Many people in India first hear about life insurance during tax-saving season. A colleague, relative, or agent may say, “Buy a policy and save tax under Section 80C.” While tax benefits can be useful, they are not the main reason to buy life insurance. The real answer to why life insurance is important is simple: it protects your family’s financial life if your income suddenly stops due to an unfortunate death.

Life insurance is a contract between the insurer and the policyholder. The insurer promises to pay a specified benefit to the nominee if the insured person passes away during the policy term, subject to the policy terms, exclusions, disclosures, and premium payment conditions. In practical terms, it is an income replacement tool for the people who depend on you.

For a salaried employee, self-employed person, or small business owner, the monthly income often supports many commitments: rent or home loan EMI, school fees, groceries, medical costs, parent care, and future goals. Life insurance cannot remove the emotional loss of a family member, but it can reduce the financial shock that follows.

Understanding Why Life Insurance Is Important for Your Financial Security

Financial planning usually starts with one question: “What happens to my family if I am not there to earn?” If you have dependents, life insurance is one of the first layers of protection you should understand.

The core purpose of life insurance is income replacement. It creates a financial backup for your family so they can continue essential expenses, repay liabilities, and protect long-term goals. This is especially important in Indian households where one person may support a spouse, children, parents, or even siblings.

For example, assume a 35-year-old earning member pays the home loan EMI, children’s school fees, and monthly household expenses. If that person passes away unexpectedly, the family may face two losses at once: emotional distress and loss of regular income. A suitable life insurance cover can provide a lump sum that helps the family manage expenses without being forced into distress decisions such as selling a home, breaking long-term savings, or taking high-interest loans.

Life insurance should not be seen as a way to make profits. It is a financial safety net. Its purpose is to help the family maintain dignity, stability, and choice during a difficult time.

Protection Against Financial Liability

Debt is one of the biggest reasons life insurance matters. Many families today have home loans, car loans, education loans, business loans, or personal loans. If the main borrower dies, the lender still has the right to recover the outstanding amount as per the loan agreement. The burden may fall on the surviving family members, co-borrowers, or guarantors.

A life insurance policy can act as a shield against this liability. If the cover amount is adequate, the family can use the claim amount to close or reduce major debts. This helps prevent a debt trap and protects important assets such as the family home.

Consider a simple example. A person has an outstanding home loan of Rs. 45 lakh and also supports monthly family expenses. If the person has only Rs. 10 lakh of life cover, the policy may not be enough to clear the loan, let alone support the family. This is under-insurance. The policy exists, but the protection gap remains.

When choosing life insurance, always consider outstanding liabilities. This includes the loan principal, unpaid interest, and any financial obligations that your family may not be able to handle comfortably without your income.

Securing Your Family’s Future Milestones

Life insurance also protects future goals. These goals may include children’s education, children’s marriage, spouse’s retirement, care for dependent parents, or maintaining a basic standard of living.

Many Indian families plan for education expenses years in advance. School fees, college fees, coaching costs, hostel expenses, and professional courses can increase over time due to inflation. If the earning member is no longer around, these goals can get delayed or compromised.

A good life insurance cover gives the surviving family a pool of money to continue important milestones. It does not guarantee that every dream will be fully funded, because that depends on the cover amount, inflation, expenses, and how the money is managed. But it can give the family more breathing room and reduce the need to make rushed financial choices.

This is why life insurance should be linked to family responsibilities, not just to annual tax planning. If your family depends on your income, your life cover should reflect the size of that responsibility.

Helpful Interactive Tool or Visual to Add

Use this simple Life Insurance Necessity Checklist as a “Protection Gap” evaluator. It is not a calculator and does not give a personalised recommendation. It helps you think through whether your family may need income replacement, debt protection, or goal security.

| Check | Your Situation | What It May Indicate |

|---|---|---|

| [ ] | I have dependent parents | You may need income replacement and medical support planning for parents. |

| [ ] | I have a spouse who depends partly or fully on my income | You may need cover to protect household expenses and long-term stability. |

| [ ] | I have children or plan to fund a child’s education | You may need goal security for education and future milestones. |

| [ ] | I have an outstanding home loan, car loan, personal loan, or business loan | You may need debt protection so your family is not forced to repay large liabilities alone. |

| [ ] | My savings and investments are not enough to support my family for many years | You may have a protection gap that life insurance can help reduce. |

| [ ] | My family has enough assets, no debt, and no financial dependence on my income | Your insurance need may be lower, but you should still review your situation carefully. |

Educational note: This checklist is for educational purposes only and does not constitute financial advice. Your actual insurance need depends on income, age, health, liabilities, assets, lifestyle, dependents, and future goals. Consult a qualified financial professional if you need a personalised assessment.

