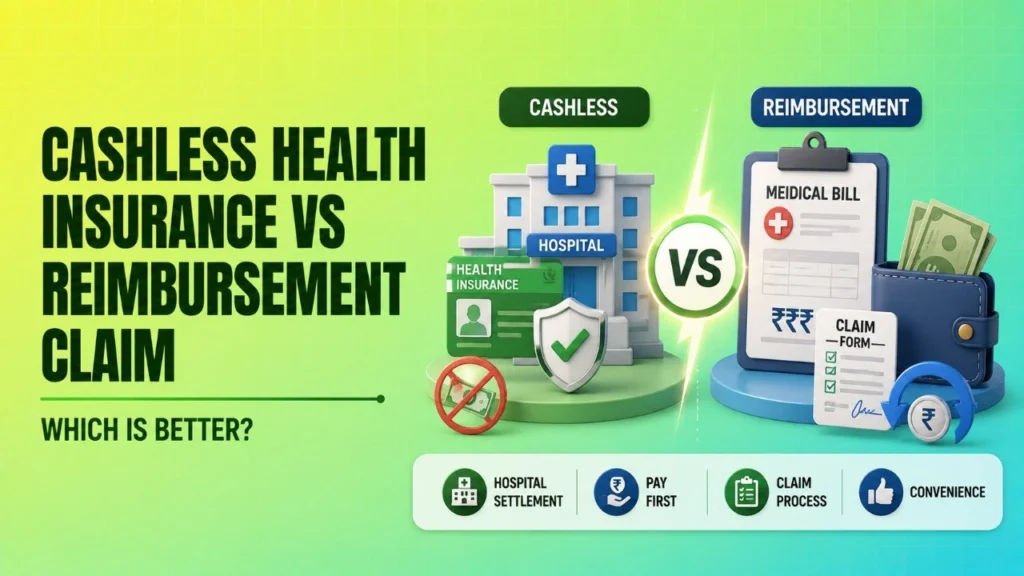

When a medical emergency happens, the last thing most families want to think about is bill settlement. But the way your health insurance pays the hospital can make a big difference to your cash flow, stress level, and claim experience. That is why understanding cashless vs reimbursement health insurance matters before you ever need to use it.

In simple terms, a cashless claim means the insurer or its TPA settles the eligible hospital bill directly with the hospital. A reimbursement claim means you pay the bill first and later ask the insurer to repay the covered amount. Both are valid claim methods in Indian health insurance, but the better option often depends on whether the hospital is a network hospital, how urgent the treatment is, and whether you can arrange money upfront.

Understanding Cashless vs. Reimbursement Claims

The main difference is the flow of money. In a cashless arrangement, the hospital sends the claim to the insurer or TPA, and the insurer settles the approved amount directly with the hospital. In a reimbursement claim, you act as the middle step: you pay the hospital bill, collect the papers, and file the claim later.

Both methods are commonly available in standard health insurance policies in India, subject to policy terms, exclusions, waiting periods, and insurer rules. The process may differ slightly across insurers, but the basic principle remains the same.

For most families, the real question is not whether cashless or reimbursement exists. It is which one will work smoothly in their situation, with the least delay and the least pressure on their savings.

Cashless Health Insurance: How It Works

Cashless claim settlement usually starts when you get admitted to a hospital that is part of the insurer’s network. The hospital coordinates with the insurer’s TPA, which is the Third Party Administrator that helps process and verify claims on behalf of the insurer in many cases.

The usual cashless flow looks like this:

- Pre-authorisation request: The hospital sends a request to the insurer or TPA before treatment begins, or soon after emergency admission.

- TPA verification: The TPA checks your policy details, room category, diagnosis, and whether the treatment is covered.

- Insurer approval: The insurer approves the eligible amount, sometimes fully and sometimes partially.

- Direct payment: The insurer pays the hospital for the approved, covered expenses directly.

Cashless settlement is often easier for planned treatment because there is time to share documents, confirm coverage, and get pre-authorisation before admission. In emergencies, it can still work if the hospital and insurer can complete the verification quickly.

When to Use Cashless

Cashless is usually the first choice for planned surgeries, scheduled procedures, and hospitalisation in a network hospital. It reduces the need to arrange a large amount of money at the time of admission.

