Choosing the best insurance company in India can feel confusing because every insurer claims to offer great coverage, fast claims, and low premiums. But there is no single “best” insurer for everyone. The right choice depends on what you need: a wide hospital network, a simple claim process, a strong branch presence, lower premiums, or better digital service.

For Indian buyers, the first filter should always be regulation. An insurer should be licensed by the IRDAI (Insurance Regulatory and Development Authority of India), because that is the regulator for the insurance sector in India. After that, compare objective factors such as claim settlement record, service network, policy clarity, digital support, and complaint handling. Marketing alone should never decide the purchase.

Insurance is not a product where the cheapest option is always the smartest. A low premium can look attractive today, but the real value shows up when you need a cashless hospital admission, a smooth claim, or support during a stressful time. That is why it helps to compare providers with a practical framework instead of chasing ads or “top 10” lists.

Key Factors to Evaluate Before Choosing an Insurance Company

To compare insurers fairly, look at the things that affect your experience during a claim, not just the premium on the quotation page. A policy may look affordable but become frustrating if the insurer has a weak network, delayed settlements, or unclear exclusions.

These are the most useful factors to check when choosing the best insurance company in india:

Claim Settlement Ratio (CSR) – how many claims the insurer settled compared with the claims it received.

Incurred Claim Ratio (ICR) – the amount the insurer paid out in claims relative to the premiums collected.

Network strength – hospitals for health insurance and garages for motor insurance.

Digital claim process – app support, online tracking, document upload, and communication updates.

Policy wordings – exclusions, waiting periods, room rent limits, sub-limits, and add-on conditions.

Customer support – how easy it is to get help when you need clarification or need to file a claim.

Remember that “best” is subjective. A young salaried person may value low premiums and app-based service, while a family with elderly parents may care more about hospital network and claim speed. Someone buying motor insurance may prioritise garage tie-ups and cashless repairs. Your own need should drive the choice of the best insurance company in india.

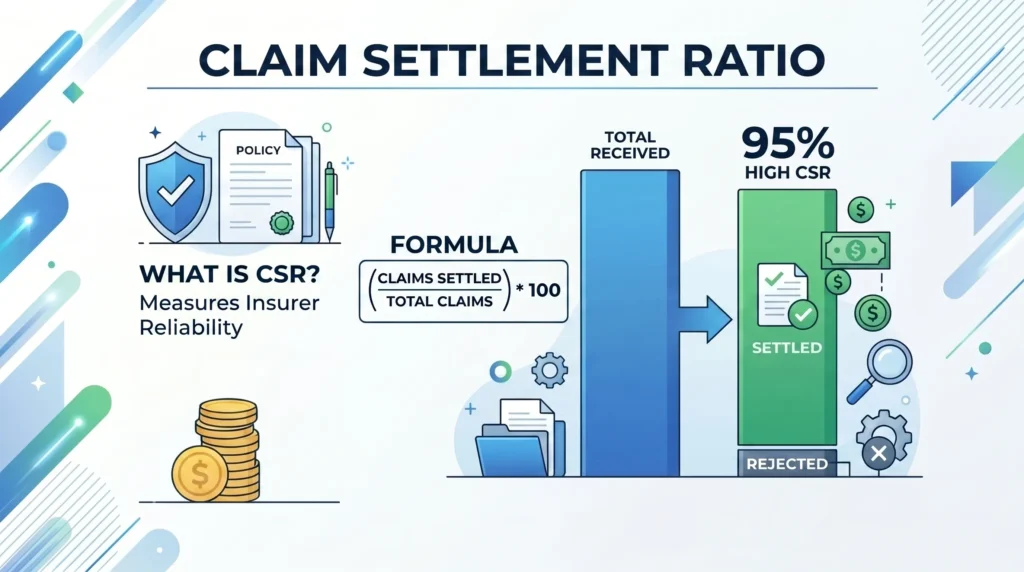

Understanding Claim Settlement Ratio (CSR)

CSR is one of the most widely used metrics in insurance comparison. It shows the number of claims settled by an insurer compared with the total claims received during a specific period. In simple terms, a higher CSR usually suggests that the insurer has a better track record of paying claims, which is important when selecting the best insurance company in india.