Why Life Insurance Is Not Just a Tax-Saving Option

Tax benefits are often the most advertised feature of life insurance, but they should not be the primary reason to buy a policy. Under the Income Tax Act, premiums may qualify for deduction under Section 80C subject to applicable limits, conditions, and the tax regime chosen by the taxpayer. Tax rules can change, so always verify the latest rules from the Income Tax Department or consult a tax professional.

The bigger point is this: a tax-saving product may not always provide adequate protection. If you buy a policy only to save tax, you may end up with a low sum assured, high premium, or a plan that does not match your family’s real needs.

Life insurance has two broad roles that people often mix up:

- Insurance as protection: The main aim is to provide a large cover at an affordable premium. Term insurance is the common example.

- Insurance as investment or savings: Some plans combine insurance with savings or market-linked investment features, such as endowment plans or ULIPs. These may have different costs, benefits, lock-ins, risks, and returns.

There is nothing wrong with understanding different products. But beginners should first be clear about the basic protection need. If your family needs Rs. 1 crore of protection and you buy a policy that gives only Rs. 5 lakh or Rs. 10 lakh of life cover, the tax deduction will not solve your family’s financial risk.

IRDAI, the insurance regulator in India, encourages transparency and policyholder awareness. Still, the responsibility to read the policy document carefully remains with the buyer. Before paying the premium, check the benefit illustration, premium payment term, policy term, exclusions, surrender conditions, waiting periods if any, claim process, and nominee details.

Key Factors to Consider Before Buying Life Insurance

Buying life insurance should not be rushed. The right policy depends on your family structure, income, liabilities, health, and goals. A policy that suits your friend may not suit you.

Here are the key factors to review before purchasing life cover:

| Factor | Why It Matters | What to Check |

|---|---|---|

| Sum assured | This is the amount your nominee may receive if a valid claim is approved. | Check whether it can replace income, repay debts, and support goals. |

| Policy term | Protection should ideally cover your earning years and key family responsibilities. | Check whether the policy lasts until loans are repaid and children become financially independent. |

| Premium affordability | A policy helps only if premiums are paid regularly. | Choose a premium you can continue comfortably without missing payments. |

| Health disclosure | Incorrect or incomplete disclosure can create claim problems later. | Disclose medical history, smoking, alcohol use, occupation risks, and existing policies truthfully. |

| Exclusions and conditions | Every policy has terms and exclusions. | Read the official policy wording, not only the brochure or sales pitch. |

| Claim process | Your nominee should know how to file a claim. | Check required documents, nominee details, and insurer communication channels. |

Premiums can differ based on age, health, lifestyle habits, occupation, sum assured, policy term, and insurer underwriting rules. A younger, healthier applicant may generally get a lower premium than someone older or with higher health risks, but the final premium depends on the insurer’s assessment.

Determining the Right Sum Assured

The right sum assured is not a random number. It should be linked to your Human Life Value, often called HLV. In simple terms, HLV estimates the financial value of your future income for your dependents, after considering expenses, liabilities, and goals.

A commonly used thumb rule is to have life cover of around 10 to 15 times your annual income. For example, if your annual income is Rs. 10 lakh, a rough starting point may be Rs. 1 crore to Rs. 1.5 crore of cover. This is only a broad rule, not personalised advice.

You may need higher cover if you have young children, a large home loan, dependent parents, limited savings, or a single-income household. You may need lower cover if you have no dependents, no debt, and enough assets to support your family.

While calculating cover, consider:

- Outstanding loans and other liabilities

- Annual household expenses

- Years for which your family may need support

- Children’s education and other future goals

- Existing savings, investments, provident fund, and other assets

- Inflation, because expenses usually rise over time

Do not assume that a small policy bought years ago is still enough. Review your cover after major life events such as marriage, childbirth, taking a home loan, a major salary increase, or starting a business.

