Bonds are one of the most popular fixed-income investment options for individuals who want regular income while taking relatively lower risk than many equity investments. When you invest in a bond, you are essentially lending money to a government, company, or other organization for a specific period. In return, the issuer agrees to pay periodic interest and repay the principal amount on the maturity date.

Bonds play an important role in building a balanced investment portfolio because they provide stability, predictable cash flow, and diversification. While some bonds focus on capital preservation, others aim to offer higher returns or tax advantages. Understanding the different bond categories helps investors choose investments that match their financial goals and risk tolerance.

What Is a Bond?

A bond is a debt instrument issued by governments, companies, financial institutions, or public organizations to raise funds. Investors purchase these bonds and become lenders rather than owners.

Every bond generally includes the following components:

| Component | Meaning |

|---|---|

| Face Value | The amount repaid at maturity. |

| Coupon Rate | The annual interest paid to investors. |

| Maturity Date | The date when the principal is repaid. |

| Issuer | Government, company, or institution issuing the bond. |

Unlike shares, bonds do not provide ownership in the issuing organization. Instead, investors receive fixed or variable interest according to the bond’s terms.

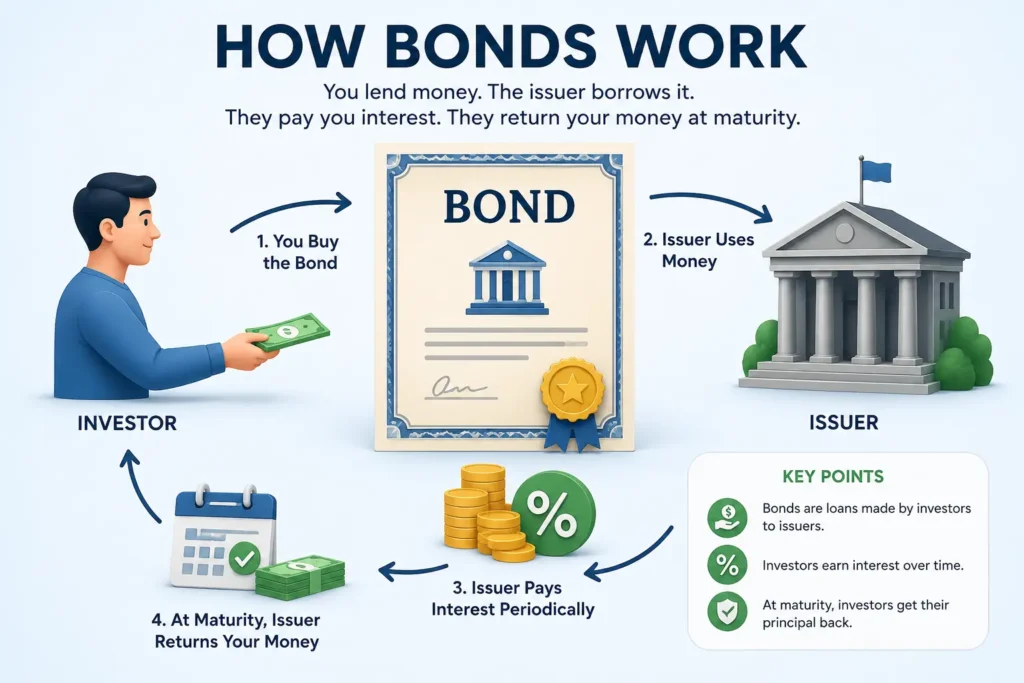

How Bonds Work

The bond investment process is relatively simple:

- A government or company needs funds.

- It issues bonds to investors.

- Investors purchase the bonds.

- The issuer pays periodic interest (coupon payments).

- On maturity, the issuer repays the face value of the bond.

For example, if you buy a bond with a face value of ₹1,00,000 offering a 7% annual coupon for 10 years, you generally receive ₹7,000 each year as interest. At maturity, the issuer returns your original ₹1,00,000.