It is especially helpful when:

- the hospital is in the insurer’s network list,

- you have enough time for pre-authorisation,

- the treatment is planned in advance, and

- you want to reduce upfront financial stress.

Before admission, always verify whether the hospital is truly part of your insurer’s current network. Network status can change, and a quick check with the insurer or TPA can save a lot of confusion later.

Common Myths and Reality

A common myth is that cashless means you pay nothing at all. That is not always true. Cashless does not mean zero out-of-pocket expense.

Many policies do not cover certain non-medical items, such as disposable gloves, masks, PPE kits, consumables, or other items listed by the insurer. These can be billed to the patient even in a cashless admission. Also, if the room rent exceeds your policy limit or a treatment item is only partly covered, you may need to pay the difference.

So, cashless helps with convenience, but it does not remove every cost from the hospital bill.

Reimbursement Claims: The Step-by-Step Process

A reimbursement claim is used when the hospital bill has already been paid by you, and you want the insurer to repay the eligible amount afterward. This often happens when treatment is taken at a non-network hospital, or when cashless approval is not possible for some reason.

The usual reimbursement workflow is:

- Pay the bills: You settle the hospital charges directly at discharge or during treatment.

- Collect documents: Keep all original bills, prescriptions, reports, and discharge papers safely.

- Submit the claim: Send the completed claim form and required documents to the insurer within the policy timeline.

- Review by insurer: The insurer or TPA checks whether the treatment is covered and whether documents are complete.

- Approval and transfer: The approved amount is transferred to your bank account.

Reimbursement is more paperwork-heavy than cashless, but it can be a practical solution when cashless is not available or not approved. It also gives you flexibility to choose any hospital, subject to policy coverage and terms.

Essential Documents Checklist

For reimbursement, document discipline matters a lot. One missing paper can delay the claim or trigger a query.

- Original discharge summary

- Original hospital bills and receipts

- Pharmacy bills

- Investigation and test reports

- Doctor’s prescriptions and consultation notes

- Claim form duly filled and signed

- Cancelled cheque or bank proof for transfer

- Any pre- and post-hospitalisation bills if the policy covers them

A practical tip: keep a separate file or folder for every hospitalisation. Many claim issues happen because families mix bills, lose originals, or submit unclear copies. An organised record can save days of follow-up.

A Quick Comparison of Cashless and Reimbursement

| Feature | Cashless Claim | Reimbursement Claim | Why It Matters |

|---|---|---|---|

| Money flow | Insurer/TPA pays hospital directly | You pay first, insurer repays later | Decides your upfront cash requirement |

| Best for | Planned treatment at network hospital | Non-network hospital or when cashless is not available | Helps choose the right mode before admission |

| Upfront payment | Usually low, but not always zero | High, because you pay full bill first | Important for liquidity planning |

| Paperwork | Moderate | Higher | More documents are needed for reimbursement |

| Speed of settlement | Usually faster at the hospital stage | Usually slower because review happens after discharge | Matters in emergencies and planned surgeries |

| Hospital choice | Limited to network hospitals for smooth approval | More flexible, subject to policy terms | Affects where you can get treatment |

| Risk of delay | Pre-authorisation or TPA approval delays possible | Document gaps and verification delays possible | Helps set expectations correctly |

Which Is Actually Better?

The honest answer is: neither is universally better. The better option depends on the situation.

Cashless is usually better when you want convenience, lower upfront stress, and treatment in a network hospital. It is especially useful for planned procedures where pre-authorisation can be completed in time.

Reimbursement is usually better when the hospital is not in the network, when cashless approval is denied for a technical reason, or when the policy path requires payment first and later settlement.

Here is a simple decision matrix to make the choice easier.

