Is your CIBIL score 700 and you’re wondering whether it’s good enough to get a loan or credit card? You’re not alone. Many people in India fall into this range and feel confused about where they stand.

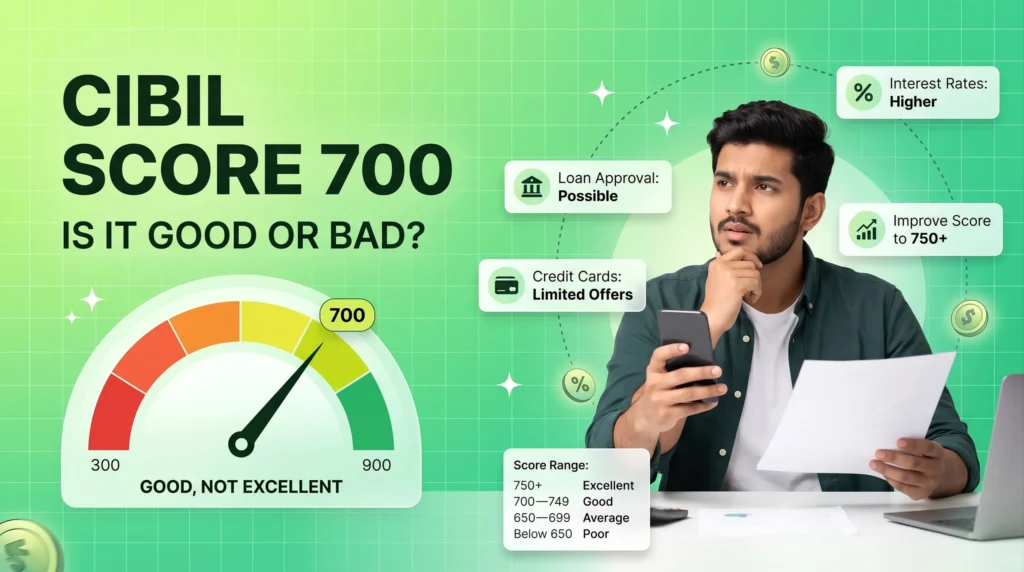

Here’s the simple answer: a 700 CIBIL score is considered good, but not excellent. It puts you in a relatively safe zone for loan approvals, but it may not get you the best interest rates or premium offers.

In this guide, you’ll learn what a 700 score really means, how lenders see it, what loans you can get, and how to improve it to 750+ for better financial benefits.

What is a CIBIL Score?

A CIBIL score is a three-digit number ranging from 300 to 900, used by banks and financial institutions to evaluate your creditworthiness. It is generated by TransUnion CIBIL based on your credit history, including loans, credit cards, and repayment behavior.

The higher your score, the more trustworthy you appear to lenders. A strong credit score increases your chances of loan approval and helps you secure lower interest rates.

Is 700 CIBIL Score Good or Bad?

A 700 score is generally considered good, but it sits just below the “excellent” category that lenders prefer.

Credit Score Range in India:

| Score Range | Rating |

|---|---|

| 750+ | Excellent |

| 700–749 | Good |

| 650–699 | Average |

| Below 650 | Poor |

Most banks and NBFCs prefer borrowers with a score of 750 or above, as they are seen as low-risk customers. With a 700 score, you are still eligible for loans, but you may not get the best deals.

700 vs 750+ CIBIL Score: What’s the Difference?

The difference between a 700 score and a 750+ score may seem small, but it can have a significant impact on your financial opportunities.

With a 750+ score, you are more likely to:

- Get faster loan approvals

- Enjoy lower interest rates

- Receive pre-approved offers

- Have better negotiation power

With a 700 score, you may:

- Get loan approval, but with slightly higher interest rates

- Have limited access to premium credit cards

- Face stricter verification checks

This is why improving your score even slightly can make a big difference.

What Can You Get with a 700 CIBIL Score?

A 700 score still gives you access to most financial products, but terms may vary.

- Personal Loan: Likely approved, but interest rates may be higher. You can also explore a personal loan with Aadhar card as a convenient option if you need quick funds.

- Car Loan: High chances of approval

- Home Loan: Possible, but depends on income and other factors

- Credit Cards: Mid-range cards with average benefits

Example:

If your monthly salary is ₹40,000 and you already pay ₹10,000 in EMIs, your loan eligibility may be limited despite having a 700 score. This is because lenders also evaluate your repayment capacity.

How Banks Evaluate Your Loan Eligibility (Beyond Score)

Your CIBIL score is important, but it is not the only factor lenders consider.

Banks also evaluate several other aspects:

- Income level: Higher income improves your loan eligibility

- Job stability: Salaried professionals with stable employment are preferred

- Existing EMIs: Too many ongoing obligations can reduce your chances

- FOIR (Fixed Obligation to Income Ratio): This represents the percentage of your income already committed to EMIs. Most lenders prefer it to be below 40–50%

So even with a 700 score, your loan approval depends on your overall financial profile.

Why Your CIBIL Score is Around 700

If your score is stuck at 700, there are usually a few common reasons behind it:

- Occasional late payments on EMIs or credit cards

- High credit utilization (using more than 30% of your credit limit)

- Short credit history

- Multiple loan or credit card applications in a short time

- A past loan settlement impact on CIBIL — if you have ever settled a loan instead of fully repaying it, it can significantly pull down your score and keep it stuck in this range

Identifying these issues is the first step toward improving your score.

Pros and Cons of a 700 CIBIL Score

Pros:

- Decent chances of loan approval

- Considered a relatively low-risk borrower

- Eligible for most financial products

Cons:

- Higher interest rates compared to 750+ score

- Lower loan amount eligibility

- Limited access to premium offers

How to Improve Your CIBIL Score from 700 to 750+

Improving your credit score is not difficult if you follow the right steps consistently.

- Pay all EMIs and credit card bills on time

- Keep credit utilization below 30%

- Avoid applying for multiple loans at once

- Maintain old credit accounts to build history

- Check your credit report regularly for errors

With disciplined habits, you can improve your score within 3–6 months.

Common Mistakes That Keep Your Score at 700

Many people unknowingly make mistakes that prevent their score from increasing:

- Paying only the minimum due on credit cards

- Maxing out credit limits

- Frequently applying for loans

- Closing old credit cards

Avoiding these habits can help you move into the excellent category faster.

Conclusion

A 700 CIBIL score is considered good, but not excellent. It allows you to access loans and credit, but you may not get the most attractive interest rates or premium offers.

If you want better financial opportunities, aim to improve your score to 750 or above. Small changes in your financial habits can make a significant difference over time.

Start by paying your dues on time, managing your credit wisely, and monitoring your credit report regularly.

FAQs

Is a 700 CIBIL score good for a car loan?

Yes, a 700 CIBIL score is generally sufficient for a car loan. However, the interest rate offered may not be the lowest compared to higher scores.

Can I get a personal loan with a 700 CIBIL score?

Yes, most lenders are likely to approve a personal loan with a 700 score, but the terms will depend on your income, job stability, and existing EMIs.

How long does it take to improve a CIBIL score from 700 to 750?

It typically takes around 3 to 6 months, provided you follow consistent financial discipline such as timely payments and low credit utilization.

Is a 700 CIBIL score considered bad?

No, a 700 score is considered good, but it is not in the excellent range.

Which banks accept a 700 CIBIL score?

Most banks and NBFCs accept a 700 score, but loan approval depends on your overall financial profile.