Insurance is a financial protection tool that helps you manage risk. It is not an investment product in the usual sense, but a safety net that can protect your money, family, health, and assets when something unexpected happens. In simple terms, insurance is a legal contract between the insured person and the insurer, where the insurer agrees to pay for covered losses in return for a premium.

For Indian consumers, understanding what is insurance is important because medical emergencies, accidents, disability, vehicle damage, or loss of income can create sudden financial pressure. A properly chosen policy can reduce that burden. But to use insurance well, you need to understand how it works, what it covers, what it excludes, and what to check before buying.

Understanding What Insurance Is and How It Works

Insurance works on two simple ideas: risk transfer and risk pooling. Risk transfer means you shift a part of your financial risk to the insurer. Risk pooling means many people pay premiums into a common pool, and that pool is used to pay the claims of the few people who face a covered loss.

Here is a simple example. Suppose 1,000 people buy the same type of policy and each pays a small premium. Most of them may not make a claim in that year. If one person is hospitalised or suffers a loss covered by the policy, the insurer pays that claim from the pooled money. This is why insurance is affordable for many people even when the claim amount can be large.

The premium is the amount you pay for the policy, usually monthly, quarterly, half-yearly, or yearly. The sum insured is the maximum amount the insurer will pay under the policy, subject to policy terms, exclusions, deductibles, and co-payment conditions.

Why Do You Need Insurance?

You need insurance because life is uncertain. A medical emergency, sudden death in the family, accident, fire, theft, or major repair can cause a financial shock. Insurance helps reduce the chance that one event will wipe out your savings or force you to borrow at a bad time.

For example, if a family’s main earning member dies unexpectedly, term life insurance can help the dependents manage living costs, EMIs, school fees, and other essential expenses. Similarly, health insurance can protect your savings from a large hospital bill. Motor and property insurance can help you recover from damage to your vehicle or home.

Insurance does not prevent the event from happening. It helps you absorb the financial impact of the event.

The Core Components of an Insurance Policy

Before buying any policy, it helps to understand the basic terms used in insurance documents. These terms appear in the policy wording, proposal form, schedule, and claim documents.

- Policyholder: The person who buys the policy and pays the premium.

- Insured: The person or asset covered under the policy. In many cases, the policyholder and insured are the same, but not always.

- Insurer: The insurance company that provides the coverage.

- Premium: The amount you pay for the policy.

- Sum insured / Sum assured: The maximum amount payable under the policy, depending on the product type and terms.

- Deductible: A fixed amount you must pay first before the insurer pays the remaining covered amount.

- Co-payment: A percentage of the claim amount that you must pay yourself, often seen in some health insurance policies.

Types of Insurance Policies in India

In India, insurance is broadly grouped into four major categories: life insurance, health insurance, motor insurance, and asset/liability insurance. Each category serves a different purpose, and the right mix depends on your life stage, family responsibilities, and financial exposure.

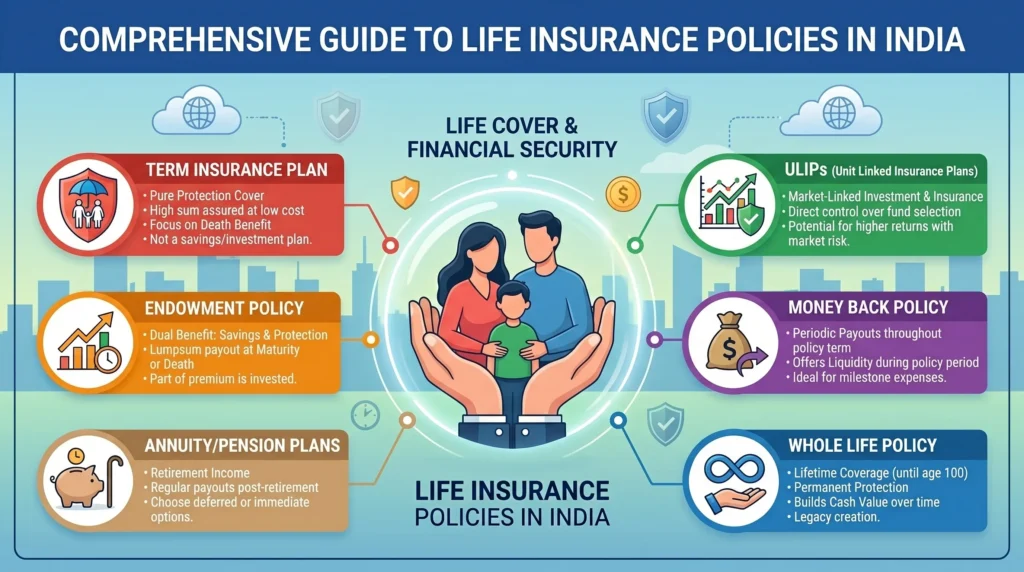

Life Insurance: The Protection Pillar

Life insurance is meant to protect dependents financially if the insured person dies during the policy term. The most straightforward form is term insurance. It provides a high cover for a relatively low premium and is designed mainly for protection.