Health Insurance Claim Decision Matrix

| Scenario | Hospital Type | Recommended Claim Mode | Key Benefit |

|---|---|---|---|

| Emergency admission | Network hospital | Cashless, if approval can be obtained quickly | Reduces immediate payment pressure |

| Emergency admission | Non-network hospital | Reimbursement | Allows treatment even when cashless is unavailable |

| Planned surgery | Network hospital | Cashless | Pre-authorisation can reduce hassle at admission |

| Planned treatment | Non-network hospital | Reimbursement | Gives flexibility to choose the doctor or facility |

| Large expected bill | Network hospital | Cashless preferred | Protects your savings and working capital |

| Hospital not in insurer network but treatment cannot wait | Non-network hospital | Reimbursement | Still lets you file a valid claim later |

If you want a practical thumb rule, use this: cashless for convenience, reimbursement for flexibility. But always verify the hospital network status before admission, because that single detail often decides the claim path.

Common Reasons for Claim Rejection or Delay

Common Reasons for Claim Rejection or Delay

Common Reasons for Claim Rejection or Delay

Common Reasons for Claim Rejection or DelayMany claim issues are not about the treatment itself. They happen because of process mistakes, incomplete documents, or policy conditions not being followed.

Common reasons include:

- Incomplete documents: Missing discharge summary, bills, prescriptions, or test reports can delay review.

- Late intimation: Many policies require you to inform the insurer or TPA within a fixed time window, often 24 to 48 hours for emergencies or within the period mentioned in the policy for planned admissions. The exact timeline can vary, so read your policy wording carefully.

- Non-disclosure of pre-existing conditions: If the insurer finds material facts were not shared during policy purchase, the claim can get complicated.

- Non-covered treatment: Some procedures, items, or hospital charges may be excluded by policy terms.

- Mismatch in documents: Names, dates, diagnosis details, or bill amounts that do not match can trigger queries.

- Policy limits exceeded: Room rent limits, sub-limits, or co-payment clauses can reduce the approved amount.

IRDAI has issued guidelines over time to improve claim servicing and cashless access, and the industry is also moving toward broader cashless availability in more situations. Even then, approval still depends on policy conditions, hospital cooperation, and correct documentation. For the latest rules, check your insurer’s policy wording and the official IRDAI updates.

Claim Decision Guide You Can Use Before Admission

| What you should check | Why it matters | What to do |

|---|---|---|

| Is the hospital in the insurer’s network? | It affects cashless approval | Confirm with the insurer, TPA, or hospital help desk before admission |

| Is the treatment planned or emergency? | Planned cases usually allow smoother pre-authorisation | Start documents early for planned admission |

| Can you arrange upfront payment if needed? | Reimbursement requires you to pay first | Keep emergency funds ready where possible |

| Do you have all documents ready? | Missing papers slow down claims | Keep prescriptions, reports, bills, and discharge summary in one file |

| Have you informed the insurer/TPA on time? | Late intimation can affect approval | Notify within the policy timeline mentioned in your document |

For families that want a simple rule, the decision is often this: if the hospital is in-network and the case is planned, choose cashless. If the hospital is out of network or the situation is already over and billed, go for reimbursement.

Frequently Asked Questions

Can I get a cashless claim in a non-network hospital?

Usually, no. Traditional cashless claims are generally available only at network hospitals. If you take treatment at a non-network hospital, reimbursement is usually the standard route. Some insurers are expanding cashless access under newer initiatives, so check the latest policy and insurer updates before admission.

Is it possible to switch from cashless to reimbursement during treatment?

Yes, sometimes it happens. If cashless approval is delayed, denied, or the hospital cannot complete the process, you may have to pay the bills and later file a reimbursement claim. The exact handling depends on the insurer, hospital process, and policy terms.

What are non-medical items in a hospital bill?

Non-medical items are charges that are not directly part of the medical treatment. Examples may include consumables, PPE kits, gloves, masks, certain disposable items, and similar hospital supplies. These are often excluded partly or fully, depending on the policy.

How long does a reimbursement claim take to process?

There is no single fixed timeline because it depends on the insurer, document completeness, and claim complexity. Many claims are processed within the standard timelines mentioned by the insurer, but queries, missing documents, or verification checks can extend the time. Check your policy wording and insurer communication for the current timeline.

Do I need original documents for both types of claims?

Original documents are usually essential for reimbursement claims, especially bills, discharge summary, and reports. For cashless claims, the hospital and insurer may still ask for supporting papers and copies. It is always wise to keep original records safely until the claim is fully settled.