Why Investors Choose Bonds

Many investors include bonds in their portfolios because they offer several advantages:

- Regular interest income.

- Lower volatility compared to many stocks.

- Better portfolio diversification.

- Capital preservation.

- Suitable for retirement planning and long-term financial goals.

However, returns and risks vary depending on the type of bond you choose.

Major Types of Bonds

The bond market includes several categories, each designed for different investment needs.

| Bond Type | Issuer | Risk Level | Suitable For |

|---|---|---|---|

| Government Bonds | Central or State Government | Low | Conservative investors |

| Corporate Bonds | Companies | Medium to High | Income-focused investors |

| Municipal Bonds | Local Government Bodies | Low to Medium | Long-term investors |

| Sovereign Gold Bonds | Government | Low to Medium | Gold investors |

| Tax-Free Bonds | Government-backed Institutions | Low | Tax-efficient investing |

| Inflation-Indexed Bonds | Government | Low | Inflation protection |

| Zero-Coupon Bonds | Government or Companies | Medium | Long-term investors |

| Convertible Bonds | Companies | Medium | Growth-oriented investors |

| Callable Bonds | Companies/Government | Medium | Yield-seeking investors |

| Puttable Bonds | Companies/Government | Low to Medium | Risk-conscious investors |

Government Bonds

Government bonds are issued by the Central Government or State Governments to finance infrastructure development, public welfare programs, and other government expenditures.

Because they are backed by the government, they are generally considered one of the safest investment options.

Common Types of Government Bonds

Treasury Bills (T-Bills)

Treasury Bills are short-term securities with maturities of up to one year. They are issued at a discount and redeemed at face value.

Government Securities (G-Secs)

Government Securities are long-term bonds that generally pay interest every six months and are widely used by banks, insurance companies, and retail investors.

State Development Loans (SDLs)

SDLs are issued by State Governments to fund development projects. They often provide slightly higher yields than Central Government securities.

Floating Rate Bonds

These bonds have interest rates that change periodically according to a predetermined benchmark instead of remaining fixed throughout the investment period.

Advantages

- Very low default risk.

- Stable income.

- Suitable for conservative investors.

- Portfolio diversification.

Limitations

- Lower returns than many corporate bonds.

- Sensitive to interest rate changes.

- Long maturities may reduce liquidity.

Corporate Bonds

Corporate bonds are issued by private and public companies to raise money for business expansion, refinancing debt, purchasing equipment, or funding new projects.

Since companies carry greater credit risk than governments, corporate bonds generally offer higher interest rates.

Types of Corporate Bonds

Investment-Grade Bonds

Issued by financially strong companies with high credit ratings.

Features

- Lower default risk.

- Stable returns.

- Suitable for conservative investors.

High-Yield Bonds

Issued by companies with lower credit ratings.

Features

- Higher interest rates.

- Greater return potential.

- Higher investment risk.

Advantages

- Better returns than many government bonds.

- Regular coupon payments.

- Variety of investment options.

- Tradable in the secondary market.

Limitations

- Credit risk.

- Interest rate risk.

- Company performance affects repayment ability.

Municipal Bonds

Municipal bonds are issued by local governments and municipal authorities to finance public infrastructure projects such as roads, hospitals, schools, public transport systems, and water supply networks.

Benefits

- Relatively lower risk.

- Supports public infrastructure.

- Suitable for long-term investing.

- Stable income potential.

Limitations

- Limited availability.

- Moderate returns.

- Liquidity depends on the bond issue.

Sovereign Gold Bonds (SGBs)

Sovereign Gold Bonds allow investors to invest in gold without purchasing physical gold.

These government-backed securities are linked to the market price of gold while also providing periodic interest.

Advantages

- No storage concerns.

- No purity issues.

- Government-backed investment.

- Portfolio diversification.

- Exposure to gold prices.

Limitations

- Returns depend on gold prices.

- Long investment horizon.

- Market liquidity may vary.