Other life insurance products such as endowment plans and ULIPs combine insurance with savings or investment features. These may appeal to some buyers, but protection should usually be the primary goal if you are looking for family security. ULIPs are market-linked, so returns are not guaranteed and depend on fund performance and charges.

If your main goal is financial protection for your family, term insurance is usually easier to understand because most of the premium goes towards risk cover rather than investment features.

Health Insurance

Health insurance helps pay for hospitalisation and related medical expenses, depending on the policy. Common types include individual health plans, family floater plans, and critical illness plans.

- Individual plan: One insured person gets a separate sum insured.

- Family floater: One sum insured is shared by the family members covered under the policy.

- Critical illness plan: Provides a lump-sum payout on diagnosis of specified serious illnesses, subject to policy terms.

Health insurance often includes waiting periods. A waiting period is the time during which certain conditions are not covered. This may apply to pre-existing diseases, specific surgeries, maternity benefits, or certain illnesses. It is important to read the policy wording because waiting periods can vary from one insurer and product to another.

Motor and Property Insurance

Motor insurance is important because third-party motor insurance is mandatory in India for vehicles as per law. It covers liability for injury, death, or property damage caused to a third party. Comprehensive motor insurance usually adds own-damage cover for your vehicle, subject to the policy terms.

Property or home insurance can help cover damage due to fire, theft, natural calamities, or other covered events. The exact coverage depends on the policy wording and the risks insured. Many people ignore property insurance until something goes wrong, but it can be useful for homeowners and even for those who want to protect valuable contents inside the home.

Insurance Coverage Checklist

The checklist below can help you think through whether your basic cover is in place. This checklist is for educational purposes only. It does not constitute financial advice. Assess your personal risk and consult a professional advisor if needed.

| Coverage Area | Do You Have It? | What to Review |

|---|---|---|

| Life Insurance | Yes / No | Check if the sum assured is enough for your family’s living expenses, EMIs, and future goals. |

| Health Insurance | Yes / No | Check sum insured, room rent limits, waiting periods, and pre-existing disease coverage. |

| Motor Insurance | Yes / No | Check if you have at least the mandatory third-party cover and whether own-damage protection is needed. |

| Personal Accident Cover | Yes / No | Check whether accidental death, disability, and income protection benefits are included. |

Suggested review: If you only have one type of cover, you may still have a protection gap. For example, a person may have term insurance but no health insurance, or health insurance but no personal accident cover. Review your risk exposure based on your age, income, dependents, and liabilities.

How to Choose the Right Insurance Policy

Choosing insurance is not just about finding the cheapest premium. It is about matching the policy to your actual need, family responsibilities, and financial risk. A low-cost policy can still be a poor choice if the coverage is too small or the exclusions are too wide.

| Factor | Why It Matters | What to Check |

|---|---|---|

| Need vs. Want | Not every insurance product is essential for every person. | Ask whether the policy protects a real financial risk or is being bought only for a tax benefit or sales pitch. |

| Coverage Amount | Too little coverage may not help during a real loss. | Check if the sum insured or sum assured is enough for your income, liabilities, and dependents. |

| Premium | Premium should be affordable over the long term. | See whether the premium fits your budget without causing missed payments. |

| Exclusions | Exclusions define what the policy will not pay for. | Read the exclusions section carefully in the policy wording. |

| Waiting Periods | Some claims are not covered immediately. | Check the waiting period for pre-existing conditions, maternity, or specific illnesses. |

| Claim Settlement Ratio | It is a reference point for an insurer’s past claim experience. | Use it as one factor only. It is not a promise that your future claim will be approved. |

| Riders / Add-ons | Extra benefits can improve coverage. | See whether riders like accidental death, disability, or critical illness are actually useful for your situation. |

| Policy Wording | This is the legal document that decides coverage. | Read the proposal form, policy schedule, and exclusions before you buy. |

A good habit is to compare the policy wording, not just the advertisement. Insurance is a contract of utmost good faith (Uberrimae Fidei), which means both the buyer and the insurer must disclose relevant facts honestly.