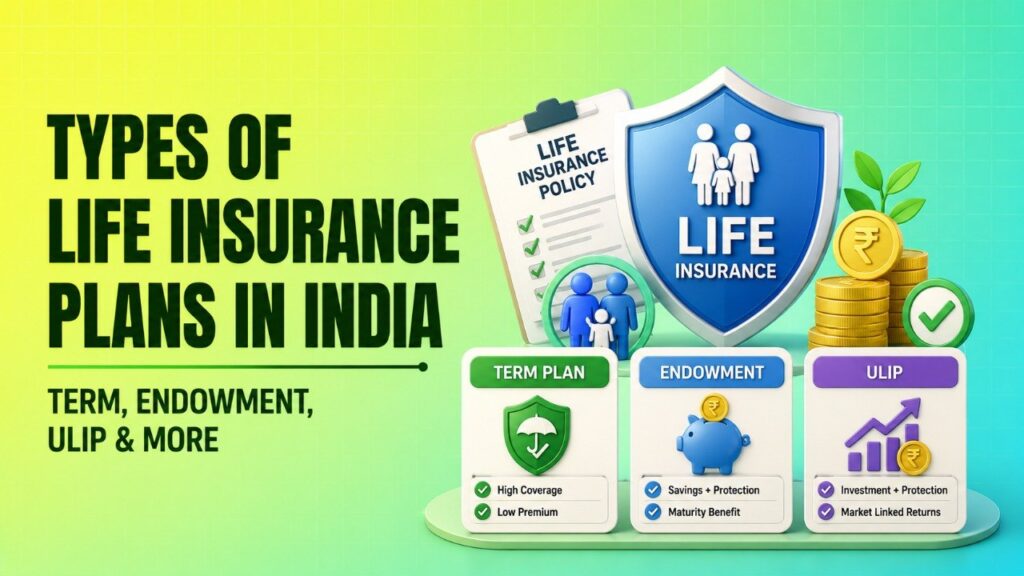

Understanding Different Types of Life Insurance

Life insurance products can look confusing because different plans combine protection, savings, and investment in different ways. For beginners, the simplest distinction is between pure protection and bundled products.

Term insurance is pure protection. It usually provides a large life cover for a fixed period at a relatively lower premium compared to many savings-linked policies. If the insured person dies during the policy term and the claim is valid, the nominee receives the sum assured. If the insured person survives the term, a regular term plan usually does not pay a maturity benefit, unless it is a return-of-premium variant with different pricing and terms.

Endowment plans combine life cover with a savings component. They may provide a maturity benefit if the policyholder survives the term, subject to terms. The life cover may be lower for the same premium compared to a term plan.

ULIPs combine life insurance with market-linked investment. Returns are not fixed and depend on fund performance, charges, and market conditions. Investment products linked to markets carry risk, so the buyer must understand costs, lock-in, fund options, and suitability.

For many beginners with dependents, a term insurance plan is often the first product to understand because it focuses on protection. However, suitability depends on personal needs, so compare policy wording, premiums, exclusions, claim process, and insurer details before deciding.

Common Mistakes to Avoid When Purchasing Life Insurance

Life insurance is a long-term commitment. A small mistake at the buying stage can affect your family later. Avoid these common errors:

- Buying too little cover: A policy with a small sum assured may give emotional comfort but not enough financial support. Calculate liabilities and future expenses before choosing cover.

- Buying only for tax saving: Section 80C benefit, if available under current tax rules, is a bonus. Protection should be the main purpose.

- Hiding medical history: Do not hide diabetes, blood pressure, surgeries, smoking, alcohol use, or other health details. Non-disclosure can create claim complications as per policy terms and insurance laws.

- Ignoring policy exclusions: Read the policy document carefully. Check exclusions, suicide clause, waiting conditions if any, premium payment rules, and claim requirements.

- Choosing based on a friend’s advice: Your friend’s income, health, loans, family responsibilities, and goals may be different from yours.

- Not informing the nominee: Your nominee should know the policy exists, where documents are stored, and how to contact the insurer.

- Letting the policy lapse: If premiums are not paid on time, the policy can lapse after the grace period. A lapsed policy may not provide the intended protection.

Also be careful with verbal promises. What matters is the official policy wording, benefit illustration, proposal form, premium receipt, and insurer communication. If something is important, get it confirmed in writing from the insurer or authorised channel.

Before publishing or acting on any insurance information, check the latest IRDAI public awareness messages and insurer disclosures. Insurance rules, tax provisions, product features, and claim procedures may change over time.

FAQs

1. Is life insurance mandatory in India?

No, life insurance is not mandatory for everyone in India. However, it is an important part of financial planning if you have dependents, loans, or family goals that rely on your income.

2. How much life insurance cover do I actually need?

A common thumb rule is to consider life cover of around 10 to 15 times your annual income. You should also add outstanding loans, future goals, and inflation, and subtract existing assets that can support your family.

3. Can I have more than one life insurance policy?

Yes, you can have more than one life insurance policy. You should disclose existing policies when applying for a new one, because insurers assess total cover based on income, age, health, and underwriting rules.

4. What happens to my life insurance if I stop paying premiums?

If you stop paying premiums, the policy may lapse after the grace period. A lapsed policy may not provide life cover. Some policies may have revival options or paid-up benefits, but these depend on the policy terms.

5. Does life insurance cover accidental death?

Most life insurance policies generally cover death due to accident, subject to policy terms and exclusions. Some policies also offer an accidental death benefit rider. Always read the policy wording to understand what is covered and what is excluded.

Life insurance is not about fear. It is about responsibility. If your income supports your family, the right life cover can help protect them from financial hardship during an already difficult time. Treat it as a protection tool first, review it regularly, and read every policy document carefully before you buy.