Latest Update: Although fresh issuances have been limited recently, existing Sovereign Gold Bonds continue to be traded in the secondary market, allowing investors to buy or sell them through eligible exchanges.

Tax-Free Bonds

Tax-Free Bonds are generally issued by government-backed organizations to finance infrastructure and development projects.

Their primary advantage is that the interest income is generally exempt from income tax according to the terms of the specific bond issue.

Advantages

- Tax-efficient income.

- Stable returns.

- Lower credit risk.

- Suitable for investors in higher tax brackets.

Limitations

- Limited availability.

- Lower coupon rates than some corporate bonds.

Inflation-Indexed Bonds

Inflation reduces the purchasing power of money over time.

Inflation-indexed bonds are designed to reduce this impact by linking certain features of the bond to inflation.

These bonds may help investors preserve the real value of their investments during periods of rising prices.

Zero-Coupon Bonds

Unlike regular bonds, zero-coupon bonds do not pay periodic interest.

Instead, they are issued at a discount and redeemed at face value upon maturity.

| Purchase Price | Maturity Value |

|---|---|

| ₹70,000 | ₹1,00,000 |

The difference between the purchase price and maturity value represents the investor’s return.

Convertible Bonds

Convertible bonds combine features of debt and equity.

Initially, they function like ordinary corporate bonds by paying interest. Under predefined terms, investors may convert them into shares of the issuing company.

Benefits

- Regular income.

- Potential capital appreciation.

- Opportunity to participate in company growth.

Drawbacks

- Lower coupon rates.

- Conversion depends on market conditions.

- Share prices may not always rise.

Callable Bonds

Callable bonds allow the issuer to redeem the bond before its maturity date.

Issuers often exercise this option when market interest rates decline, enabling them to refinance at lower borrowing costs.

Advantages

- Usually offer slightly higher interest rates.

- Attractive during stable interest rate environments.

Risks

- Early redemption.

- Reduced future interest income.

- Reinvestment at lower interest rates.

Puttable Bonds

Puttable bonds provide investors with the right to sell the bond back to the issuer before maturity under specified conditions.

This feature offers additional flexibility and protection if market conditions become unfavorable.

Advantages

- Greater investor protection.

- Improved flexibility.

- Reduced downside risk.

Limitations

- Lower coupon rates than comparable callable bonds.

- Less commonly available in the market.

Comparison of Major Bond Categories

| Bond Type | Risk | Return Potential | Best For |

|---|---|---|---|

| Government Bonds | Low | Moderate | Conservative investors |

| Corporate Bonds | Medium to High | High | Income-focused investors |

| Municipal Bonds | Low to Medium | Moderate | Long-term investors |

| Sovereign Gold Bonds | Low to Medium | Moderate | Gold investors |

| Tax-Free Bonds | Low | Moderate | Tax-efficient investing |

| Inflation-Indexed Bonds | Low | Moderate | Inflation protection |

| Zero-Coupon Bonds | Medium | Moderate | Long-term wealth creation |

| Convertible Bonds | Medium | Moderate to High | Growth-oriented investors |

| Callable Bonds | Medium | Moderate | Yield-seeking investors |

| Puttable Bonds | Low to Medium | Moderate | Risk-conscious investors |

Conclusion

Bonds are an essential part of a well-diversified investment portfolio, offering a balance between stability, regular income, and capital preservation. From low-risk government bonds to higher-yield corporate bonds and specialized options like Sovereign Gold Bonds, tax-free bonds, and inflation-indexed bonds, each bond category serves a different investment purpose.

Understanding how these bond types work, along with their benefits and potential risks, can help you make more informed investment decisions. Instead of focusing only on returns, consider factors such as credit quality, maturity period, liquidity, and your long-term financial objectives before investing.

Whether you’re a beginner building your first investment portfolio or an experienced investor looking to diversify, selecting the right mix of bonds can support your financial goals while helping manage overall portfolio risk.