Also verify whether the insurer is registered and active through the official IRDAI website or other official insurer resources. Avoid offers that promise “guaranteed claim approval” or push you to skip reading the fine print.

The Insurance Claim Process: What You Should Know

Although claim procedures can differ by product and insurer, the general process usually follows a few common steps. Knowing these steps in advance makes the process smoother if you ever need to file a claim.

- Intimation: Inform the insurer as soon as possible after the event happens. Many policies require prompt claim intimation.

- Documentation: Submit the required documents, such as the policy copy, ID proof, hospital bills, discharge summary, FIR in case of theft or accident, repair estimates, or death certificate, depending on the claim type.

- Survey or investigation: For non-life claims such as motor or property damage, the insurer may appoint a surveyor or investigator to assess the loss.

- Assessment and settlement: The insurer reviews the documents, verifies the claim against policy terms, and then settles, partially settles, or rejects the claim based on coverage and eligibility.

For health insurance, cashless claims may be available at network hospitals, subject to pre-authorisation and policy terms. For reimbursement claims, you usually pay first and then claim later using bills and supporting documents.

The most important point is to disclose facts correctly at the time of buying the policy and when making a claim. Non-disclosure of pre-existing conditions, incorrect answers in the proposal form, or missing documents can delay or weaken a claim.

Common Mistakes to Avoid When Buying Insurance

- Buying only for tax saving: Tax benefits may be available in some cases, but insurance should first solve a real protection need.

- Under-insuring: A very low sum insured may look affordable but may not help enough in a major loss.

- Over-insuring: Paying for too much cover without understanding the purpose can make premiums unnecessarily expensive.

- Ignoring riders: Some riders can be useful, but only if they fit your actual risk. Do not add them blindly.

- Not disclosing medical history: Hiding pre-existing diseases or other material facts can create claim issues later.

- Skipping exclusions: Many claim disputes start because the buyer did not read what was excluded.

- Focusing only on premium: The cheapest policy is not always the best one if the coverage is weak.

- Ignoring policy lapse risk: Missing premium payments may lead to lapse or reduced benefits after the grace period ends.

Another common mistake is treating insurance like an investment. Protection and investment are different goals. Insurance protects against a loss. Investment aims to grow wealth. Some products may combine both, but the combined structure may involve charges, lock-ins, and market risk. That is why you should understand the product before signing up.

As a practical rule, first ask: “What risk am I trying to protect?” Then ask: “Which policy documents prove that this risk is covered?”

FAQ

1. Is insurance an investment?

No. Insurance is primarily a protection tool, not an investment. Its main purpose is to cover financial risk from events like death, illness, accident, theft, or damage. Some products, such as ULIPs or endowment plans, may include investment or savings features, but they are not the same as pure insurance protection.

2. What happens if I don’t pay my premium on time?

Most policies offer a grace period after the due date, but the exact number of days depends on the policy and product type. If you still do not pay within the grace period, the policy may lapse, and coverage can stop. Always check the policy terms for renewal and revival rules.

3. Can I buy multiple insurance policies?

Yes, you can buy multiple policies if needed. This is common in health insurance and life insurance. For claims, the insurer will pay according to the policy terms and the nature of the loss. In some cases, the benefit is subject to indemnity principles, meaning you should not receive more than the actual covered loss where indemnity applies.

4. What is a nominee in an insurance policy?

A nominee is the person you name to receive the policy benefit if the insured event occurs, usually in life insurance. The nominee helps the insurer identify the person who should receive the claim amount, but the final legal position can depend on the type of policy and applicable laws.

5. Are all insurance claims guaranteed to be paid?

No. Claims are paid only when they are valid under the policy terms, within the coverage limits, and supported by proper documents. Claims can be affected by exclusions, waiting periods, non-disclosure, policy lapse, or incomplete paperwork. That is why reading the policy wording matters so much.

6. What are insurance riders and do I need them?

Riders are additional benefits you can add to a base policy for extra coverage, usually at an extra premium. Examples may include accidental death cover, disability benefit, or critical illness cover. You may need a rider if it fills a real protection gap, but not every rider is necessary for every buyer. Review your risk before adding one.