But CSR should not be read in isolation. A company with a 100% CSR may have received fewer claims overall, so the number alone does not tell the full story. It is better to look at CSR along with the size of the claim book, the type of policies sold, and how the insurer handles documents and verification.

You should also check whether the claim was settled smoothly or only after repeated follow-ups. A good insurer is not just one that pays claims eventually, but one that makes the process transparent and predictable.

Service Network and Digital Presence

For health insurance, the cashless hospital network matters a lot. If your insurer has a wide network in your city and nearby areas, it becomes easier to get treatment without arranging large upfront payments. This is a key factor when identifying the best insurance company in india.

For motor insurance, a strong garage network can make repairs and cashless settlement simpler.

Digital service is equally important. Many insurers now let you buy policies, upload documents, track claims, and chat with support teams through mobile apps or customer portals. This can save time, especially if you need policy copy downloads, claim status updates, or emergency help.

Still, digital convenience should not replace policy clarity. A fast app does not help much if the policy has strict exclusions or low sub-limits. Use technology as a support tool, not the only reason to buy.

How to Compare Insurance Providers Objectively

Use aggregators for quote comparison, but do not choose only by the lowest premium. Aggregator prices are useful for shortlisting, but the final decision should depend on coverage quality, claim history, and service terms when selecting the best insurance company in india. Sometimes a slightly higher premium gives better hospital network access, fewer restrictions, or easier claims.

s, or easier claims.

The table below can help you compare providers more objectively.

| Feature | Importance | What to Check | Potential Red Flag |

|---|---|---|---|

| Claim Settlement Ratio | High | Recent CSR from official or IRDAI-referenced reports | Very low settlement record or unclear claim data |

| Incurred Claim Ratio | Medium | Whether the insurer is paying a healthy share of premiums as claims | Extremely low ICR without a clear explanation |

| Network hospitals/garages | High | Coverage in your city, locality, and preferred hospitals or garages | Few cashless partners near your location |

| Digital claim process | High | App support, document upload, claim tracking, and communication updates | No clear online process or poor complaint response |

| Policy wording | Very high | Exclusions, waiting periods, sub-limits, room rent caps, add-ons | Vague wording, hidden conditions, or heavy restrictions |

| Premium | Medium | What is included for the price, not just the headline amount | Lowest premium with weak coverage or many exclusions |

| Customer support | High | Call support, grievance handling, turnaround time, and claim updates | Difficult to reach support or repeated delays |

One practical tip: compare at least three insurers side by side on the same coverage amount and similar add-ons. That helps you see whether a cheaper policy is actually offering less protection.

Steps to Verify an Insurance Company’s Credibility

Before you buy, verify the insurer instead of relying only on the seller, agent, or aggregator. This takes only a few minutes and can save you from unpleasant surprises later when choosing the best insurance company in india.

Check the IRDAI authorisation status. Visit the official IRDAI portal or insurer list and confirm that the company is licensed to operate in India. This is an important step in identifying the best insurance company in india.

Look for the insurer’s registration details. The insurer should clearly display its registration number, official name, and contact details on its website and policy documents.

Review recent annual reports or public disclosures. Official reports can help you understand claim trends, business volume, and service-related disclosures.

Read the product brochure and policy wording. Focus on exclusions, waiting periods, co-pay, sub-limits, and claim conditions.

Check complaint and grievance information. See how the insurer handles customer issues and whether it gives clear escalation channels.

Confirm network and service tools. For health and motor insurance, check the current list of cashless hospitals or garages on the official website or app.

If you are comparing a few providers, use the IRDAI annual report and the insurer’s own disclosures together. That gives you a more realistic picture than a sales brochure. Since claim and service data can change, always verify the latest numbers from official sources before making a purchase.

