive, and well documented.