Insurance Provider Comparison & Selection Checklist

Use this simple checklist to identify what matters most to you. It is meant for educational comparison only and is not a recommendation to buy from any specific brand.

| My priority | What I should focus on | What I should ignore |

|---|---|---|

| Affordable premium | Compare price with coverage, exclusions, and sub-limits | Choosing the cheapest policy without checking fine print |

| Wide hospital or garage network | Check network coverage near my home, office, and frequent travel areas | Assuming all cashless partners are equally convenient |

| Fast claim support | Look for clear digital claim tracking and responsive service channels | Relying only on sales promises about quick settlement |

| Strong brand trust | Check regulation, disclosures, and public service records | Buying only because the brand is popular |

| Simple policy terms | Read exclusions, waiting periods, and add-on conditions carefully | Skipping the policy wording because it looks long |

Quick self-check: If you need a large hospital network and quick digital claim filing, focus on service and network first. If your budget is tight, compare price only after you have confirmed that coverage is adequate. If you are buying for family protection, policy wording and exclusions should matter more than promotional discounts.

Common Mistakes to Avoid When Comparing Insurers

Many buyers make the same mistakes when choosing insurance. Avoiding these can improve your chances of getting real value from the policy.

- Buying only because the premium is low. A cheap policy can have high co-pay, limited coverage, or serious exclusions.

- Ignoring waiting periods. Many health policies have waiting periods for pre-existing conditions or specific treatments.

- Skipping sub-limits. Some policies cap expenses such as room rent, ambulance, or day-care procedures.

- Not reading exclusions. If a treatment, situation, or damage is excluded, the claim may be denied even if the policy is active.

- Buying only for tax benefits. Tax savings should be a side benefit, not the main reason for choosing insurance.

- Assuming every claim will be approved. Claim settlement depends on policy terms, documents, disclosures, and insurer verification.

A good rule is simple: if you would be unhappy paying the premium for a full year, the policy may not be the right fit. Insurance should feel understandable, not confusing.

The Role of IRDAI in Protecting Policyholders

IRDAI is the regulator that oversees insurance companies in India. Its role is to make sure insurers follow rules, maintain proper conduct, and treat policyholders fairly. It also publishes regulations, annual reports, and disclosures that can help you compare insurers in a more informed way.

If a claim is wrongfully denied or you are unhappy with the insurer’s response, first use the company’s grievance redressal process. Keep your policy number, claim number, documents, emails, and rejection letters ready. If the issue is not resolved, you can escalate it through the insurer’s grievance mechanism and then use the official complaint channels available through IRDAI and related policyholder grievance systems.

Whenever you see a claim promise that sounds too good, pause and verify the policy terms. Insurance claims are always subject to terms and conditions, and the final outcome depends on the policy wording, documents, exclusions, and verification by the insurer.

Insurance is the subject matter of solicitation.

FAQs

Does a higher Claim Settlement Ratio guarantee my claim will be paid?

No. A higher CSR only shows the insurer’s past settlement performance. Your claim still depends on the policy terms, exclusions, documents, waiting periods, and the facts of the claim. This is important when evaluating the best insurance company in india.

How do I find a list of cashless hospitals or garages for an insurer?

Check the insurer’s official website or mobile app. The cashless network is usually updated there, and you should confirm the list for your city before buying when choosing the best insurance company in india.

Is it better to buy insurance directly from the company or through an aggregator?

Both are valid. What matters most is the policy features, premium, network, and claim support. Use aggregators for comparison, but verify the final policy on the insurer’s official platform.

Can I switch my insurance provider during the policy term?

Usually, you switch at renewal rather than during the active term. Some products may allow portability or continuity benefits, but the process and eligibility depend on the insurer and product rules.

Where can I officially check if an insurance company is authorized in India?

Check the official IRDAI portal or IRDAI-linked insurer listings to confirm that the company is licensed to operate in India.

What should I look for in the policy fine print?

Focus on exclusions, waiting periods, sub-limits, co-pay, room rent limits, claim documents, and any conditions that may affect settlement.